Hello everyone,

This will be the last piece on Druckenmiller for now. Next up will be a piece on Soros and then we’ll return to a variety of other personalities. I’ve recorded an audio companion piece which includes some snippets from Druckenmiller’s interview. You can listen to it in your podcast player by using the link on the bottom-right of the Substack player.

After my last piece on the aftermath of 1987 and Druckenmiller’s open-mindedness (“one of my strengths over the years was having deep respect for the markets and using the markets to predict the economy”), I revisited his 2018 interview with Bloomberg’s Erik Schatzker (my notes on Twitter). Druckenmiller elaborated on this idea but also described how changes in markets had made it much more difficult to implement:

“A big part of my process is taking signals from markets. I’ve always believed markets are smarter than I am. They send out a message and if I listen to them properly, no matter how powerful my thesis, if they’re screaming something else, it’s telling me you’ve got to re-evaluate. You got to re-evaluate it. If it’s still alright, fine. But you've got to be open-minded.”

Referring to his first mentor, Speros Drelles, he said: “My first mentor used to say: 100 million Frenchmen can't be wrong. It was his saying that the the voice of the market was always correct and I need to listen to it.”

But today’s markets acted differently:

"About 6-7 years ago, the combination of central banks cancelling the signals but, maybe more importantly, the algos coming in with very sophisticated models."

Druckenmiller had trusted the “invisible hand” of the market leading to trends he could trade. Now, “the algos, machines trading, they tend to have different motivations. They're not nearly as momentum oriented. It has severely inhibited my ability to read the signals."

For example, in the past, “if a company was reporting great earnings and the stock just didn't act well for three or four months,” he said, “almost inevitably something happened that you didn't foresee six months down the road.” Price was a valuable signal.

"I'll never forget, 2-3 years ago, Facebook had reported great earnings. Stock was like 122, opens at 131 after hours, 3 days later it's at 116. The analysts come in... nothing's wrong.

I said, No kid you're wrong something's going to come out you just don't know it yet. Anyway a year later the stock was like 220. So that didn't mean anything."

“The price signals I learned to read are broken, they certainly don't work the way they used to. I still like price action versus news but it used to be a very very important part of my process.”

While he still listens to the market, particularly in the form of cyclical sectors, but it has become a lot noisier:

"I think the message over eight or nine months is still great. Like here I am telling you what the auto stocks are doing. I just think over a week or two you're getting noise that used to mean something and now it doesn't mean anything."

The search for valuable signals dates back to Druckenmiller’s early days as an analyst. As self-described “top-down investor,” it seems to me he focused mostly cyclical sectors. Their behavior could give him a read on the overall economy and market. And anticipating their next move could be profitable and would play more to his strength than assessing a single company’s business model or valuation.

He was looking for a disconnect between the direction of an industry’s fundamentals and market expectations.

“Economic signals and puzzle solving is something I’ve done for a long time, and I have confidence in it.”

It’s a very different approach from bottom-up investors who may focus on valuation, quality, or growth trajectory of individual companies. Druckenmiller was not looking to hold and compound for the long-term. He needed for the market to agree with his view of the industry’s changing fundamentals over the next 1-3 years.

While he discussed individual long and short stock picks in 1988, they were mostly expressions of his view of an entire industry. Much of it reminded me of Marathon Asset Management’s capital cycle framework:

“The first notion is that high returns tend to attract capital, just as low returns repel it. The resulting ebb and flow of capital affects the competitive environment of industries in often predictable ways – what we like to call the capital cycle.

Typically, capital is attracted into high-return businesses and leaves when returns fall below the cost of capital. This process is not static, but cyclical – there is constant flux. The inflow of capital leads to new investment, which over time increases capacity in the sector and eventually pushes down returns. Conversely, when returns are low, capital exits and capacity is reduced; over time, then, profitability recovers.

The key to the “capital cycle” approach – the term Marathon uses to describe its investment analysis – is to understand how changes in the amount of capital employed within an industry are likely to impact upon future returns.

