When to listen to markets? Druckenmiller, Diversity, and the Debate over 1987

"The only good economist I have found is the stock market. People say it has predicted seven out of the last four recessions. That’s still better than any economist I know.” Stanley Druckenmiller

Hello everyone.

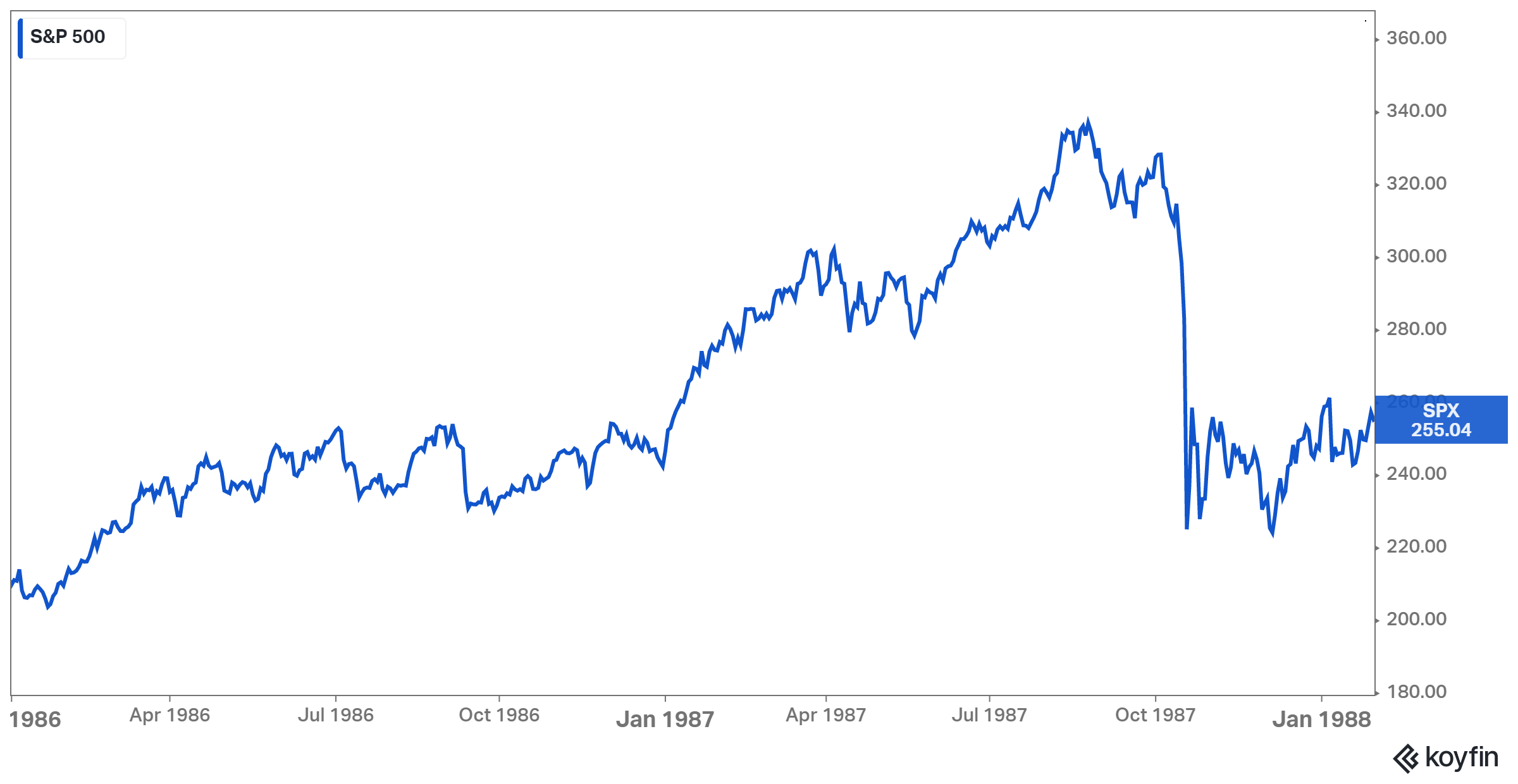

After my last piece on Stanley Druckenmiller, I tried to put myself into the shoes of an investor in late 1987 or early 1988. Druckenmiller observed with admiration that George Soros was able to bounce back from his humiliating loss quickly - and in contrast to many other investors:

“Just about every manager I knew who was caught in the crash became almost comatose afterwards. George took a bigger hit than any of them. Within two weeks, he put on a massive leveraged dollar position.”

