Workshop Note: Bear Market Traps🐻

"Play stupid games, win stupid prizes."

One of the challenges of bear markets is that they grab our attention. They can be corrosive to our behaviors and tempt us to diverge from the game we play.

First we get shamed for our past overconfidence and greed (I write this as I look at a position of SPAC warrants trade at pennies on the dollar). No problem. We can mentally write off the losses and are ready to move on.

But the volatility continues and the headlines get frantic. Fear is contagious. We instinctively want to avoid more pain. At the same time, a long bull market has conditioned us that things snap back, that the dip must be bought. Who wants to be left behind when the party continues?

As the market speeds up, it’s tempting to think that we should speed up as well. And sure, if you’re a great trader you might be able to shoot first. As Jeremy Irons tells Kevin Spacey in Margin Call: “If you're the first out of the door, that's not called panicking.”

It’s what David Tepper did in 1998. According to the book The Chastening, Tepper cut his risk very quickly:

“The problem was, you had had this idea that with the IMF, there was some safety net underneath the market, but if Russia could default, why couldn’t Brazil default, and why couldn’t Mexico default, and why couldn’t others default?”

“If you’re doing portfolio management, and there’s a 25 percent probability something’s going to [negatively] affect the price of something you hold, you sell. No matter what. I don’t give a shit if it’s affected or not at the end of the day. It’s Just a probability game. So we moved pretty fast in August.”

Even so, his fund was battered 1998. It seems he had a quick trigger finger again this year. Last week, he told Jim Cramer he’d covered his Nasdaq short. And that he’d be a buyer “10% lower.”

Disclaimer: I write for entertainment purposes only. The information in this publication is not intended to constitute investment advice and is not designed to meet your personal financial situation. Consult your financial adviser to understand whether any investment is suitable for your specific needs and before making investment decisions. I may, from time to time, have positions in the securities covered in my articles. This is not a recommendation to buy or sell securities.

But here we are. The time for that first move has long passed. In fact, a lot of froth has come off the market already. Retail’s favorite stocks have retraced their outperformance. Goldman Sachs' non-profitable tech stock index has returned to earth. Sentiment is bad (though I doubt it’s actually at the 1987 lows; lower than in 2008 and 2009?!).

Tech-focused hedge funds, the stars of the last couple of years, have cut a lot of positions. Dan Loeb just published his quarterly letter and noted his net exposure was “lower … than at any time during the last 10 years.” He also started adding back single name shorts. But even shorting is not straightforward in a bear market.

“I’ve done well in bear markets. I’d love to sit here and tell you I made it shorting stocks. It’s always very difficult in a bear market. They don’t trade with rhythm, you get these vicious rallies, you get squeezed out of shorts and people play all sorts of games. I always made it in Treasuries, because Treasury yields would go down dramatically.” Stanley Druckenmiller

Unfortunately, Treasuries haven’t served as protection in this market - it’s been one of the worst times for a standard 60/40 portfolio. Paul Tudor Jones said on CNBC that he couldn’t think of a “worse environment than where we are right now for financial asset” and that “clearly you don’t want to own bonds and stocks.”

Keep an open mind and don’t get overconfident

“This is a humbling market. And I — it’s not particular to Cathie Wood. But I think I’ve seen a number of cases where people are way too confident about the future.” Boaz Weinstein

Here’s a paradox. If macro uncertainty is increasing, you should be less confident in making bets. Time to play defense. However, if you’re suddenly spending a lot of time ingesting macro research, confidence in your judgements may be increasing.

I think it’s especially important to combat recency bias and not anchor our expectations to the experience of the last decade.

