How Craig McCaw Pioneered the Wireless Age

"Some said I was a 'crackpot' (many still do)."

“You learn and you see an opportunity - a gap between what is and what should be. If one thinks in anthropological terms, if you go towards what should be, then eventually things will get there and you just have to work out the timing. With cellular telephony, in particular, we saw an enormous gap between what was and what should be. [The fixed phone system] makes absolutely no sense. It is machines dominating human beings. The idea that people went to a small cubicle, a six-by-ten office, and sat there all day at the end of a six-foot cord was anathema to me. If one thing is obvious, people will pay, will contribute something for control of their lives, the right to choose.” - Craig McCaw in Money from Thin Air, a biography written by O. Casey Corr.

Venture capitalist Bill Gurley once attended a talk by Bill Gates and was surprised to hear Gates call Craig McCaw one of the people he most admired. McCaw not only saw the potential of cellular telephony, an industry considered too small for AT&T to focus on, he bet his life’s work on a highly leveraged gold rush to acquire licenses and create the leading company in the space. This came after McCaw and his brothers had built a cable operator out of the ashes of his father’s business empire.

McCaw’s determination sold capital providers on a vision of the future when neither cable nor cellular businesses showed profits. As Gurley put it, McCaw, "had convinced investors in not one, but two industries to pay attention to proxy valuations as opposed to traditional valuation metrics. McCaw convinced analysts and investors alike that valuation tools such as price-earnings and price-cash flow were flawed when evaluating early-stage infrastructure plays. As alternatives, he offered up new metrics such as 'homes passed' and 'POPs.'"

Financier Michael Milken commented on McCaw’s commitment: "Craig McCaw’s family was in cable, radio, television. They were willing to give all that up for cellular. You wanted to find that individual who had passion for what they were doing. Finding great people and backing them is obviously one of the great decisions."

There is a lot to learn from McCaw, who made a fortune in two industries before reaching a bit too far into the future during the telecom boom.

Early Lessons

Craig McCaw was born in 1949 in Centralia, WA, a small railroad and lumber town outside of Seattle. He was one of four sons of Elroy McCaw, an ambitious entrepreneur whose business experience — and mistakes — provided Craig some influential lessons.

Starting with a local radio station when the industry was still in its infancy, Elroy acquired and built a string of businesses after WWII. He borrowed heavily and bought into stations from Hawaii to Texas. In 1953, he bought a money-losing radio station in New York with $60,000 in equity. He cut costs, introduced rock 'n roll music, and hired popular disc jockeys. He sold the station to Westinghouse Broadcasting for $10 million. After that he continued to invest in a variety of ventures, including an attempt at a 24-hour financial news network.

Along the way Elroy tried to teach his sons from an early age, often taking Craig on business trips and playing chess with him.

Then, one day in 1969, Craig found his father’s body. Elroy had died of a stroke at age 57.

In the following years, the McCaw business empire was dismantled. The portfolio had been built on handshake deals and leverage. An estimated $12 million estate dwindled to $20,000 as creditors and business partners claimed assets. Bill Gates’s father, William Gates Sr., was the McCaw family’s attorney and helped sort out the mess over the course of a decade.

The family lost all of its businesses except for a tiny local cable system with 3,000 subscribers, which Elroy had gifted to his sons when they were still teenagers. Their mother wanted to sell it, but the brothers had other ideas. They decided to run and grow the company instead.

The ugly unraveling of his father’s work taught Craig McCaw invaluable lessons. His father had spread himself too thin, he failed to keep track of the details and trusted the wrong people. He tried to do too much himself. Craig took those lessons to heart:

“I'm picky about the people I do business with. He wasn't picky. I learned to be fastidious about accounting, to be careful about the ethical nature of people. And to keep things simple, to focus on quality,” he told Forbes in 2000.1

“My father was a visionary who did not hire great people. The company was too dependent on one person.’’ 25iq

Craig also learned he was dyslexic. He did not let this discourage him but recognized he had to play to his unique strengths and find ways to make up for his weaknesses.