Veterans like Michael Steinhardt recalled feeling “so depressed that fall that I did not want to go on. My confidence was shaken. I felt alone.”

Magazine covers weren’t exactly inspiring confidence either:

The key question was whether the crash itself had any meaning. If the stock market discounted the future, was it signaling a downturn? Or was the crash a purely technical and emotional outlier event?

This question touches on a cornerstone of Druckenmiller’s philosophy of having an open mind and looking at the market for signals:

“One of my strengths over the years was having deep respect for the markets and using the markets to predict the economy, and particularly using internal groups within the market to make predictions. And I think I was always open minded enough and had enough humility that if those signals challenged my opinion, I went back to the drawing board and made sure things weren't changing.”

It presents a tension: when to use the market for guidance and when to lean against it. Soros also commented on being often and incorrectly “considered a contrarian.” Instead, he was “very cautious about going against the herd.” He considered himself a trend follower but “all the time I am aware that I am a member of a herd and I am on the lookout for inflection points.”

In the summer of 1987, Druckenmiller took a contrarian stance against the bull market. In early 1988, he was again bearish because the market had crashed:

“I do know that every time the stock market has gone down 30% in this century, we’ve had a recession. The only good economist I have found is the stock market. To people who say it has predicted seven out of the last four recessions, or whatever, my response is that it’s still a lot better than any of the other economists I know.”

By then, he was managing more than $3 billion across five different funds at Dreyfus and finally getting attention. He was still young and still spoke openly to the press. In February 1988, he appeared in Fortune in a brief interview titled “Battening Down for a Recession.” In March, he sat down with Barron’s for an extensive conversation titled “Short’s Story.”

Both articles offer insights into his philosophy and I’m going share more quotes in a separate post. In this piece I’m going to focus on his idea of using the market as a leading leading indicator.

Druckenmiller turned out to be wrong on the market (it recovered and did not make new lows) and wrong, or at least very early, in anticipating a recession (did not happen until late 1990). This does necessarily mean that his decision was wrong as we can’t judge it by the outcome alone (a mistake that Annie Duke calls “resulting”).

I think his approach of looking to the market for guidance can be useful but, counterintuitively, it likely works better after the crash. Why? Because a diversity of opinions has been restored.

Market efficiency and diversity

When thinking about market efficiency, I learned from Michael Mauboussin to consider the market a complex adaptive system (something he learned from the scientists at the Santa Fe Institute). Mauboussin articulated his view in a paper from 2002 (my twitter notes).

From his book More Than You Know:

“Investors with different investment styles and time horizons (adaptive decision rules) trade with one another (aggregation), and we see fat-tail price distributions (nonlinearity) and imitation (feedback loops).”

“An example of this phenomenon is an ant colony. If you were to “interview” any single ant about what it does, you would hear a narrowly defined task or set of tasks. However, because of the interaction of all the ants, a functional and adaptive colony emerges. In capital markets language, the behavior of the market “emerges” from the interactions of investors. This is what Adam Smith called the “invisible hand.” Revisiting Market Efficiency

This means that cause and effect thinking is often futile because “large-scale changes can come from small-scale inputs.” It can be impossible to pinpoint the exact reason for a market move. Mauboussin pointed to the Brady Commission which failed to pinpoint an exact cause for the 1987 crash.

We can observe this every day in financial news when headlines are written to explain the market (narrative follows price).

“On Wall Street today, news of lower interest rates sent the stock market up, but then the expectation that these rates would be inflationary sent the market down, until the realization that lower rates might stimulate the sluggish economy pushed the market up, before it ultimately went down on fears that an overheated economy would lead to a reimposition of higher interest rates." Mankoff, 1981, The New Yorker

Importantly, for the system to function well, agents must follow a diversity of decision rules which “compete with one another based on their ‘fitness,’ with the most effective rules surviving.” This is how the system adapts over time. If that diversity disappears in a “diversity breakdown,” Mauboussin wrote, markets become “susceptible to inefficiency.”

