What George Soros and Steve Jobs Can Teach Us About EV Stocks

Finding reflexivity in unexpected places

“Tell the truth, but make the truth fascinating” David Ogilvy

“A boom/bust process occurs only when market prices find a way to influence the so-called fundamentals that are supposed to be reflected in market prices." George Soros

“In [Jobs’s] presence, reality is malleable. He can convince anyone of practically anything. It wears off when he’s not around, but it makes it hard to have realistic schedules.” Apple engineer Bud Tribble on Steve Jobs

“Nikola is one of the most innovative companies in the world. General Motors is one of the top engineering and manufacturing companies in the world. You couldn’t dream of a better partnership than this” Nikola Founder Trevor Milton

What is the connection between electric vehicle stocks, George Soros, and Steve Jobs’s raid on Xerox PARC? Reflexivity.

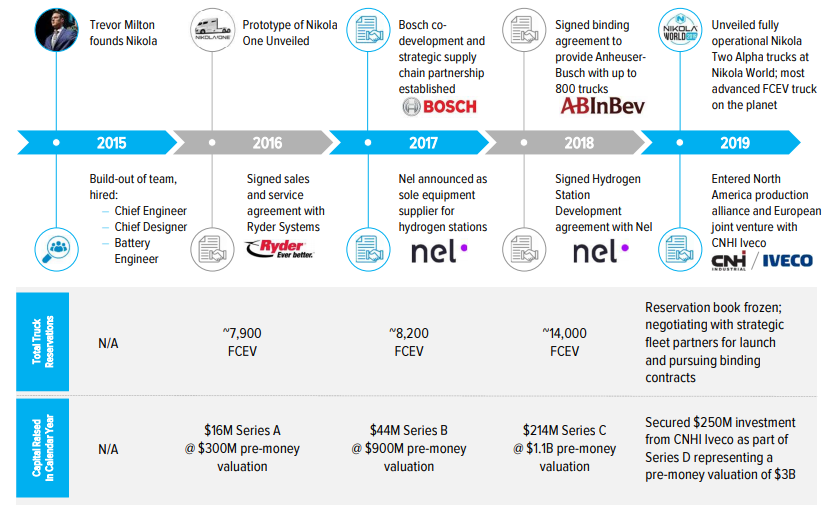

A couple of days ago, Nikola Corp. entered into a strategic deal with General Motors, whereby GM will receive a $2 billion stake (priced at $41.93 a share) in return for engineering, building, and supplying components for Nikola’s Badger SUV (basically for doing almost all the work). At that price, Nikola’s existing equity was valued at more than $15 billion – a steep increase from the $4 billion at the time of the SPAC merger.

Sure, GM expects some future revenue from this agreement. But access to GM’s EV division, valued by some analysts between $20-100 billion, will allow Nikola to unlock whatever value there may be in its designs and brand. Investor excitement about the future of electric vehicles (and a market environment of abundant liquidity) allowed pre-revenue Nikola to offer $2 billion of stock to GM without completely diluting existing shareholders. In a similar vein, Tesla was recently able to raise $5 billion in fresh capital with minimal dilution.

I’m not here to argue about the fair value of either company. If you believe the short sellers, Nikola may not be worth all that much (I do recommend reading that report if you’re in any way involved in the stock). The bull case seems to be a “capital light Tesla 2.0.”

Nikola is definitely bringing one thing to the table: it’s story. It’s cool and exciting. Perhaps GM hopes some of the glitter will rub off?

No matter how this plays out, it’s an example of reflexivity at work: of market perception changing fundamentals. And nobody has thought more about the interaction between reality and perception in financial markets than George Soros.

Is this worth $15 billion? George, what is going on here?!

Soros used the concept of reflexivity to explain “boom-bust sequences,” the blowing and popping of bubbles.

Reflexivity can create a bubble, if "the prevailing bias and the prevailing trend reinforce each other until the gap between them becomes so wide that it brings a catastrophic collapse."

