What Creates Opportunity?

“I have a friend who says, ‘The first rule of fishing is to fish where the fish are. And the second rule of fishing is to never forget the first rule.’” -Charlie Munger

Hello everyone,

What is a shared trait among three recent subjects: David Swensen, Seth Klarman, and Warren Buffett? Each one thought deeply about the game they played and the factors that created opportunities.

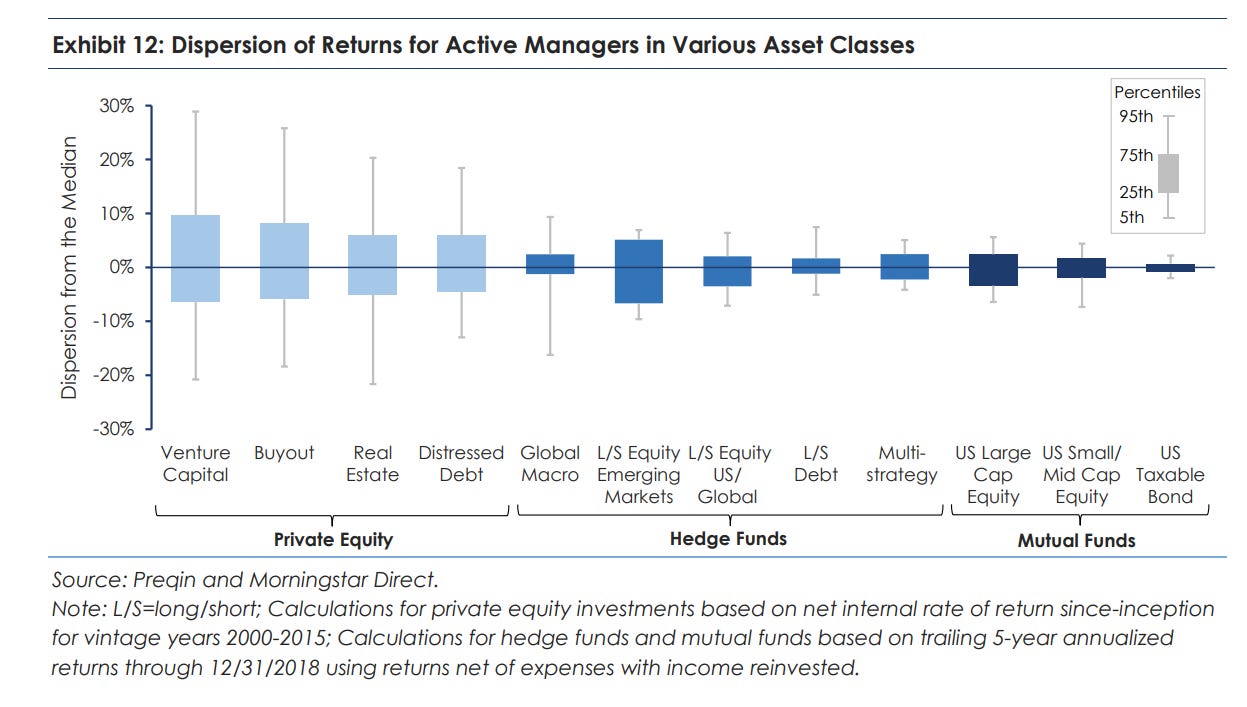

Seth Klarman described his philosophy as the search for “market inefficiency or imperfection” with examples like spin-offs created by “institutional constraints.” Swensen accepted steep fees for active management as long as he had conviction that the manager had sufficient skill and operated in an asset class with sufficient opportunity to overcome that fee burden. He looked for areas with enough dispersion of returns:

The game and opportunity set change over time. For example, the aggregate level of skill in the market has increased. The foreword to Pioneering Portfolio Management was written by Charlie Ellis, chairman of Yale’s investment committee, who also wrote The Loser’s Game, an essay on the Paradox of Skill in investing:

“Gifted, determined, ambitious professionals have come into investment management in such large numbers … that it may no longer be feasible for any of them to profit from the errors of all the others sufficiently often and by sufficient magnitude to beat the market averages.”

Or as Buffett said in 1998:

"The secret of life is weak competition. It’s way better to be in securities markets if you have a hundred IQ and everybody else operating has an 80, than if you have 140 and all the rest of them also have 140."

