Was Tepper Wrong? Liquidity, Timing, and the Keynesian Beauty Contest

Minds and Markets #2, 2023

Hello everyone,

During my conversation with Paul Podolsky, he compared great portfolio managers to artists. Both seem to be able to see around corners, imagine a different world, and act before the rest of us.

They're imagining what that future is. Some of those things are radically different than what we're living through right now. And those are the people that correctly call stock market bubble tops and crises and things. There is an element to it that I think is quite artistic.

If you think about artists that create stuff that seems really out there initially, but then 10, 20, 30, 40 years later, people are like, this is the most beautiful thing ever done. They're doing the exact same thing. They're imagining a set of pictures in our head that are gonna resonate.

This reminded me of a quote by Bruce Kovner when asked by Jack Schwager about what made him different: “I have the ability to imagine configurations of the world different from today and really believe it can happen. I can imagine that soybean prices can double or that the dollar can fall to 100 yen.”

This presents an obvious challenge. Not only do you have to be right, you have to survive until reality and the market catch up with your view. Otherwise you won’t get paid. Just ask van Gogh. Or Michael Burry, almost. And in the interim, the market can throw all kinds of antics (short seller John Hempton: “We found the Wirecard fraud in 2009. It went from 9 to 191 euro and then to zero. It was our biggest ever loser.”).

It’s particularly challenging when making a call on the entire market. During this episode of Investing by the Books, Gregory Zuckerman called David Tepper the best hedge fund trader he knows. Tepper, according to Zuckerman, is always a step ahead. Well, in December last year, Tepper came out of hibernation to comment on the market. He was ‘leaning short’:

We don’t have coordinated tightening around the world, everybody tightening at the same time, too often. We just don’t. And I don’t have people tell me they’re gonna further tighten, they don’t tell me where they’re gonna go too often.

… I’m leaning short on the equity markets. I think the upside/downside [risk here] just doesn’t make sense to me when I have so many central banks telling me what they are going to do.” (Also: Barron’s, Billionaire David Tepper Is Betting Against the Stock Market Because of the Federal Reserve)

Tepper advised caution and followed a longstanding trading maxim: “don’t fight the Fed.” Or in the words of Stanley Druckenmiller:

Earnings don’t move the overall market; it’s the Federal Reserve Board. It’s liquidity that moves markets.

I just finished the autobiography of Roy Neuberger, founder of asset manager Neuberger Berman, who commented on one of his mentors:

He was the first person to get me interested in the Federal Reserve system. He said that the most important factor motivating the market is the supply of money available for investment and speculation. Looking back at that remark from many decades in the business, I would say, clearly, that he was right on target.

It sounds intuitively right. But I’ve never found it to be quite that simple.