“A dyslexic tends to be more conceptual and do things which other people wouldn’t see as obvious. So maybe it’s a strategic asset . . . I can’t go to a piece of paper and organize things as most people would in a way that they could understand and come up with a plan,” he told the Seattle Times.

“I think I had trouble fitting as a dyslexic. I don’t think like other people, so I don’t fit very well in a clique. As a result of that I have trouble quantifying people as directly as others. I look at their ideas, rather than at them so much as individuals… if you pass autonomy as far down in any grouping of people as you can, you will get extraordinary results if you ask for a lot. The greatest burden you can put on someone is trust.” 25iq

Cable and Pagers

In the mid-1970s, McCaw put his tiny cable system on a path to rapid growth through acquisitions, leverage, and a detail-oriented team to complement his skills. He brought on Wayne Perry, a former tax attorney who structured the different cable systems to remain independent and leveraged to minimize the tax payments due to a lack of taxable profits. “Wayne was the brilliant consigliere. Not a good leader, but a brilliant inside guy,” he said in Money From Thin Air, a book I will quote at length and worth reading if you’d like to learn more about him.

Leverage was a crucial component for the expansion and McCaw hired a former banker as his CFO to continuously search for bank financing and improve terms. Over time, they sought to negotiate documents to gain more flexibility. For example, they replaced “authorized spending” from “cable company” to “communications business,” leaving room to deploy capital in new ventures.

Banks lent based on a multiple on cash flow, around four to five times in the beginning, later in the high single digits. Therefore, every incremental dollar of cash flow provided purchasing power for further acquisitions. Like other cable operators, McCaw acquired smaller systems and was able to boost cash flow by consolidating costs like billing and maintenance. With growing scale he could also negotiate better volume discounts with the cable channels. The result was a growing system that continuously increased borrowing capacity and reinvested the available cash into more acquisitions. Perry called the company “an efficient predator. Always hungry, it kept moving, kept buying. We were like a shark — eat or die.”

Closing deals required focus and speed. Once there was an interested seller, the team went into overdrive, working all night to crunch numbers and get to “90 per cent of comfort.” Then they’d visit the seller immediately and whoever was on the scene had full authority to make a deal. The motto was “sign ‘em quick, close ‘em slow” — get effective control by striking a deal quickly but don’t rush to wire the money.

“We always leveraged future growth,” said Perry. “We would go to a programmer… we want you to give us discounts equal to 250,000 subscribers and we’ll promise to be there by the end of the contract. If not, we’ll have to rebate you all the money.”

McCaw later reminisced: “I started out in the cable business, where you are acutely aware of the “homes-passed” cost of extending your network. You are also very aware of what your lender is charging you for capital, and you have certain assumptions about what the speed of customer adoption will be.”

McCaw also acquired a small but profitable paging business in Centralia, WA. “Some said I was a 'crackpot' (many still do), because Centralia was not a market large enough to support a paging business. But the business succeeded because there really was a need there,” he recalled at a luncheon. Through the paging business he became a licensee of radio spectrum and in 1979, he and other operators attended a conference organized by Motorola to explore a novel business: cellular telephony.

The Bet of a Lifetime

AT&T’s Bell Labs tested its first cellular system in 1974 but it took until 1979 before the FCC established its cellular policy and began the process of issuing bandwidth licenses.

In 1980, AT&T asked McKinsey for an analysis of the market for wireless telephony. The consultants came up with 900,000 subscribers by the year 2000. This was too small a market for AT&T to focus on, especially at a time when it was being broken up into the Baby Bells and also tried to enter the computer business. McKinsey’s estimate turned out to be less than 1 per cent of the actual subscriber number.

The story reminded me of the moment when Western Union, America’s dominant telegraph business, declined to buy the telephone patents from Alexander Graham Bell. Bell had been struggling to raise additional capital and was willing to sell out. But much like AT&T, Western Union couldn’t see the value in the technology that would later displace its business.

While the number was too small for Bell, it was large enough to entice an upstart like McCaw, who quickly locked on to the enormous potential of cellular. In 1981, he dug up the projections AT&T had filed with the Federal Communications Commission and went to work (an important reminder of the treasures buried in public disclosure).

