Hello everyone,

Welcome to the second part of my series on Stanley Druckenmiller (part 1). In this brief piece I’m going to cover the early 80s when Druckenmiller set up his own firm and struggled to build his business.

I’ve found several themes that are quite common among investors: the transition from managing capital to also being a business owner can be rocky and the pressures of running a small asset manager can affect investment decision-making. Also, developing your own unique style can take many years. Druckenmiller continuously evolved his thinking and reflected on his mistakes.

This piece is based primarily on his interview in The New Market Wizards. At this early stage in his career, Druckenmiller was not yet covered much by the press. In the next piece we will take a look at the crash of 1987 (based on Market Wizards, More Money Than God, and Barron’s). After joining George Soros in 1988, he received a lot more attention and we will have more sources to draw on such as Barron’s, Fortune, and newspapers like the Wall Street Journal and the New York Times.

I am working on overhauling the newsletter and plan on adding audio versions to my profiles. Audio and deep dive profiles will be available to the premium subscribers who support my work. This shorter piece is available to everyone, only the audio version will be behind the paywall.

Let’s pick up where we left off last time:

Druckenmiller came to Wall Street with a passion for games and a thirst for learning. His first mentor and a rapid succession of different roles within Pittsburgh National Bank ensured that he never fully adopted the mindset of the securities analyst. He started to blend fundamental, technical, and economic analysis into a unique perspective on industries and the overall market. …

It’s good to be interesting

In 1980, Druckenmiller made a presentation in New York and was approached by someone in the audience afterwards.

“You’re at a bank! What the hell are you doing at a bank?”

“What else am I going to do? Frankly, I think I’m lucky to be there, given the level of my experience.”

“Why don’t you start your own firm,” the man suggested.

“How can I possibly do that?” Druckenmiller asked. “I don’t have any money.”

“If you start your own firm,” he replied, “I’ll pay you $10,000 a month just to speak to you. You don’t even have to write any reports.”

It’s important to remember that even though Druckenmiller had been promoted to head of investments, he was only 27 and working at a regional bank. He was still only earning $48,000 a year. The prospect of $10,000 a month and a chance at running his own fund must have been mouth-watering.

Druckenmiller launched his firm, Duquesne Capital Management, in February 1981 with an analyst, a secretary, and a mere $1 million under management. He was charging 1 percent of AUM and thus his revenues would be $10,000 of asset management fees and $120,000 from consulting.

Raising capital without a track record requires an ability to build high-trust relationships and sell what is essentially a commodity product. Druckenmiller’s unique perspective on the market made him more than just an effective trader: it also made him interesting. He could have opened a research firm or written a Substack😉 – people wanted to hear his thoughts. I believe this is an underrated aspect of marketing funds. Some investors allocate capital not just to earn a return but also to gain access to the views and ideas of their portfolio managers.

Developing his own style

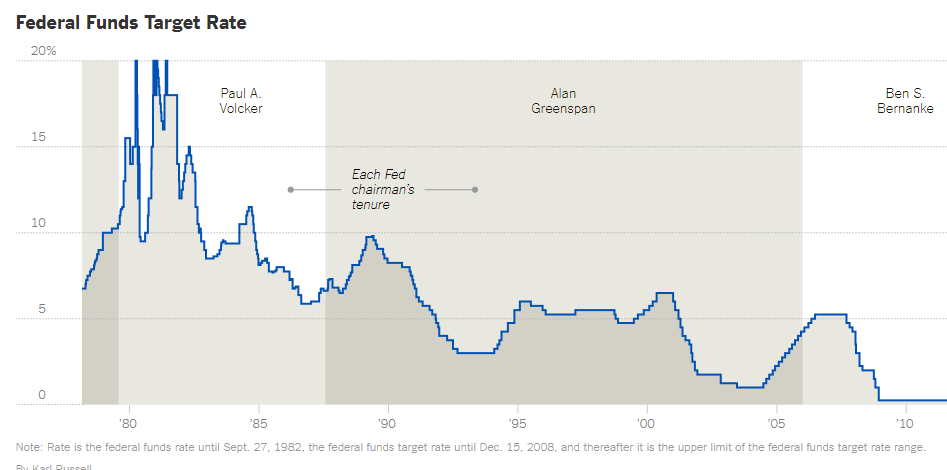

Druckenmiller remembered starting off “extremely well,” riding a bull market in small cap stocks. When Fed Chairman Paul Volcker aggressively hiked interest rates, the small caps stocks which were “up to the top of their valuation range” presented “one of the more obvious sell situations in the history of the market.”

