Thinking About the Tail End and the Long-Term. With Mark Leonard, Nick Sleep, Druckenmiller, Buffett and Reinsurance, Paul Tudor Jones, Alix Pasquet

Minds & Markets #1, 2023

Hello everyone,

A few days ago, I returned from Portugal following a brief detour to Germany to see my ailing grandparents. My time with them always leaves me revisiting my values and priorities.

I often struggle being fully present during vacations. My mind gets pulled to work, to Twitter, to books. After a few days, I yearn to sit by myself, read, write, and jump back on the never-ending information hamster wheel. Sometimes that’s a positive as the friction of travel can be surprisingly creative. Airports, trains, and planes are perfect places to practice meditation, write, or churn through books and podcasts. It’s a joy to turn outer constraints into an inner happy zone.

But it’s treacherous to carry this impulse into the precious moments we have with our loved ones. The world of ideas and information always feels interesting and important. It offers the steady dopamine drip of scrolling and discovery. And because it comes in bite-sized engagement, it doesn’t feel costly. What’s the downside of being distracted by the phone for a few moments?

In The Tail End, Tim Urban brilliantly visualized how little time many of us have left with our family. And how uncomfortable it can be to face this.

Take my grandparents. There are only a few topics still interesting to them. Everything boils down to health, family, and happiness. Work is only interesting to the extent that it offers a sense of meaning, happiness, satisfaction, and enough money for a comfortable life. To people who lived through war and hunger, a middle class life already represents abundance. Greater aspirations pale in comparison to the not-so subtly expressed longing for a healthy and expanding family. Setbacks and mistakes seem less important, too. As the time window shrinks, there is no doubt what matters to them: people, not things.

They intuitively know what I need to re-learn by reading Urban’s post:

2) Priorities matter. Your remaining face time with any person depends largely on where that person falls on your list of life priorities. Make sure this list is set by you—not by unconscious inertia.

3) Quality time matters. If you’re in your last 10% of time with someone you love, keep that fact in the front of your mind when you’re with them and treat that time as what it actually is: precious.

I try to keep all this in mind as I draft lengthy lists of goals. There’s nothing wrong with ambition and material aspirations. But every day we face a decision of how we spend our marginal time, the brief moments not committed. Do we invest that time in trying to get ahead? Do we waste them on some app? Do we use them for ourselves or do we share them with someone important to us?

Long-term thinking means that we turn ourselves into advocates of our future selves who see the tail end, and everything that truly matters, clearly.

I hope you’ve all had an amazing start into the near year.

Here are a few of my favorite reads from the past few weeks. If there’s a unifying theme, it’s the need to think long-term. And the occasional tension this creates with the need to be nimble, flexible, and find short-term feedback.

Maintaining habits: “If you maintain the habit, then all you need is time.”

Reinsurance and Berkshire. “A bad reinsurance contract is like hell: easy to enter and impossible to exit.”

How to spot an inexperienced dealmaker

Field research with Alix Pasquet and Druckenmiller; the need to think long-term with Sleep and Zakaria and the upside of being a trader with Paul Tudor Jones

Lessons from Mark Leonard’s life (and what he’d do differently)

Maintaining habits

One challenge of travel is that it takes us out of our habits. Whether it’s exercise, reading, creative work, diet, or practices like meditation. I can return to find my apartment as it was, yet my daily routines I often have to rebuild with conscious effort.

I enjoyed this conversation between James Clear and Tim Ferriss in which Clear made a point about scope vs. schedule.

I give myself permission to reduce the scope but stick to the schedule. There have been days where all I have time for is to do a couple sets of squats, but it counts for a lot to not throw a zero up for another day.

Bad days matter more than the good days because if you show up on the bad days, even if it’s less than what you had hoped for, you maintain the habit. If you maintain the habit, then all you need is time.

I found this simple yet profound. If you maintain the habit, all you need is time.

This applies to a lot of areas that compound. Whether it’s learning, investing, building, creating, relationships. If you manage to not interrupt the positive forces in your life, all you need is time to compound.

Speaking of time and compounding, Buffett’s health and longevity in face of his seemingly awful diet seem at least as impressive (but not replicable) as his returns. Tweet of the week goes to Brandon:

More perplexing even is Buffett’s pride in a behavior that compounds negatively long-term:

AUDIENCE MEMBER: Good morning. I’m (inaudible) from Walnut Creek, California. Could you please expand on how do you maintain your good mental and physical health? (Laughter)

WARREN BUFFETT: Well, you start with a balanced diet. (Laughter) Some Wrigley’s, some Mars, some See’s, some Coke.

I suspect we don’t know the whole truth and that underneath Buffett’s house is a secret lair stuffed with broccoli, a yoga studio, medical staff… Or perhaps it’s just that he created the right conditions and removed sources of chronic stress.

You know, I have no stress whatsoever. Zero. You know, I mean, I get to do what I love to do every day. You know, and I’m surrounded by people that are terrific.

