📚No Grand Strategy: The Complete Financial History of Berkshire Hathaway

“Buffett’s raw material was a dying textile company with $22 million in net worth, no durable competitive advantage, and high capital costs.”

Hello everyone,

About a year ago, I talked to Gary Hoover who runs the American Business History Center. A former founder of a chain of bookstores, Gary had collected one of the country’s largest private libraries of books and magazines about business history.

A week ago, the building housing his collection burned to the ground. Thankfully, Gary escaped unharmed. But the home, and the history, are gone. There is a gofundme to support Gary in case you feel inclined to help out. But that’s not the point of this post. It’s a tragic coincidence that this happened when I was drafting a piece related to the history of Berkshire Hathaway.

Business history is an odd topic. Why would anyone other than enthusiasts and employees care about the past of a particular company? Doesn’t the market change too quickly? During our conversation, Gary reflected soberly that “nothing that deeply matters in business is new.”

“The key ideas of business are timeless. Human behavior, the fundamentals of finance, how to lead, strategies in competitive battles, and many other things are the same stories repeated over and over. My education as to how to be a retailer came from reading the lives of the greats of the 19th and 20th centuries, and those lessons apply more than ever as we go through the 21st century. The same is true of virtually every industry.” Gary Hoover

While Gary is interested in the rise and fall of corporations in a variety of industries, you can go the other way and deeply study just one outstanding business. That’s what Adam Mead did in The Complete Financial History of Berkshire Hathaway. His insights led me to finally tackle Charlie Bluhdorn recently. The following quotes are from Adam unless attributed to someone else.

On the one hand, his book is an exhaustive financial history filled to the brim with data, a reference work for the serious student. “I wrote the book I always wanted,” he told me.

“In the context of 10,000 plus pages, which is roughly my source material, the 750 pages of my book is fairly concise.”

It’s easy to forget how much history hides behind this chart.

On the other hand, it offers a sharpened perspective because it tackles only the business, without diversions into Buffett and Munger’s personal lives. And Adam breaks down 55 years of deals into digestible decades.

Themes emerge for each decade. The connective tissue behind many decisions, the lessons from successes and mistakes, becomes clearer. I don’t think it’s necessary to look at each and every investment. But to see Berkshire emerge as something organic, the result of a myriad of individual decisions, is immensely valuable. The company changed its shape many times based on Buffett’s evolution as an investor and the market environment he found himself in.

An accident of history

Consider its unlikely origins. Buffett, brilliant as he was, got himself into the driver’s seat out of spite. Cigar butt investments, as Berkshire was, are there to be picked up, smoked, and discarded. Buffett intended to exit the stock through a tender offer before Seabury Stanton, Berkshire’s CEO, tried to short-change him by 12 ½ cents. In that moment, the otherwise calculating and rational Buffett made an emotional decision.

Instead of moving on to the next stock, he stuck around. He committed. I find it utterly relatable that he took it personally, that he got triggered into taking control of a basket case of a company. He was going to show people how to build a great business. It’s a testament to his abilities and what Adam described as “patient opportunism” that Berkshire turned out the way it did.

“Building Berkshire was an exercise in patience combined with opportunism and a reminder that opportunity cost matters. There was no grand strategy.”

It also reflected the initial conditions in which Buffett and Munger operated, including having the “good fortune to observe what worked and what didn’t” at the previous generation of conglomerates. “These lessons were then applied to their canvas at Berkshire to create a masterpiece.”

“Warren Buffett and Charlie Munger were born at the right time to fill their sails, and that of their conglomerate, with incredible tailwinds. They were lucky to begin solidifying Berkshire’s economic position when market inefficiencies were much more prevalent.”

There was no grand plan and small mistakes turned out to be the stepping stones on the way to great success.

“Mistakes in capital allocation, such as the losses experienced in Florida and Texas in Berkshire’s Insurance Group, do happen. The key is making sure bad investments don’t put the larger enterprise at risk, learning lessons from those mistakes, and communicating candidly with shareholders about them.”

However, Berkshire under Buffett was never truly in peril. Buffett carefully created structures that ensured survival. There’s a lesson in that, too.