Capital cycle analysis looks at how the competitive position of a company is affected by changes in the industry’s supply side.” Capital Returns

Many of Druckenmiller’s public appearances have had a bearish tilt: such as in 1988, at various times since the financial crisis, and when described markets as the “everything bubble” in November 2021.

But when Schatzker asked him about whether “grumpiness” was a good quality as an investor, he pushed back:

"Bulls make more money than bears. Being an optimist about life is a great attribute as an investor. You just can't be starry-eyed and naïve. You have to be a little skeptical, a bit of a contrarian."

Especially since navigating bear markets is hard:

“I’ve done well in bear markets. I’d love to sit here and tell you I made it shorting stocks. It’s always very difficult in a bear market. They don’t trade with rhythm, you get these vicious rallies, you get squeezed out of shorts and people play all sorts of games. I always made it in Treasuries, because Treasury yields would go down dramatically.”

Even so, Druckenmiller has long had a concern about a tail risk in which bonds no longer act as the trusted diversifier. Concerns about the US’s debt levels, deficits, and demand for the dollar are not new and not unique to him. They did prevent him from profiting from bonds.

But it is interesting to see, with these concerns coming back en vogue, how long they date back.

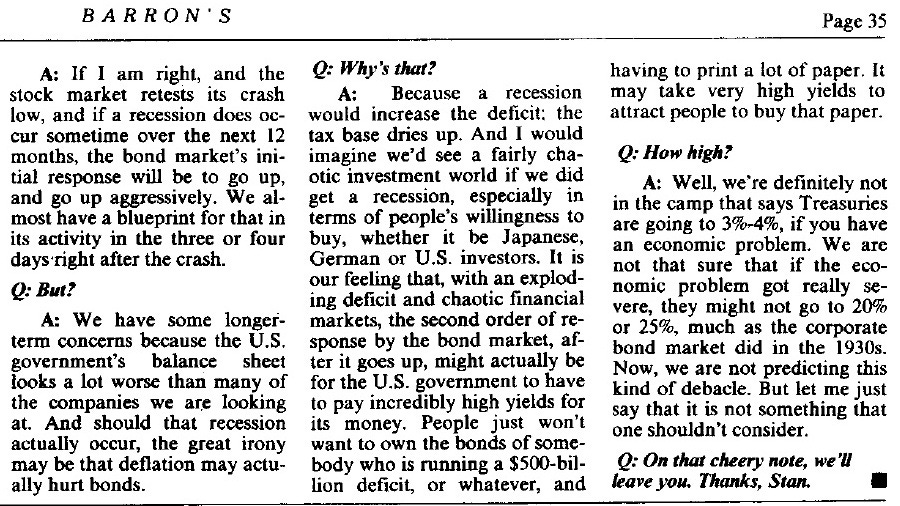

“If I am right, and the stock market retests its crash low, and if a recession does occur … the bond markets initial response will be to go up.

The great irony may be that … a recession would increase the deficit. … We’d see a fairly chaotic investment world …. in terms of people’s willingness to buy.

With an exploding deficit and chaotic financial markets, the second order response by the bond market … might be for the US government to have to pay incredibly high yields.”

Highlights from Barron’s “Shorts’ Story” and Fortune’s “Battening Down for a Recession”:

Druckenmiller’s Mandate & Mindset

Markets Train You, Then Humiliate You

Short the Japanese bubble: “History never repeats itself.”

The only good economist I have found is the stock market.

Three views of market: valuation, liquidity, technical analysis

Valuation: the risk level

Liquidity: the Fed and Corporate America’s Capital Cycle

Technical Analysis

Top-Down, Sector-Driven Stock Picking

Disclaimer: I write and podcast for entertainment purposes only. The information in this publication is not intended to constitute investment advice and is not designed to meet your personal financial situation. Consult your financial adviser to understand whether any investment is suitable for your specific needs and before making investment decisions. I may, from time to time, have positions in the securities covered in my articles. This is not a recommendation to buy or sell securities.