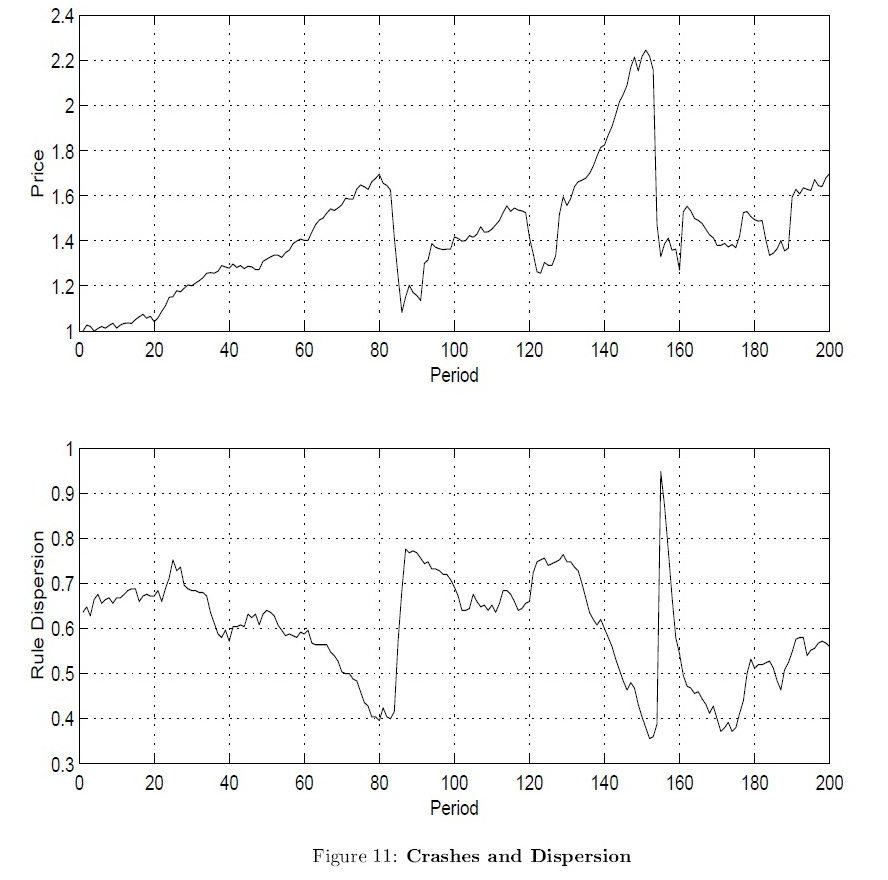

Mauboussin highlighted to me a paper by Blake LeBaron which highlighted this dynamic. LeBaron created a model in which a population of agents trade one asset (representing the market) based on a diverse set of decision rules (investment strategies). Agents had different time horizons and picked strategies based on performance over their respective timeframes (some are short-term traders, some long-term investors). Over time, more and more agents piled into similar strategies. Trends accelerated. Then the market crashed.

The top chart shows the market price: a positive long-term return with boom-bust episodes.

The bottom chart shows that dispersion among strategies declined before each crash and was restored through the sell-off.

“A simple story is starting to emerge,” Lebaron wrote. “During the run up to a crash population diversity falls. Agents begin to use very similar trading strategies as their common good performance begins to self-reinforces. This makes the population very brittle in that a small reduction in the demand for shares could have a strong destabilizing impact on the market.”

When the sell-off occurs, “traders have a hard time finding anyone to sell to” because “everyone else is following very similar strategies.”

Even though the market looks more treacherous after the crash (recency bias), it should be more robust and efficient because a diversity of opinions has been restored.

The raging debate

The 1988 Barron’s Roundtable and other investor interviews around that time illustrate what that diversity of opinions looked like. There was a sharp divide between bulls and bears. Macro thinkers tended to fall into the bearish camp, believing that the market was signaling a brutal downturn. Many bottom-up investors however found a contrarian buying opportunity.

Paul Tudor Jones, by then famous for ‘predicting’ the crash, was a vocal bear (I wrote about it here). He was concerned about a “worldwide depression like the early Thirties" and the "future welfare of the world.”

“The only real operative historical parallel to what we have right now is the Twenties. And the similarities are so striking, so rampant and so numerous that one has to use that as a basis.”

“Go back and read Barron's. It's the same exact newsprint with different names and characters.”

He was convinced the stock market was leading the economy:

"Earnings can disappear overnight if the market makes new lows. The stock market is a leading indicator."

Marty Zweig, famous for his appearance on Wall Street Week the weekend before the crash argued in Fortune that "we have never had a decline of more than 30% during peacetime that wasn't followed by a recession or depression" (sounds like he and Druckenmiller were sharing notes..). A mild slowdown on the other hand would be positive because stocks would be bolstered by lower rates.