In other words, if an investor bias (a positive or negative misperception of reality) meets an existing trend and in turn reinforces said trend, the resulting self-reinforcing sequence can accelerate until the gap between perception (valuation) and reality (value) reaches bubble-like proportions. To Soros, this feedback loop is a key ingredient to bubbles. Investor sentiment alone is not enough.

From the Alchemy of Finance: “market valuations are always distorted” and “prices must have some effect on the fundamentals, in order to create boom/bust pattern.”

It’s the observer effect at work in financial markets.

“What makes the analysis so difficult is that the participants’ views are part of the situation to which they relate.” George Soros

Soros first applied this concept to the conglomerate boom of the 1960’s. Then he saw it at work in mortgage REITs and banks. Higher valuations allowed the companies to accelerate the underlying trend (ie. to acquire more assets to boost earnings growth). Investors extrapolated the acceleration in the underlying trend, feeding it back into rising valuations.

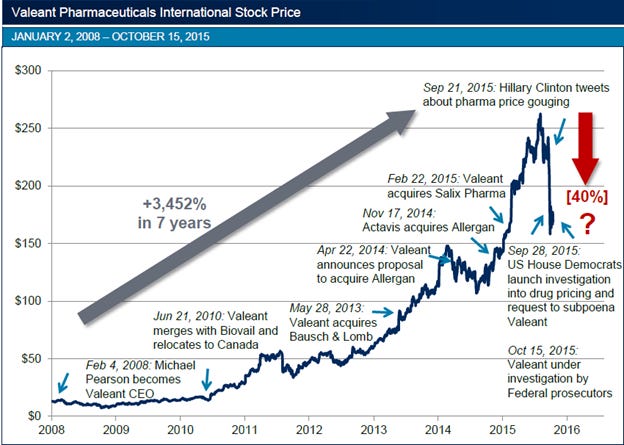

More recently, we saw this play out with acquisitive “platform” companies such as Valeant Pharmaceuticals. Check out this excellent presentation from 2015 for some fantastic charts on past booms and the analogy with the platform companies.

While Soros started his career covering individual stocks, over time he gravitated to thematic bets and other asset classes such as currencies. That’s where his framework was most applicable and he could trade boom-bust sequences both during their inflation and collapse.

Fundamental investors on the other hand often find themselves drawn to the idea of shorting “concept stocks” like Nikola once they discover a glaring divergence between valuation and fundamentals, between perception and reality.

However, the longer this gap persists, the greater an opportunity it presents for creative management teams to create value for shareholders by exploiting market (mis)perception. Examples would be raising equity or debt capital at favorable terms, acquiring assets with stock, entering into partnerships based on a perception of success, and even attracting talent.

We can find this pattern at work in unexpected places, such as Silicon Valley at the birth of personal computing.

In 1979, Steve Jobs learned about Xerox's Palo Alto Research Center (PARC). He and a team of Apple colleagues would visit the facility several times, an event that altered the course of history for both Apple and the computer industry.

While the advanced research at PARC was proprietary, the facility itself was not a secret. In fact, thousands of visitors had been welcomed since its inception in 1970. As a Xerox shareholder, you could have read about it in the annual report:

From the 1977 Xerox Annual Report:

"In 1971, the Palo Alto Research Center was established in that northern California heartland of data-processing sciences and scientists. More than 200 professional people from many countries conduct the studies that are essential to the company's development of digital equipment and office methods for the future."

"The Palo Alto Center does fundamental research in such matters as new information-storing substances and technologies, new memory formats, fiber optics, laser input and output scanning, new integrated circuit technologies, and many more."

"A prototype information system involving linked, interactive machines is in productive and routine use at the Palo Alto Center now. Parts of the system have been used experimentally by children in a nearby public school system, even in the elementary grades, to draw pictures and compose music and do other things according to the instructions devised for the machines by the children themselves."

That's right, even schoolchildren had already seen some of the tech and apparently used the graphical user interface (GUI). And yet, Xerox was slow to act on the breakthrough research done at PARC.