“[Buffett] wrote that Berkshire probably could have increased the 23.8% compounded annual return it had achieved by borrowing more money, but he was uncomfortable with even a 1% chance of failure. Even at 99:1 odds, he and Munger would not have been comfortable with the risks.”

“Charlie and I have never been in a big hurry: We enjoy the process far more than the proceeds—though we have learned to live with those also.”

Before publishing my conversation with Adam, I want to share some quotes from the book. If you enjoy Adam’s take on Berkshire, consider checking out the book or his website which has a massive Berkshire spreadsheet and tons of other goodies.

Structure as a reflection of personality

Adam explains how Berkshire’s decentralized structure followed Buffett and Munger’s backgrounds as stock pickers. Despite being very interested in the operations, they had no desire in becoming hands-on managers themselves.

“Berkshire was constructed using what might be termed a portfolio approach. It became a collection of businesses and not one large business with operational oversight of multiple business activities. This is an important distinction. Berkshire’s capital allocators were accustomed to acting as owners, not managers.”

This enabled greater scale and meant that the impact of a growing capital base on returns, what Buffett calls a ‘self-forged anchor’, was delayed somewhat.

“The extreme autonomy given to operating managers meant the company could scale almost without limit and not become unwieldy. Autonomy had the added benefit of providing managers with a sense of ownership that motivated them outside of any monetary benefits. Berkshire maximized business potential by maximizing human potential.”

However, this required an unusually high level of trust.

“Another nuanced risk Berkshire successfully managed was trust. Berkshire understood there were risks related to its policy of extreme autonomy. A delicate balance existed between maximizing human potential (and by extension business potential) by being hands off, all the while maintaining adequate oversight. Berkshire took the position that it was better to over trust and incur infrequent but public embarrassments than impose strict controls that were a net negative. It continually reinforced the message that it cared for Berkshire’s reputation first and foremost.”

Focus on what’s important

Great investors are able to identify and focus on the key driver’s behind a business’s performance. For Berkshire, it was Buffett’s ability to source attract investments, having the right managers, and optimizing Berkshire’s capital structure. If he got those right, the flywheel would inevitably spin.

“A central guiding principle was to focus on the underlying business. It did not matter whether the actual investment was a whole company, part of a company via stocks, or lending to a business via fixed income investments.”

“A focus on the long-term economic characteristics of businesses was paramount to Berkshire’s success. This included seeking businesses with strong economic moats.”

“Owners’ wealth is built over the long run by focusing on economic realities. Accounting is only the starting point of the analysis, and it oftentimes “obscures rather than illuminates,” according to Buffett. In Berkshire’s case, this was an acute problem since significant value resided in the look-through earnings.”

“Buffett said a company’s profitability is determined by three factors: “1. What its assets earn; 2. What its liabilities cost; and 3. Its utilization of ‘leverage’.” Berkshire did a good job earning high returns on assets, but its liabilities also contributed to its outsized success.”

Buffett likes to say that it’s “not necessary to do extraordinary things to get extraordinary results.” Getting the basics right and letting the output compound over long periods of time can itself be extraordinary.

That said, this is anything but ordinary in my book:

“Over a long period, Berkshire found the optimal financial structure, use of a permanent and low cost source of capital, motivated and properly incentivized management teams, judicious risk management techniques, care for the individual shareholder, and a base of owners that supported the company’s strategy.”

Reshaping Berkshire through the decades

A fascinating aspect of Berkshire is how often it made concentrated investments whose importance, despite performing well, quickly faded. Who knew that Buffett bet nearly half his capital on a regional bank? Berkshire changed its shape regularly as Buffett deployed ever greater stacks of capital.

The following table hints at different themes throughout the decades. Notice the changing concentration in the top four stock positions and the growth and decline of the stock portfolio as a share of the overall equity.

I’m going to share just a few key quotes for each decade.

1965-1974

“This first decade of Berkshire Hathaway under Warren Buffett’s control is in some respects the most important. Like a caterpillar that morphs into a butterfly, Berkshire began a transition from a textile company to a conglomerate almost unrecognizable from its former self.”