An Undervalued Asset

Licenses were being awarded to Baby Bells and independent bidders and could be bought for around $4.50 per “pop” or “population covered.” McCaw didn’t know exactly what they would be worth. But based on AT&T’s data, he believed they were worth a lot more. And he preferred to be roughly right to being exactly wrong. Perry recalled: “The AT&T projections made it a no-brainer to go to 80 bucks a pop.”

Getting an allocation of the early licenses was a key step. “I knew from cable you had to promise big dreams,” meaning broad coverage and service. “Take care of people. That’s what [regulators] want to see.” McCaw was granted licenses in six of the top 30 markets in the US in 1983.

In the following land rush to acquire licenses, he recycled his father’s pioneering spirit and traveled all over the country to meet with smaller operators. All kinds of speculators had bought licenses. Some had heard the idea on a television show about speculative investments. Even Bill and Hillary Clinton turned $2,000 into $48,000 by being in a partnership that acquired a license, according to the Seattle Times.

McCaw bought licenses from dentists, small business owners, an ambulance driver, and a man who lived in a mobile home deep in the woods of Oregon. McCaw bought the hermit’s licenses for $3 million. One couple won the license for Yakima, WA, and turned $15,000 into $1 million when McCaw bought them out. Being nimble and fast was key. McCaw and his brothers had a one-page sales agreement. They crisscrossed the nation asking owners: "what will it take to get you to sign right now?"

Financing the Buying Spree

This buying spree required a lot of capital. After Salomon and other banks failed to raise debt, McCaw met with Michael Milken who greeted him with the words, “You’ve got to show strength. How much you looking for?”

With Milken’s help, McCaw was able to close a linchpin deal: acquire MCI’s cellular and paging operations for $120 million. One of McCaw’s lieutenants estimated that without junk bonds, McCaw would have had to sell some 60 per cent of the equity — worth nearly a billion dollars later. After selling MCI’s paging operations for $75 million, McCaw had effectively paid $46 million for cellular properties valued at $1 billion seven years later.

Milken recounted working with McCaw on a podcast episode:

"Let's talk about Craig McCaw. He went everywhere in the world and no one would give him money. So, when he came to me, I told Craig, 'if you need a brain surgeon, would you go to a veterinarian?' It would be hard for people to believe it today. But the most difficult thing to finance, of all the industries that I financed, was mobile. People couldn't understand why they needed mobile. No one would give him the capital. We developed a very close relationship. I believed the future was mobile. I had seen Captain Kirk tell Scotty to beam him up. Craig had this belief that your communication device was where you were, not the communication device itself.”

"His family had built radio, television, cable. I told Craig that his vision was going to require so much capital, that if he and his family wanted to own a significant share of the company, he was going to have to sell everything."

In 1987, the McCaws sold the cable business with 434,000 subscribers for $755 million. Craig personally made around $250 million, according to Forbes. He invested all his capital in the cellular business, and convinced the capital markets of the value of the licenses such that he could use them as collateral. He raised more than $1.25 billion in junk bonds with Milken and sold a minority equity stake to a British company. His acquisition spree culminated in 1989 with the acquisition of LIN Broadcasting for $3.5 billion, paying $350 per pop.

McCaw didn’t view his big bet on cellular as risky: "We have always been risk-averse, in spite of our willingness to borrow a lot of money." He recounted how on early business trips his father had taught him the concept of an exit strategy. Wayne Perry said: "Every deal we ever did had a back door. The public just didn't see the back doors."

The back door was his competing bidders, the Baby Bells. As long as McCaw bought licenses below their intrinsic value and in the right locations, he was confident he could unload the assets and survive a crisis.

“Never go through the front door unless you’ve got a back door, and the hardest thing to get people to do is to not commit themselves to one course of action. Playing chess with my father, I give him credit for that. I mean, if you haven’t thought three moves ahead and what if he does this, and what if that happens. You can take chances, but you never, ever play the game without an out.”

