Julian Robertson: Lessons From the Tiger Who Was a Wolf

“If I had had to give my own money to any of them, I would have given it to Robertson. He knew stocks better than anyone.” Jim Chanos

Hedge fund legend Julian Robertson passed away this past August (Institutional Investor obituary, WSJ obituary, Bloomberg obituary). In my search for lessons from his life I revisited my archive of articles as well as the best chapter on Robertson which is in Sebastian Mallaby’s More Money Than God (I’ve talked to Mallaby about the history of hedge funds including Tiger). There is also a book about Robertson, A Tiger in the Land of Bulls and Bears, but it didn’t blow me away. If you have feedback, corrections, or interesting stories or content about Robertson and Tiger please reach out.

Despite its moniker, I think of Tiger as a wolf pack. Unlike some other great investors, Robertson didn’t hunt alone. One of his key strengths was his ability to attract talented analysts and bring out the best in them. In combination with his exceptional network, he created a research engine to constantly source and test ideas for the portfolio. His greatest legacy are the Tiger Cubs, the diaspora of former analysts who were mentored and put in business by him and who carry on his philosophy.

But even Robertson had to live through moments when it looked like the markets were conspiring against him, when the world was upside down, and everything he’d worked for seemed to be falling apart.

In early 2000, two legendary investors were wrestling with the dotcom boom. Stanley Druckenmiller was a trader and despite his fundamental research also took his cues from the market. After getting burned trying to short the high-flying tech stocks, he turned around and went long. Meanwhile, the dominant fundamental hedge fund manager of his era, Julian Robertson, was fighting to survive.

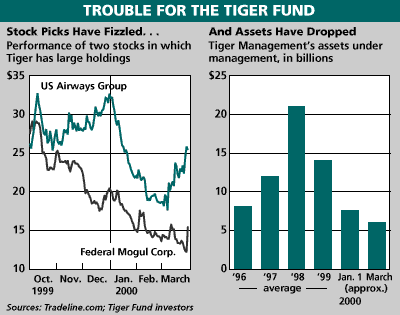

Business Week had called for his demise already in 1996. Prematurely as it turned out (Robertson had filed a defamation suit and the publication had settled with the acknowledgement that its prediction of poor performance had been incorrect). However, this time it was serious. Tiger was down nearly 40 percent since the beginning of 1998. Investors were redeeming and assets had shrunk from $21 billion to $6 billion in just two years.

Robertson’s portfolio of value stocks was out of favor and his global macro bets had turned against him. The New York Times pointed out that he was a value investor “in a market that's not value-oriented.” Robertson didn’t hide his frustrations:

“Some of these companies are selling at literally five and six times earnings and selling at two and three times cash flow. It's just wild.”

He was convinced the bubble was unsustainable, calling the “technology, Internet and telecom craze” a “Ponzi pyramid destined for collapse.”

“The only way to generate short-term performance in the current environment is to buy these stocks. That makes the process self-perpetuating until this pyramid eventually collapses under its own excess.”

However, while the bubble was still inflating it wreaked havoc on any short seller such as Tiger. On Invest Like The Best, Tiger Cub Stephen Mandel recounted the experience of shorting cash burning companies with no signs of the business improving or creating value: “the stock was $12. Six weeks later, on no news, the stock was 108." When bookseller Books-A-Million merely announced it was creating a website, its stock popped from $5 to $39.

When Robertson started his fund in 1980, short selling had been a profitable secret weapon, a “quiver that conventional funds lacked,” as Sebastian Mallaby wrote. Now it was “like being run over by a train that's going to derail a mile down the road.”

Robertson had no way of predicting when the bubble would end and like Druckenmiller he was burned out. He decided to shut down Tiger and published his closing letter on March 30, 2000, shortly after the Nasdaq had reached its peak.

“In May of 1980, Thorpe McKenzie and I started the Tiger funds with total capital of 8.8 million dollars. Eighteen years later, the 8.8 million had grown to 21 billion, an increase of over 259,000%. Our compound rate of return to partners during this period after all fees was 31.7%. No one had a better record.”1

Robertson was proven right. The bubble collapsed and his value stocks returned to favor. Whitney Tilson’s Value Investor Insight tracked the performance of Tiger’s final holdings from 2000 until 2006: the portfolio returned 120% compared to the S&P 500’s negative 7%. Funds that spun out of Tiger at the time put up incredible numbers in their first couple of years.

One could argue that Robertson was the last skeptic to capitulate. That the shutdown of Tiger was the kind of tragedy that the market demanded for a top to form. Did he simply lack the resilience, the grit to make it through this final challenge?

Imagine if he had stuck it out. Yes, he would have triumphantly returned and restored his track record. But then what? Perhaps he would have kept his role as portfolio manager of Tiger.

When Institutional Investor caught up with him in 2002, he seemed content. They asked whether he ever regretted his decision to close down his funds:

“I really don't. I can't do this forever. I'm not on the phone for an hour early in the morning from New Zealand [his second home]. I just couldn't wake up at age 95 worrying about my partners' money. I love my life so much now. In hindsight, I might have been better off closing two years earlier.”

His lasting legacy are the many investors he seeded and mentored. Would he have been better off with more money, a better track record, and more years of running other people’s money? Rather than devoting himself to being the mentor and catalyst for the next generation? I doubt it. I think the bubble can be viewed as a blessing in disguise, Glück im Unglück. It was the catalyst that allowed him to transition, painfully as it was, to the next stage in his life.