“Buffett was shaping Berkshire into not the best textile company, but the best company—period.”

“One lesson was that even the most talented management team can’t save a business with bad economics. Another was how swiftly capital allocation could shift the fortunes of a company for the better, which in this decade were the two large acquisitions of National Indemnity (1967) and the Illinois National Bank and Trust of Rockford (1969). These bold moves represented 28% and 44% of Berkshire’s average equity capital at the time of purchase, respectively.”

1975-1984

“The Berkshire that emerged from Buffett’s second decade would be the result of the successful allocation of over $1 billion of capital. This result would come in part from great patience and fortitude in the face of the economic recession of the mid-1970s, the large storm that hit the usually strong insurance industry during the latter half of the decade, record interest rates, troubles at the Buffalo News, and other challenges along the way.”

“Even good businesses can experience challenges. Buffett and Munger faced many problems from the Insurance Group during the decade and oversaw massive underwriting losses toward the end of it. … The actions of competitors in the insurance industry and their lack of understanding about the true, long-term cost of doing business, caused industry premiums to be inadequate.

1985-1994

“The 1985–1994 decade was one where Berkshire Hathaway moved swiftly to implement its leaders’ understanding of good businesses, and in particular the potential for value creation in its insurance operations.”

“Berkshire perfected its understanding of insurance. It lost money in all but two of these years (1993–94) and used those lessons to engrain in the entire organization a philosophy of underwriting profitably first and foremost. Berkshire moved confidently into reinsurance and generated huge amounts of float to invest in marketable securities.”

“Ajit Jain joins Berkshire and begins building an insurance powerhouse focused squarely on profitability.”

1995-2004

“The 1995–2004 decade was notable for the wave of acquisition activity—in particular, the growth in insurance through the acquisitions of General Re and the remainder of GEICO.”

“Buffett shared his formula in his 1995 Chairman’s letter: Berkshire had ‘benefited greatly—to a degree that is not generally well-understood—because our liabilities have cost us very little.’”

When would you have placed your bet?

This question lingered on my mind after my recent piece on searching for the next Buffett. At what point would an outside investor have bet on Buffett?

Berkshire was traded over the counter until its listing on the New York Stock Exchange in 1988. There was no research coverage either. How would one have heard about it? Unless one stumbled across one of Buffett’s shareholder letters or was familiar with his track record as manager of a small investment partnership, why would one investigate it? And neither of those documents were easily accessible in the pre-internet era.

The stock did well during Buffett’s first decade at the company.

By the end of that decade however, shareholders owned a smorgasbord of assets:

“Owners of Berkshire in turn owned an insurance operation, a bank, a newspaper, and, through Blue Chip Stamps, an interest in a trading stamps business, another bank, and a candy company.”

Does that really sound like the world’s greatest compounding machine in the making?

Adam agreed that it was a difficult question.

“You'd like to say, ‘I would get in there super early and I would get this thing at rock bottom.’ But I don't know if I would have.”

He put the moment at which investors recognized there was something special going on in Omaha as ‘probably the mid-80s.’ And I agree.

The 1970s were an amazing environment for Buffett to deploy capital. He emerged as a financial celebrity once he reaped the rewards of those shrewd purchases. The below chart stood out to me because I think of the 1970s as a long and painful bear market. Yet Berkshire quickly surpassed its old highs.

Its performance was astounding as “book value per share increased from $90.02 at year-end 1974 to $1,108.77 at year end 1984—a compounded annual rate of return of 28.5%.”

No wonder people started paying attention.