Exit Through the Back Door

In the early 1990s, McCaw shifted his focus from expansion to integration and customer acquisition. In Jim Barksdale he hired an experienced manager from FedEx to streamline his fragmented organization. McCaw said of Barksdale: “He took a great mergers-and-acquisitions company [McCaw Cellular] and made it into a great operating company.”

Fast-growing McCaw Cellular had an entrepreneurial and decentralized culture. Chief Technology Officer Nicolas Kauser: "McCaw has traditional telephone people in 10 per cent of the jobs, and all of those are in technical areas. Besides them, I can't think of any people here from the telecom industry. We have people who used to sell fridges and cars. That's what gave us a new spin."

Todd Wolfenbarger described the ‘McCaw formula’: "An opportunity is tapped, and a frantic pace follows, but everyone associated with the effort is handed fulfilling fragments. It's your business to run and you have fun running it."

But the company was buckling under $5 billion in debt, including $3 billion McCaw had needed for the Lin Broadcasting deal. One of his executives, Thomas Alberg, remembered: "We got close to the edge a couple of times. McCaw was viewed as a great risk taker, but we were also very much infused with a sense that we have to be careful, too."

Alberg and Perry negotiated an exit deal with AT&T. In November 1992, AT&T acquired one-third of the company in a $3.8 billion deal. AT&T also received an option to acquire control.

McCaw explained the deal to his employees. “You all know, this deal includes the potential that they can fire me. They can't fire you, but they can fire me,” he said. “So long as we run the company well, AT&T won't have reason to take us over. We must work hard,” he said, a smile forming on his face, "because I never want to be fired.”

At that point, McCaw Cellular generated $1.75 billion in sales and had two million subscribers. In 1993, AT&T acquired the rest in an $11.5 billion deal (plus $5 billion in assumed debt). McCaw and his brothers made $2.3 billion, according to Fortune.

The Telecom Boom

Selling his company under pressure was a tough decision for Craig McCaw. He told a friend, "Well, I guess my career is over."

He decided against going on the AT&T board and instead formed his family office Eagle River to make private equity investments. McCaw felt he had missed early opportunities to invest in the growth of the Internet, and now was his time to make up for it. A telecommunications boom was picking up steam and McCaw was free to place his bets.

"Two or three years before the Netscape IPO, Steve Jobs came to Seattle and we were just chitchatting. He said, 'The Internet is it. I think it is the greatest change coming in computing.' And I thought, 'It sounds great. How do we buy it?' Well, it wasn't quite that easy." He did look into buying a piece of one or another of the companies that connect users to the Internet, like UUNet, but thought they were all overpriced. "And they weren't. It was a focus issue. We were winding down McCaw Cellular, and I suppose that was part of the excuse,” reported Fortune.2

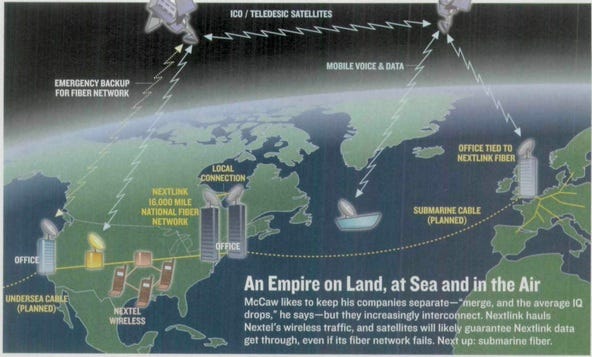

The “Nexts”

McCaw pieced together a vision of global communication including cellular, broadband data, fiber, and satellites. Three of his companies were the ‘Nexts’: Nextel, Nextlink, NextNet. Only his satellite venture, Teledesic, stood out by name.

"The revolution is here. People need high-capacity networks to homes, to remote locations, to farms, to villages that have never had fiber and won't for a long time. It's pretty obvious that there's a need, and that demand will build," he told Fortune in 1996.

“You arrive at moments in time when an entrepreneur, a technology, and the needs of people coincide. You get serendipity every once in a while. You try to be willing to accept it when it works on your behalf."