There were other bears, including Michael Price who said he “couldn't be more bearish" and was prepared for “new lows” and possibly “another 30% off the Dow.” I think his view may have been colored by wishful thinking - the value investor’s hope to pick up shares even cheaper. While Price was already finding stocks that were “beaten up,” he was a “seller on strength” and excited for new lows to “start buying” again.

Felix Zulauf announced that “the world changed in the fall of '87. A bear market started that will probably last several years.” The first downward move was being met with disbelief, he argued, because “markets are leading economic events." He viewed “any improvement in the stock market” as a “countertrend move.”

Jim Rogers, formerly Soros’s analyst and right hand, expected a rally followed by “the worst bear market since 1937.” The dollar was doomed and there was going to be a bear market to “wipe out most people in the financial community, most investors around the world.”

The bulls were led by Peter Lynch who seemed to revel in his optimism:

“The economy is great.”

“People said oil was going to go to $100, and then we were going to have a depression. The same people said oil was going to go to $5, and we were going to have a depression.”

“There's always something to worry about. It's garbage to worry about these things.”

“People dump all over this country, it's just absurd.”

Like him, stock pickers found value and came out rather bullish, particularly in industries that benefited from the lower dollar or that that been restructured and consolidated (Mario Gabelli: “I see significant gains in earnings for these types of companies” and John Neff: “once you get to a fairly valued market, you are pretty well obligated to get fully invested.”)

I’ve written before about how Julian Robertson, whose fund suffered badly in 1987, reached out to CEOs and portfolio companies and was bullish based on a belief the real economy was doing well:

“I don’t talk to anybody in industrial America who isn’t absolutely tonning it. I’m talking about smokestack America. They are making a fortune.”

“I am not quite sure what will happen next… But I know that Ford Motor Co. is a value at four times earnings and twice cash flow.”

“Things are setting themselves up for one of the major buying opportunities of our time. Industrial America has not been this competitive with the rest of the world in years.”

Bill Miller described 1987 as a "liquidity implosion" in which an overvalued stock market collided with an accelerating economy. In the aftermath, "rapid easing should neutralize the economic shock effect." This was different from 1929, when “an over-valued stock market was finally brought down by a weak economy.” Miller described the economy as “expanding rapidly,” driven by strong exports.

And Druckenmiller?

“We see an economy that's in a lot of trouble. Auto sales and housing starts are weak -- in fact, the entire consumer sector. The economy appears strong because lagging indicators like capital spending still appear healthy. What would make us more bullish would be the recognition that we are in a recession. That would lead to lower stock valuations and buying opportunities.”

My take

My first takeaway is to recognize the sheer difficulty of getting these big picture calls right.

There were so many moving pieces that seemed important at the time: the deficit, high unemployment and weak growth in Europe, competition from Japan, the dying steel and car industries, high debt levels, an impending election, higher taxes, a lower dollar, earnings, valuations … You could find experienced investors on both sides of the argument and with widely divergent views on the economy. Everyone views the market through their own unique prism and what information they focused on seemed to mostly reflect their existing biases.

In this case case, it was important to understand who was doing primary work (talking to companies) to figure out how the real economy was doing. Which is not to say that the bottom-up view is superior or always right. We can probably find examples in which the the market flashed warning signs and stock pickers got caught off guard (maybe 2007?). And it’s important to keep in mind that macro traders like Druckenmiller or Paul Tudor Jones change their minds quickly and are not wedded to their public comments.

But I have more respect now for investors who focus on what is knowable. I understand why Peter Lynch commented that he would “love to know if we're going to have a recession. The odds of me figuring that out - I'm never going to.”

Or Ron Baron who said: "I don't predict the market or the economy. I am able to find incredible values, like I've never found before in my career." It must have been very tempting to become a tourist in macro narratives (as may have happened to Michael Price who was expecting - hoping for - lower prices to buy).

My second takeaway is that the presence of this heated debate itself was valuable. It meant that a diversity of opinions had been restored. It could indicate that the market was less brittle than before the crash - that it was a moment to follow the market’s direction, rather than bet against it.

It was great to read how diverse the opinions of even the most successful minds in investing were at that time - it just puts everything into perspective, especially when one is again tempted to throw all humbleness overboard and try to predict the next turn of the market.

Hi Frederik,

I just wanted to mention that I link your piece here in this:

https://www.libertyrpf.com/p/272-shopify-vs-amazon-logistics-microsoft

Cheers! 💚 🥃