While he correctly anticipated that Volcker’s attempt to crush inflation would tank the market, he was still operating with the mindset of a bank trust department portfolio manager.

“We went into a 50 percent cash position, which, at the time, I thought represented a really dramatic step.”

The remaining 50 percent of his portfolio however “got obliterated.” Druckenmiller was livid.

“You have to understand that I was unbelievably bearish in June 1981. I was absolutely right in that opinion, but we still ended up losing 12 percent during the third quarter.”

“I said to my partner, ‘This is criminal. We have never felt more strongly about anything than the bear side of this market and yet we ended up down for the quarter.’”

He was on his own now and the constraints of a bank’s conservative approach could no longer serve as an excuse. Frustrated, he changed his approach.

“Right then and there, we changed our investment philosophy so that if we ever felt that bearish about the market again we would go to a 100 percent cash position.”

Druckenmiller’s style started to become more aggressive, too. He sold his equities after a partial rebound, then positioned the portfolio 50 percent in cash and 50 percent long bonds. He successfully bet that Volcker’s rate hikes would start to curtail inflation and thus lead to lower long-term interest rates.

“I took 50 percent of the capital and put it into 30-year treasury bonds yielding 14 percent, and I owned nothing else. I could see that there is no way this man was going to let inflation go.”

He was still developing his view on sizing however:

“Had I known George Soros when I made the bond bet,” he commented later, “I probably would have made a lot more money because I wouldn’t have put 50 percent in the bonds, I probably would have put about 150 percent in the bonds.”

Never force a trade

While Druckenmiller was doing well and his assets under management increased to $7 million, his consulting client, disappeared (and later ended up in prison). Without the consulting fees and an annual overhead of $180,000, Duquesne started bleeding cash. According to Bloomberg, Roger Entress, a Pittsburgh surgeon, early Duquesne investor, and long-time golf partner, let Druckenmiller live in his apartment rent free.

Druckenmiller had $50,000 of his own capital and decided to throw a hail mary pass. He was convinced rates were heading lower and “took all of the firm’s capital and put it into T-bill futures.”

In the span of four days, he “lost everything” on his leveraged bet. In a cruel twist, interest rates reached their peak only a week later. Druckenmiller had been right on the direction but too early and far too aggressive.

“That was when I learned that you could be right on a market and still end up losing if you use excessive leverage.”

He was forced to raise $150,000 from one of his clients in exchange for a 25 percent stake in the company. I don’t know when or how Druckenmiller bought the stake back, but it must have been a great trade for his partner. Within a year, Duquesne’s assets under management climbed to $40 million. By 1983, Druckenmiller joked that he finally made more than his secretary.

In 1986, he was approached by Howard Stein who headed the Dreyfus funds. Druckenmiller started to manage mutual funds for Dreyfus including one that shot up 40 percent in the span of three months, earning Druckenmiller more public attention and fund mandates at Dreyfus. Druckenmiller also borrowed $75,000 from a friend to start a hedge fund which allowed him to charge 20 percent of profits on top of the management fee.

With his business on solid grounds, Druckenmiller could now focus exclusively on trading. Next time we’ll see him meet - and even outshine - his new mentor.

Enjoyed this piece? Please let me know by hitting the ❤ button. It makes my day to see whether my readers like the content (it really does!) Thank you!

If you enjoy my work, please consider sharing it with friends who might be interested.🙏

There is no further text behind the paywall. The paywall is turned on for the audio version of this piece.