Nextel, originally called FleetCall, carved out a niche in the wireless space by using spectrum that had been used by taxi radio dispatch and paging operators. The company’s handsets offered a push-to-call “walkie talkie” function which was valued by its fleet customers. The company needed capital to transition from analog to digital, and in 1995 McCaw invested $1.1 billion. He brought in Daniel Akerson from MCI to turn around the company. They decreased the reliance on fleets and broadened the base of business customers who could connect large groups of workers. In 2005, Nextel merged with Sprint in a $35 billion deal.

McCaw had retained some assets from the sale to AT&T with which he started building Nextlink, initially as a provider of local phone services. The company aimed to become a major internet access provider and started investing in fiber. In 2000 it was renamed XO Communications and Akerson from Nextel took over as CEO.

Teledesic

McCaw’s most ambitious project was Teledesic, a network of low earth orbit satellites. It was the 1990s version of Elon Musk’s Starlink, and had initially been funded by McCaw Cellular. With the sale to AT&T, that funding source disappeared:

"I stepped in and said, if you won't support it, I'll put the money in myself. But if I'm going to do that, then I'm going to take it and run it my way. I'll be the CEO, and all the things you are when you actually put your own money in. Whoo! What a scary project!"

What had started out as an effort to provide wireless telephony in rural, hard-to-reach areas, evolved into the ambition to provide global coverage with data connectivity. In 1994, the plan was to launch 840 satellites, more than had been launched in all history until that point. The cost for the project was budgeted at $9 billion. McCaw raised additional capital from his friend Bill Gates and Saudi Prince Alwaleed bin Talal.

“Typical Craig," laughs his friend Wayne Perry, former president of McCaw Cellular, former CEO of XO, and an advisor to McCaw since 1975. "Leave it to him to try something greater than the sum of the whole world's experience.”

Gates commented, "I wouldn't have invested in Teledesic unless Craig was involved. Craig is an amazing person. He thinks ahead of the pack and understands the communications business and where it's going better than anyone I know."

Capital Starvation: The Bubble Bursts

"The way things are going in the industry; it feels as though I'm on an episode of Survivor and could be voted off the island at any minute."

McCaw’s fortune and ambitions took a serious hit when the dotcom and telecom bubbles collapsed. Fortune estimated that his wealth shrunk from $13 billion to $2 billion as stocks declined.

Nextlink/XO Communications was battered as overinvestment in fiber capacity and technological improvements led to a collapse in the price for bandwidth. Along with many of its competitors it ended up in bankruptcy. Tren Griffin wrote: “Craig McCaw said to me often during this period: 'You are always at the mercy of your stupidest competitors.' And in this case, there were scores of competitors.”

In 1998, Teledesic scaled back to 288 satellites as competing satellite ventures started to struggle. With Iridium and Globalstar heading towards bankruptcy, McCaw was eventually forced to abandon Teledesic. At the last moment he decided against investing in the distressed Iridium. Its satellites were already outdated and did not offer enough bandwidth to be competitive.

In the middle of the dotcom bust in 2002, a somber McCaw looked out at Seattle’s Puget Sound and Mount Olympus: "It's optimistic," he said cryptically, pointing into the gray skies. Asked to elaborate, McCaw paused. "I like looking towards the west. It symbolizes possibility. It helps me think about the future."

In a speech to the Federal Communications Bar Association in 2002 he described the environment:

“Many of the most highly touted telecom stocks of the late '90s are now more than 90 per cent off their highs. Even giants like Intel and Cisco have seen their market caps plummet. The strongest CLECs are trying to restructure through bankruptcy; the weaker ones are already gone. All of this has created not just red ink for investors, but pink slips for employees. All of these problems have led to a critical shortage of capital. Just as investors irrationally threw money at bad business plans two or three years ago, they now irrationally withhold capital from promising start-ups with solid business plans. The resulting environment is one of total capital starvation. The only business opportunities being saved are the safe bets — the ones where the biggest companies sell the lowest-risk, most me-too services in the largest, most lucrative markets. All the more innovative — and therefore riskier — opportunities are left to wither on the vine.”