In Dave Rubenstein’s How to Invest Bruce Karsh of Oaktree called the late 80s and 90s the ‘halcyon days’ of distressed investing with “plenty of great opportunities and little in the way of competition.” Distressed debt “was much more inefficient.”

There’s a scene in HBO’s Industry, a show about a drug and sex-fueled London trading floor, that captures the idea well. The protagonist encounters the desk’s senior trader in the parking garage. After the trader parks his new Ferrari, he comments:

“I bought my motor off a recently divorced dad in Chingford. Distressed seller is key.”

It’s not complicated and some people live and breathe the mentality.

The game for each successful investor also changes with a growing capital base. Buffett famously commented on how small sums could be compounded at much higher returns.

“I can name a half a dozen people that I think could compound a million dollars — or at least they could earn 50 percent a year on a million dollars — have that as expectation, if they needed it.

You find small securities in your area of competence ... and occasionally little arbitrage situations. Very small things you are almost certain to make high returns on.”

Munger pushed back a little, highlighting how much the opportunity set had changed.

“What we did 40 or so years ago was, in some respects, more simple than what you’re going to have to do. We had it very easy, compared to you. It can still be done. But it’s harder now. You have to know more. I mean, just sifting through the manuals until you find something that’s selling at two times earnings, that won’t work for you.”

Distressed debt investors in particular face a cyclical ebb and flow of opportunities. Managing their capital appropriately became a valuable skill (it’s a little counterintuitive to think of them as market timers). Karsh again:

“I’m most proud of the fact that we picked the right time in the economic and distressed-debt cycles to raise our largest funds. … when the supply of distressed debt was most plentiful.”

While Buffett is locked out of most securities at this point, he managed to turn scale into an advantage on the right side of his balance sheet. The insurance operation benefited from Berkshire’s sizable fortress balance sheet with the ability to underwrite large, unusual, and long-tail risks. The structural advantage of his float leverage became the perfect complement to a long-term buy and hold strategy for great businesses at fair prices.

“There’s nothing like the pain of being in a lousy business to make you appreciate a good one. … How to play those business games — you learn a lot by trying. What you really learn is which ones to avoid.” Warren Buffett

The idea of understanding other players is most obvious in event-driven situations but it extends into other domains, for example global macro where the relevant players could be central banks, governments, and institutional investors (hello UK pension funds…). Or as Sebastian Mallaby wrote in More Money Than God:

“This book has described the many ways hedge funds make money: by trading against central banks that aren’t in the markets for a profit; by buying from price-insensitive forced sellers; by taking the other side when big institutions need liquidity; by sensing all kinds of asymmetrical opportunities.”

Michael Mauboussin laid out a helpful framework for thinking through edge which I want to revisit and start to augment with examples. I hope it’s going to be more elaborate and useful than Jeremy Irons’s legendary rule of thumb:

“What have I told you since the first day you stepped into my office? There are three ways to make a living in this business: be first, be smarter, or cheat.”

Or in Buffett’s words: “We want a mathematical edge in every transaction.”

Taking the BAIT

“Who is on the other side,” Mauboussin’s paper on investment edge, should be required reading for any investor. “The key to winning,” he writes, “is participating in a game ... [as] the most skilled player.” However, markets are “generally highly competitive” and low-skill games only remain so if there are barriers for sophisticated players such as size constraints (the best investors quickly exit the micro-cap space by virtue of their success). Mauboussin called his framework BAIT:

“If you buy or sell a security and expect an excess return, you should have a good answer to the question “Who is on the other side?” In effect, you are specifying the source of your advantage, or edge. We categorize inefficiencies in four areas: behavioral, analytical, informational, and technical (BAIT).”

Informational: “Information inefficiency arises when some market participants have different information than others and can trade profitably on that asymmetry.”

Analytical: “Analytical inefficiency arises when all participants have the same, or very similar, information and one investor can analyze it better than the others can.”

Technical: “Technical inefficiency arises when some market participants have to buy or sell securities for reasons that are unrelated to fundamental value.”

Behavioral: People make mistakes, individually and as part of groups.

“Behavioral inefficiencies may be at once the most persistent source of opportunity and the most difficult to capture. Many behavioral inefficiencies emanate from the psychology of belief formation and the psychology of decision making. It is essential to remember that these inefficiencies are generally the result of collective, not individual, actions.”

It’s interesting to consider how these sources of inefficiency changed over time:

Keep reading with a 7-day free trial

Subscribe to Frederik's Age of Alchemy to keep reading this post and get 7 days of free access to the full post archives.