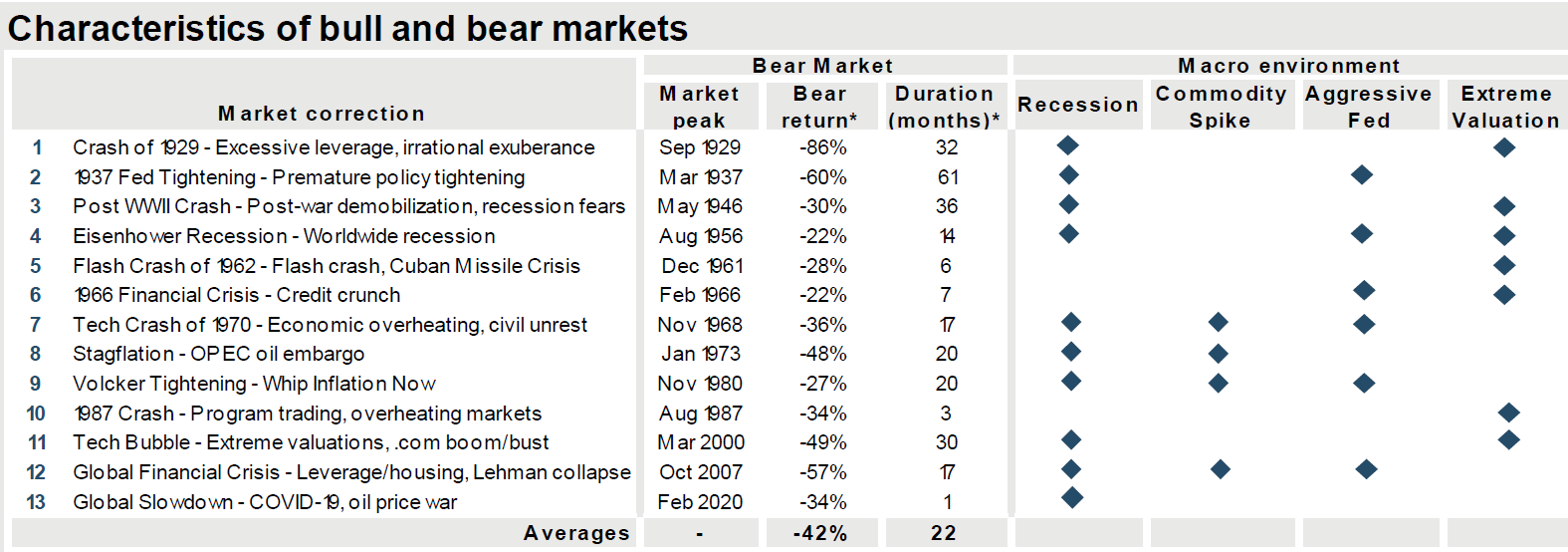

Are we going to enter an extended bear market? I don’t know but it’s certainly possible. Check out the below table courtesy of JP Morgan. 22 months, the average duration of bear markets in the sample, is a long time to retain faith. The point is not to try and predict whether this will happen but to have a portfolio that will let you sleep at night and stick with your strategy in case it does.

It’s also worth considering that in a different market regime different strategies will perform well.

“If there was a strategy that I would want to employ right now, if someone put a gun to my head, I’d say simple trend-following strategies. They are not too popular today. They will probably do very well in the next 5-10 years.” Paul Tudor Jones

Create the right structures

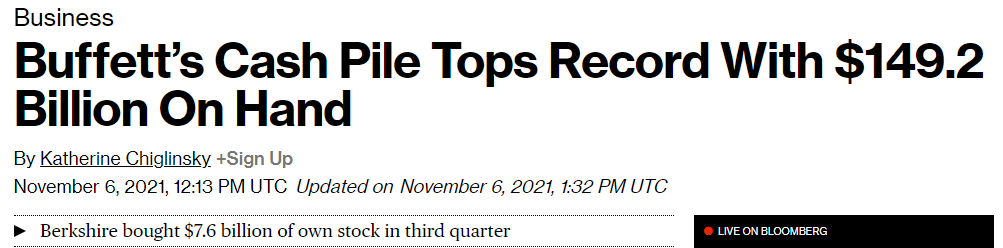

I wish I’d paid more attention when the investor with the longest track record built up a lot of cash. Which he is now putting some to work (in energy stocks and financials).

But it’s more interesting to consider why he was able to do this. Why can Buffett comfortably sit on the sidelines for extended periods of time?

First, he put the right structure in place. The first time he found himself in this position, he shut down his partnership in 1969 noting that he was “out of step with present conditions.” Buffett knew that running a fund incentivized him to play a game he didn’t like. It’s hard to sit on cash.