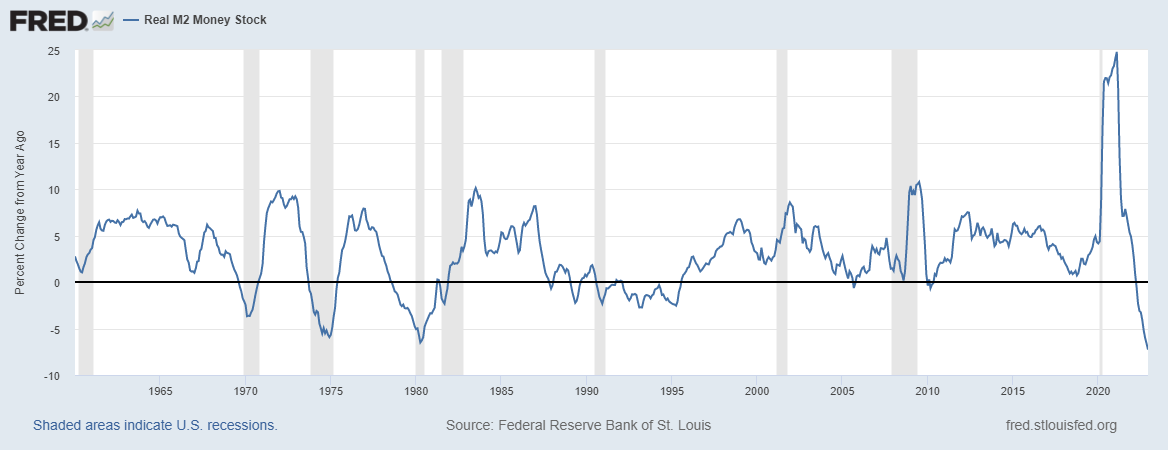

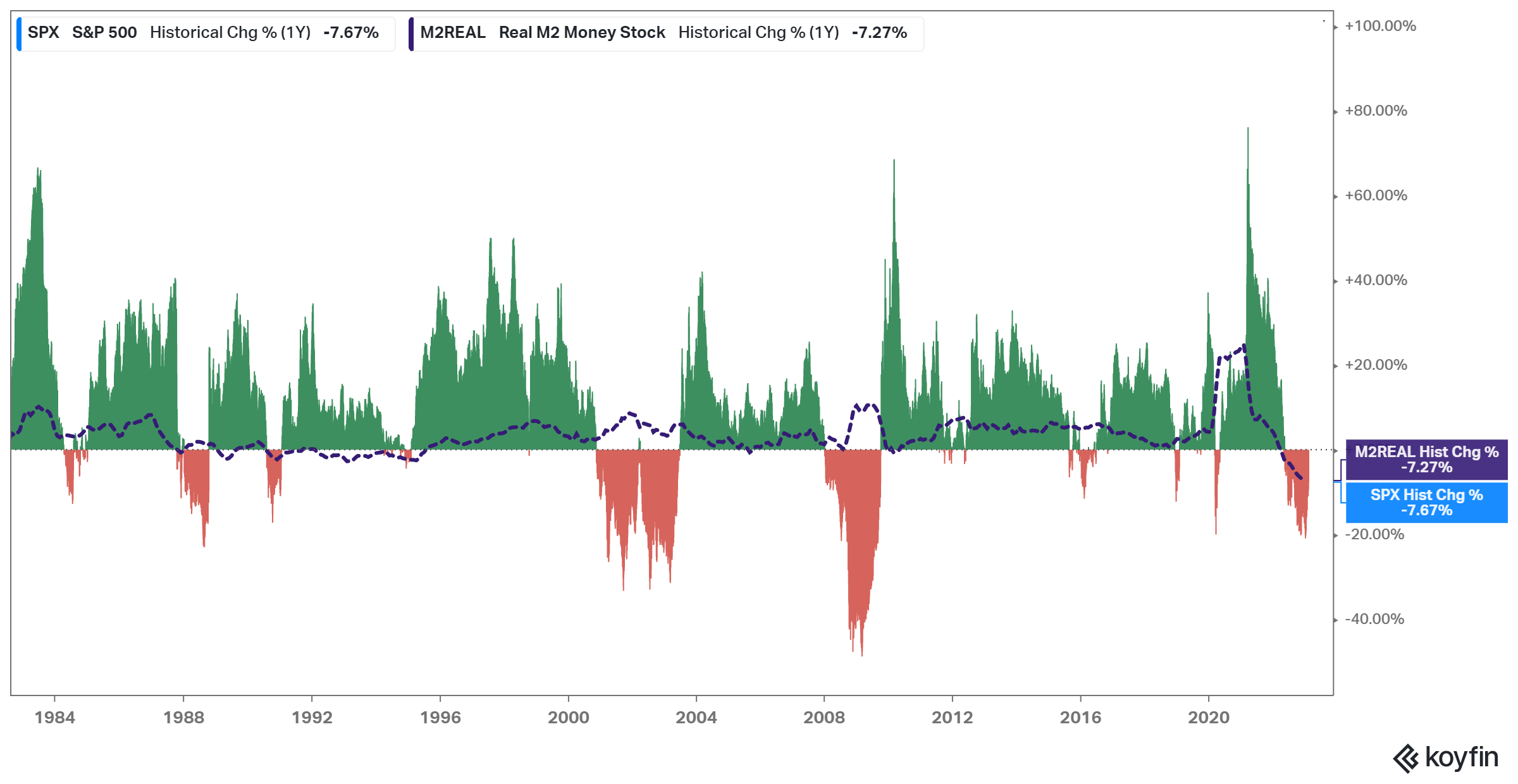

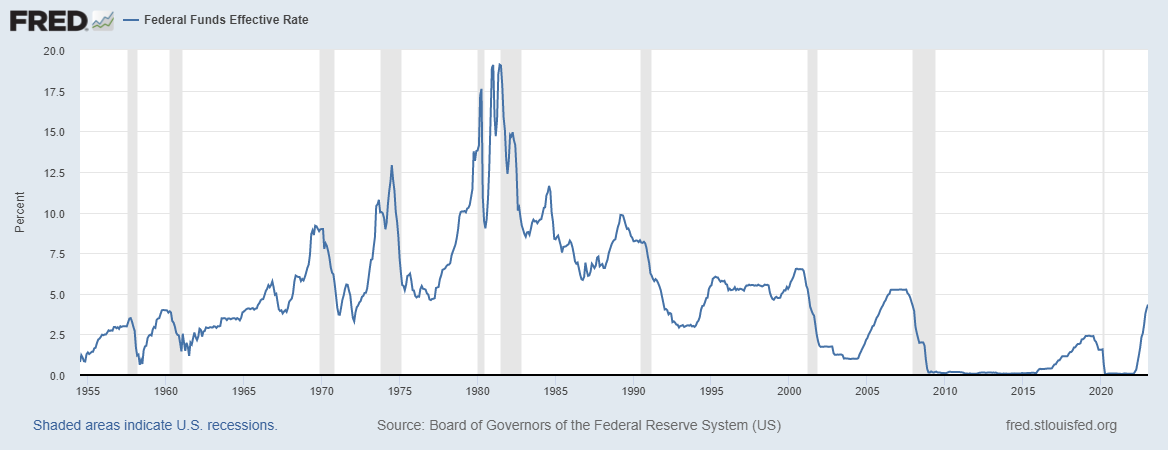

First, people use the term ‘liquidity’ to describe a variety of things in this context. People look at bank reserves, the change in M2 money supply, the Fed’s balance sheet, global central bank assets, some other combination (like currency + reserves + Treasury paper held by the public), or a combination of monetary measures and financial/credit conditions. If you’re a strategist at an investment bank, you best come up with your own liquidity indicator.

It’s kind of a mess of different indicators and often conflates money supply and credit conditions (like spreads on high yield, for example) under the broader term of ‘liquidity’.

Look at M2. Perhaps this was helpful in the 70s and early 80s when a severe contraction warned investors of a downturn. But since then?

Sure, you can use it in retrospect to help construct a narrative. But it’s not a reliable indicator of market returns. No single indicator could be that over the long run.

Not only is the market always shifting and reconfiguring itself, it’s also a complex adaptive system. Which means its damn participants are aware of their own history. Indicators are a great example of the Keynesian beauty contest in which observers move from observing the object to observing each other.

"It is not a case of choosing those [faces] that, to the best of one's judgment, are really the prettiest, nor even those that average opinion genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth and higher degrees." (Keynes, General Theory of Employment, Interest and Money, 1936).

If someone made a killing trading a leading indicator, like declining money supply, the market eventually catches on. The indicator becomes less important than the game of expectations. What does the crowd think the indicator will be? What does the individual in the crowd think the rest of the crowd is thinking? No wonder traders like Platt care a lot about figuring out consensus and positioning.

And even Platt, who recognized the coming financial crisis by looking at declining liquidity in the interbank market, is not clairvoyant. The indicators that had served him well in 2008 led him to bet on a crisis in 2011 that did not transpire. The rules of the game had already changed.