“Our communication with the corporate offices was not so much limited by the distance. I think it was really limited on both our ends by our different visions for the future and about how to commercialize the things we developed.” David Biegelsen, former PARC research fellow

While PARC’s researchers were frustrated by the lack of commercialization by Xerox’s East Coast-based management, they knew their technology was incredibly valuable. They weren’t keen on showing their most advanced ideas to visitors, let alone to a competitor like Steve Jobs.

This is where reflexivity kicked in.

Apple was a hot startup on its way to go public. Its equity was highly desirable. It wasn’t just an attractive risk-reward investment, it was sexy from a career standpoint. Who wouldn’t want to have “Apple pre-IPO investor” on their track record?

Apple Computer IPO Prospectus:

Apple’s growth pre-IPO:

Jobs ingeniously used this valuable bargaining chip: he opened Apple's latest funding round to Xerox: "I will let you invest a million dollars in Apple if you will open the kimono at PARC." Xerox accepted.

When the Apple team first arrived at PARC, they were shown basic systems available to other visitors. It wasn’t the secret sauce Jobs was looking for. He called Xerox headquarters and scheduled a second visit.

Again, the PARC team tried to stonewall Jobs. Adele Goldberg, one of the researchers, remembered trying to keep their breakthrough technologies under wraps: "it was incredibly stupid, completely nuts, and I fought to prevent giving Jobs much of anything."

But Jobs knew he wasn’t getting what the was looking for. He shouted: "let's stop this bullshit." Then he placed another call to Xerox headquarters and asked the head of venture capital to intervene.

His persistence paid off. The Apple team was shown PARC’s work on personal computing, including the GUI and the mouse. The PARC team witnessed Jobs "hopping around so much I don't know how he actually saw most of the demo. But he did, because he kept asking questions."

"You're sitting on a gold mine," Jobs shouted. He returned to Apple, determined to leverage the intellectual capital being hoarded at PARC. The ideas would be implemented first in the Apple Lisa, then the Macintosh.

"It was like a veil being lifted from my eyes. I could see what the future of computing was destined to be."

"Xerox could have owned the entire computer industry," Jobs would later say.

Would you recognize a gold mine if it looked like this?

It’s an imperfect example because Xerox’s investment in Apple stock was not based on a complete misperception. It worked out well in the short-term, with the $1 million being worth more than $17 million at the time of Apple's IPO. In a way, the misperception was the misunderstanding of the relative value of upside in Apple stock and the research done at PARC.

Still, I think it is a useful illustration of how investor perception can alter reality by creating value at the underlying company.

In the longer term, Xerox’s failure to act decisively on its personal computing innovations led to a string of departures. The “PARC mafia” started companies such as Adobe, Pixar, and 3Com.

Peter Thiel wrote that a great company is a conspiracy to change the world, built around a secret hidden from the outside. Better yet, if investors perceive your secret to be highly valuable, you can use it to gain access to the secrets of others.

Warren Buffett once said he would rather analyze a stock before knowing its price to avoid anchoring bias. But most people aren’t like Buffett (obviously). For better or worse, they will use a company’s stock chart as a shorthand way to assess the health of the underlying business.

Up and to the right? That company is probably doing better than the one whose stock is making new lows every day. Not too dissimilar from a startup’s ability to raise capital at increasing valuations. If that pattern breaks, alarm bells go off. Of course, this kind of System 1 thinking can lead to serious errors in judgement, which is where an investor’s variant perception comes into play.

But it does make me appreciate CEOs who can communicate their company’s story to the markets in a way that benefits valuation and can kickstart a reflexive dynamic. In the words of Josh Wolfe:

“The single best trait of an entrepreneur is someone who can tell a story.”

Shareholders can benefit from reflexivity created by a storyteller CEO. And short sellers have to be mindful that the gap between perception and reality can be used to change reality. In the long-run, presumably, fundamentals will win out. In the short-run, it’s best to read up on Soros.