Instead, he acquired control of a deeply undervalued company to use it as his permanent capital base. He removed the risk and distraction of investors pulling their capital due to underperformance and created optionality by having an asset-rich balance sheet and ongoing cash flows to deploy once the market turned and offered bargains.

He commented on the importance of this structure as well as the second issue which is behavioral.

“It will bore most people and certainly boredom is a problem with most professional money managers. If they sit out an inning or two, not only do they get somewhat antsy, but their clients start yelling, “Swing you bum,” from the stands. And that’s very tough for people to do.”

On a recent podcast, Boaz Weinstein of Saba Capital talked about his internship at Goldman Sachs where he worked with David Tepper:

Weinstein: “They would make bets. He'd yell over at Jim Zelter, “How many synagogues do you think there are in Montana?”

“Not more than three.”

“Boaz, go to the library and figure it out.”

“Were interest rates ever negative, bets of all kinds. I would learn a lot through osmosis.”

Ritholtz: “The Salomon Brothers version was Liar’s Poker played with dollar bills. At Goldman, it was a trivia contest?”

Weinstein: “You know, traders like to bet.”

That last sentence stuck with me. Traders like to place bets. That’s why they became traders in the first place. But sometimes it’s a bad time to make bets and you’re best off minimizing your activity. That’s what Buffett meant when he talked about not hearing so many stories in Omaha.

“You can think here. You can think better about the market; you don’t hear so many stories, and you can just sit and look at the stock on the desk in front of you. You can think about a lot of things.”

Stick to your game

That said, the internet has collapsed distances and we’re all inundated with stories and noise. And because I like to study great traders, I get my fair share of them. Last year, Druckenmiller called markets the “everything bubble”:

It’s tempting then to revisit his market framework around valuation, liquidity, and technical indicators. The picture isn’t pretty. Overall valuations are still high (though of course some areas have come down significantly) and the Fed is tightening…

But hold on. Before spending more time with this, it’s worth considering the context. Agile traders like Druckenmiller can change their opinion and portfolio in a matter of days in a volatile market. He is playing the macro trading game to win. Without being as immersed in it and dedicated to it as he is, one can only play it to not lose.

“I think we’re in one of those very difficult periods where simple capital preservation is I think the most important thing we can strive for. I don’t know if it’s going to be one of those periods where you’re actually trying to make money.” Paul Tudor Jones

It’s ok to dial back risk when markets reach extremes. Even Jack Bogle did it.

“But, in late 1999, concerned about the (obviously) speculative level of stock prices, I reduced my equities to about 35% of assets, thereby increasing my bond position to about 65%.”

But that is not an activity one has to dedicate a lot of time to. You don’t need to engage in the futile exercise of trying to predict a complex adaptive system. Or as Bill Ackman would say: what is the return on brain damage here?

It’s very important to consider in which areas of our lives an increase in effort and attention will lead to better outcomes. For most of us, trading based on macro is not one of those areas.

It’s ok to listen to legendary investors and traders opine on the market and say “interesting, but I don’t know.” It’s important to reconsider what amount of risk one is comfortable with and to make adjustments if needed. And it’s good to keep an open mind as to what strategies and assets are more likely to perform well in the future. But because macro is “the raw material for story-telling,” as Kris Abdelmessih so eloquently put it, “it’s more likely to give you brainworms by beefing up your priors. It will calcify hunches into commandments when the evidence only merits ‘things to learn more about.’”

It’s crucial to not obsess but shift back to activities in which our investment of time does more reliably translate into value.

Global macro is also an area in which even experienced traders routinely get tripped up. Victor Niederhoffer, a trader who worked for George Soros and had his own fund, once recounted staying at Soros’s Hamptons home at the end of summer. As Niederhoffer walked into the water, Soros shouted:

"Look at those waves. Stay out, they're too big for you."

"Well, that's the job of a speculator, to stand in the way of the big waves."

"That's your big problem. You don't know when to stand away when the big waves are coming."

"And he was right."

Two years later, Niederhoffer blew up his fund during the Asian financial crisis.