Despite the setback, McCaw remained involved in the wireless industry. A friend joked “Craig never met a frequency he did not like.” “Nobody has fulfilled the dream of what mobile broadband could be,” McCaw said in 2007 when he invested in Clearwire. The company invested billions in 2.5GHz spectrum in a bet the FCC would permit the use for wireless broadband. After the approval, the value of the spectrum soared by an estimated four to ten times. Clearwire proceeded to build out an early 4G network based on WiMAX technology and partnered with Sprint Nextel. However, AT&T and Verizon eventually launched their own 4G LTE networks and Clearwire ended up being acquired by Sprint.

Conclusion and Lessons

To borrow a phrase from Jeff Bezos, McCaw leaned heavily into the future all his life. He was able to clearly see the value that wireless technology created for consumers and the demand that would be unlocked as costs decreased. Today we have nearly arrived at the destination he envisioned some three decades ago: global access to wireless communication and data that allows everyone to participate in one community and marketplace.

McCaw operated in industries that required enormous upfront investment for licenses and physical infrastructure. The combination of leverage and commodity services meant that he eventually found himself “at the mercy of the stupidest competitor.”

I kept wondering about his ability to raise capital. There were no examples of grand showmanship. Instead, he had conviction, displayed relentless focus, and had as much skin in the game as anyone. And he knew how to pitch different audiences. Banks were happy because he cared deeply about optimizing cash flow and had a CFO who spoke their language. Regulators wanted an operator who would make their constituents happy by investing in service and reach. McCaw was a missionary with the self-awareness to find believers who made up for his weaknesses. He serves as an example that the best salespeople don’t appear to be selling at all. They just let you see the world through their eyes and invite you to join the vision. When you pick up your phone and walk around today, remember how McCaw’s bet of a lifetime made it possible. And use the freedom to pursue an ambitious bet of your own.

Recognizing value: Tren Griffin pointed out how McCaw was a genius at spotting products and services that provided such value to the consumer that they seemed inevitable. In his mind, the landline phone system turned people into “slaves to places.” The old system was stupid to him: "Alexander Graham Bell put cotton in the ringer of his phone. The system is really dumb. Anytime someone sends an electrical burst down the wires, all the phones in your house ring."

Courage: When McCaw saw a tremendously undervalued asset, he didn’t just take a stake. He bet his entire fortune on it. McCaw viewed himself as an outsider and was not afraid to look foolish. As he said:

“A government policy premised on waiting for the largest players to innovate is a recipe for stagnation. It has never been the established players that have taken risks or bet on innovative products and services. Instead, it's the risk-takers, the 'crackpots,' if you will, who have been the architects of the largest, most cutting-edge telecom infrastructure on the planet.”

Self-Awareness: McCaw understood that his strength was seeing the big picture earlier and with higher conviction than others. He had also witnessed how a lack of organizational rigor could undermine and unravel a business empire. In response to this he hired strong managers to make up for his weaknesses, particularly legal, financial, and operational talent.

Focus and Speed: It is notable that McCaw made a fortune by being focused on one or two businesses at a time: first cable and paging, then cellular. In each case he put in place a system that allowed his team to close on acquisitions quickly, giving him an advantage over bureaucratic incumbents. During the telecom boom he spread himself thin. That period was most reminiscent of his father’s empire-building and ended with another set of hard-earned lessons.

"If you're worried about your legacy, you're worried about the past. I'd rather not focus on the past."

Further Reading:

I highly recommend Tren Griffin’s lessons from working with Craig McCaw. He also wrote about his experience at Teledesic.

For another story from the telecom bubble, check out my thread on Level 3 Communications, a company forged by Walter Scott of Kiewit (of Berkshire Hathaway Kiewit Plaza fame). Tren Griffin also penned an excellent piece on the bubble. Lastly, Modest Proposal collected lots of helpful data on the bubble. Federal Reserve research paper on the telecom boom and bust. Series of articles on McCaw in the April 4, 1993, April 8, 1993, August 17, 1993. Speech to Federal Communications Bar, 2002. Brief speech to the Horatio Alger Association. Brief bio.

'Craig's Higher Calling,' Forbes, 2000

‘Craig McCaw sees an Internet in the sky,’ Fortune, 1996