That doesn’t mean indicators of money supply and credit conditions are useless. But in the short-term, the market is as much about the data as it is about positioning and expectations. And things shift very quickly. You thought central bank assets were declining and this was a headwind to markets? Well, suddenly the Bank of Japan steps back in and assets are actually spiking. Sure, the Fed is still hiking. But with inflation falling, they’re shifting the outlook for further hikes. And financial conditions have actually been easing already.

The challenge with listening to someone like Tepper is that you don’t know which timeframe they are operating on. Tepper has transcended styles and labels. He can take a long-term view in making a distressed investment and take a short-term view in his portfolio.

The piece to read about this is Graham Duncan’s excellent essay The Playing Field (my notes) in which Graham describes Tepper as follows:

Tepper appears to be using multiple mental models when he invests, choosing what works for a moment or context rather than being constrained by his historical role as a “distressed debt investor.” If you monitor the 13F filings of the stocks he owns, he appears to move effortlessly across sectors and asset classes, scooping up dollars as he goes. You would have a difficult time deciding what benchmark or comparable fund to judge him against.

To a short-term trader, his December comments seem wrong. They were made at a time when risk assets were bottoming and liquidity was starting to improve. Since then, the Fed has not stopped hiking but declining inflation has allowed a less hawkish stance. And markets have bounced.

But to the investor, his comments may still ring true. What’s a month in the context of a credit cycle after all? Here’s Jeremy Grantham on the yield curve:

But the most ancient and effective predictor of future recession, the 10-year minus 3-month yield spread, is now clearly signaling recession within the next year. This spread has gone negative only 8 times in the past 50 years and all 8 times have been followed by recessions.

While that’s true, the curve inverted in late 2019 and the following recession was arguably caused by the impact of COVID. Anyway. You can also look at leading economic indicators (and try to square those with continued strong employment growth). Then remember that Grantham nearly lost his business during the dotcom bubble because he was bearish early.