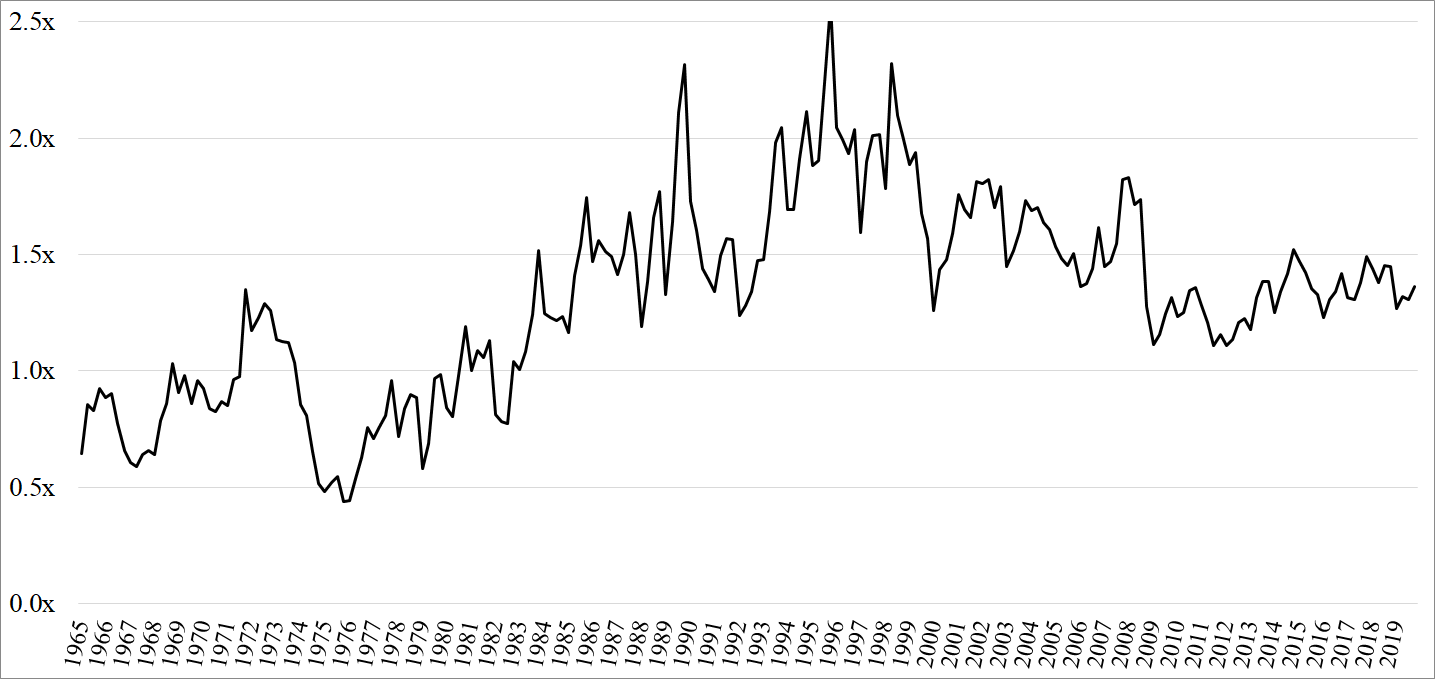

Valuation confirms that it took investors until the mid-80s before they ascribed a premium to Buffett’s skills and the value of the operating businesses accumulating within the Berkshire umbrella. That’s when the price to book ratio sustainably rose above 1.0x, meaning a dollar invested at Berkshire was ascribed more than a dollar of value by the market.

Berkshire’s price to book ratio:

If Druckenmiller is right and we possibly face a lost decade in markets, who wouldn’t want to find the next Berkshire, the company that will break out regardless? While the many details of its history may remain the domain of enthusiasts, the guiding ideas behind its success are as relevant as ever.

: Adam J. Mead, John Bradford, Harriman House Ltd: Audible Books")

done.

there is a pic of Warren sitting in his office purposed by the camera eye

as the consummate reader. oh what a grand! it was for my own eye

to catch that worn Value Line Investment Survey compendium perched

by an arm's reach from Warren at the moment necessary. I studied that

same paper cave of financial & technical details on those 1700 stocks in

my small town library back in the 70's. arriving full circle; here is one of

your best write ups for my own financial curiosity & it's one that wills

the karmic influx my way. for sure, Adam Mead's effort will sit in front of

me pretty damn quick thanks to Neckar's connection.

I really enjoyed our chat, Frederik! Happy to answer any questions readers have here in the chat. Or ping me on Twitter: @brk_student