If you have a long-term view, you have to be both mentally and structurally prepared to be patient and sit through periods of looking wrong (great fund managers need to resist peer pressure).

And while no indicator is infallible, have we ever had a hiking cycle without a recession and distressed cycle?

Actually yes, once. Conor at

did a great post on this. 1994 was such a soft landing. However, that didn’t come after a massive boom in credit (the 1980s boom had already faltered). This time there has been a lot of credit built up and we might be in for the first non-industry specific default cycle in a while. But can that happen without a recession while stocks are climbing back to all-time highs? That seems like it would be first.

Paul described the minds of great portfolio managers as working “like a kaleidoscope. They're staring at the world and keep shifting the kaleidoscope and it's literally changing every single day.”

If that doesn’t sound like you, it’s best to stick with Neuberger’s advice:

My advice is to learn from the great investors-not follow them. You can benefit from their mistakes and successes, and you can adapt what fits your temperament and circumstances. Your resources and your needs are bound to be different from anyone you may want to emulate.

Most of us don’t reorganize our view of the market on a daily basis. We have to be careful listening to exceptional operators like Tepper who transcend the investor/trader categories and who can pivot back and forth between different time frames. It’s too easy to get sidetracked by comments from people playing a different game or to waste a lot of time going down the rabbit hole on indicators that are being gamed by market participants already.

When in doubt, stick with Tepper’s comment from 2021:

‘Sometimes there’s times to make money … sometimes there’s times not to lose money’.

Stay safe out there and thank you for reading,

Frederik

Some terrific reads this week.

Framework for evaluating character.

Ted Gioia’s ‘8 Best Techniques for Evaluating Character’. Much of this boils down to ‘look at what they do, not what they say’ and creative ways of finding a track record of choices. However, perhaps the most powerful way to use this framework is as a mirror. How do we measure up?

1. Forget what they say—instead look at who they marry.

2. See how they treat service workers

3. Discover what experiences formed their character in early life

4. How do they invest their two most valuable resources?

5. Identify what irritates people the most in others—because this is probably the trait they dislike most in themselves.

6. Can they listen?

7. If they cheat at small things, they will cheat at big things.

8. Watch how they handle unexpected problems

Primer on short sellers.

Terrific piece by Marc Rubinstein on the history and evolution of short selling with prominent examples.

Buffett highlights another kind of short seller, the specialist short-selling fund. “I would never put any money with a short fund, but not because I would think it would be ethically wrong. I just think they’re unlikely to make money.”

Even with an activist bias, it is still difficult for short-sellers to make money. “I could have made a lot more money with a lot less trauma if years ago said we’re going to do a long oriented fund,” says Carson Block, founder of short-selling firm Muddy Waters Research. But the people who do it have other incentives. “We probably have a belief…that we’re smarter than a lot of the people around us, even the people who are more successful and more popular than we are, and we probably ha[ve] a burning desire to show them up!”

Over the years, short-sellers have put the spotlight on Enron, Lehman Brothers and plenty more bad companies. In so doing, they improve price discovery for all market participants while helping to combat fraud. As interest rates rise, the return on cash that short-sellers receive when they sell stocks goes up, making short-selling structurally more profitable. That, and the success of firms like Hindenburg, will likely draw more capital in. Everybody is better off for it.

Seth Klarman’s lessons.

The Forgotten Lessons of 2008: Seth Klarman. Conor dug out a gem on enduring lessons that investors quickly forget. Also check out his piece A Hike Across History for a breakdown of previous hiking cycles.

Klarman has a history of commenting after cycles. In 1990, he wrote an op-ed in the Washington Post about the lessons from the 80s junk bond and takeover binge (download link). Nothing much changed and the high yield market returned with a vengeance as soon as the economy improved.

on Henry Singleton.

Singleton’s story is outlined in The Outsiders. His discipline makes for a compelling contrast to Charlie Bluhdorn, whose ego got the better of him during the conglomerate boom. The Kingswell write-up highlights the major lessons on capital allocation.

Collection of investment tools.

Ed Dorsey shared a collection of terrific links: The Best Stock Research Tools for 2023.

Keep reminders of your mistakes.

Conversation with value investor Chris Davis. Interesting idea to use physical stock certificates as a tangible reminder of your mistakes.

When Chris began as a manager with Davis Advisors, he became obsessed with the idea that you have to study mistakes in order to get better. The best way to do that is through prompting a conversation through displaying the actual stock certificates. This meant framing the stock certificates of their mistakes, hanging them on the wall, and including a plaque that codifies a transferable lesson from that mistake. That wall currently holds about 25 certificates; lessons learned.

Brilliant piece, Frederik. Love the comparison of artists and elite investors