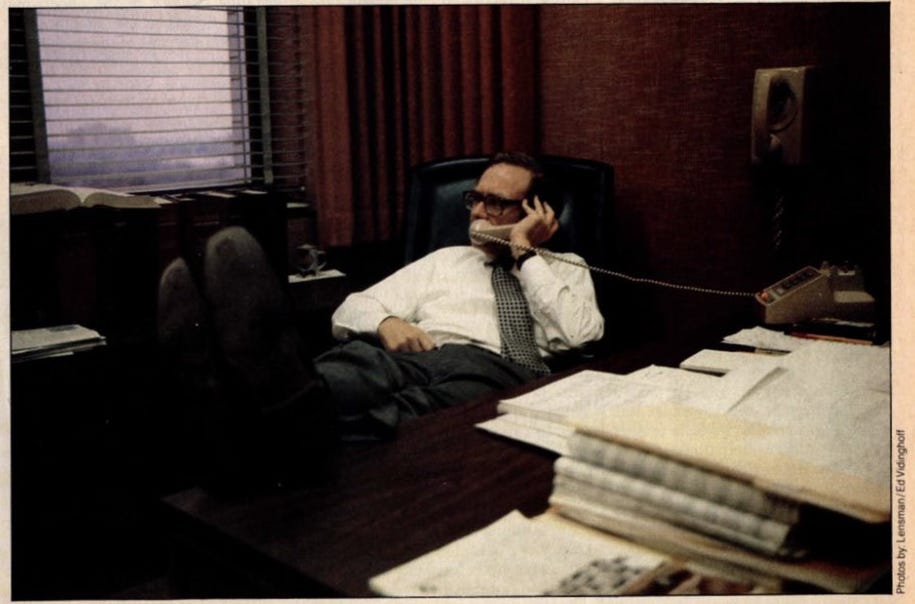

That’s why I liked the 1979 profile. Does this man look stressed?

Marc Rubinstein on reinsurance and Berkshire

Terrific piece on the net interest with background on the reinsurance industry and Berkshire’s involvement. Again, an area in which long-term thinking and incentives are crucial. Head over to learn from Marc about Buffett’s principles in this arena.

But Buffett wasn’t always good at reinsurance. He launched his first reinsurance operation in 1969. … However, the market soon turned and George Young didn’t manage it well. “Net, counting the value of float, it was not a good business for us for 15 years,” said Buffett in 2011. “It’s not an easy business. It looks easy most of the time.”

Buffett suffered from the poor business he wrote in the 1970s for many years. “After more than 20 years, [we] regularly receive significant bills stemming from the mistakes of that era,” he wrote in his 1995 shareholder letter. “A bad reinsurance contract is like hell: easy to enter and impossible to exit.”

Buffett explains in his 1997 shareholder letter (emphasis added throughout): “Consider, for example, the odds of throwing a 12 with a pair of dice – 1 out of 36. Now assume that the dice will be thrown once a year; that you…agree to pay $50 million if a 12 appears; and that for “insuring” this risk you take in an annual “premium” of $1 million. That would mean you had significantly underpriced the risk. Nevertheless, you could go along for years thinking you were making money – indeed, easy money. There is actually a 75.4% probability that you would go for a decade without paying out a dime. Eventually, however, you would go broke.”

Also: if you know of good pieces dissecting Buffett’s long history across the insurance space, please share them with me.

Spotting an inexperienced dealmaker

How do you spot an inexperienced dealmaker? Ask former investment banker Adebayo Ogunlesi, founder of Global Infrastructure Partners and profiled in How to Invest. Ogunlesi sought out advice from Henry Kravis who told him that “any fool can buy a business. It’s not when you buy that you celebrate. It’s when you sell at a profit.”

Ogunlesi then pointed out the shift in mindset required from banker to investor:

When we hire new people from investment banking, we can always tell at the very first investment committee, because they are the ones who are emphasizing everything that’s good about the investment. They don’t spend any time on what could go wrong, and they’re always optimistic.

Whereas experienced people say, “Here’s what could go wrong. Here’s all the bad things that you need to know. You make the decision.”

The banker is incentivized to think short-term and close the deal. The investor on the other hand has to live with the consequences. Of course, the best bankers (or any kind of broker or agent) realize that their most valuable assets are trusted relationships — which require long-term thinking.

Field research with Alix Pasquet and Druckenmiller; the need to think long-term with Sleep and Zakaria and the upside of being a trader with Paul Tudor Jones

I fondly remember watching this talk by my friend Alix Pasquet at Columbia University. He’s finally sharing notes on Twitter including this anecdote on Stanley Druckenmiller:

“I had a guy who managed some money for me come in when the stock was $82 (Tesla). And I think I was 62. I had given myself a Tesla for my sixtieth birthday. And he had this incredibly effective analysis, like 20 pages of financials about why Tesla was a short. And at the end of this presentation – really well thought out – I said, ‘Have you ever driven the car?’

And he said, ‘no.’

And I sent him his redemption notice the next week.”

Spending time with the product is just a piece of the mosaic, though possibly an important one in consumer goods (particularly for products that create strong positive or negative reactions among the professional investor demographic).

Druckenmiller thinks in a sequence of short and intermediate term steps. He has a long-term thesis but can change his view on a dime. Very different from Ron Baron, profiled in in How to Invest, who used Tesla as an example for the need to be patient as a fundamental investor:

It’s not the time. It’s the fundamentals of the business. I could own a stock for a number of years and not make a return on it, and that wouldn’t bother me as far as making me think I had made a mistake. We were an investor in Tesla for four or five or six years and didn’t make a return. Then, all of a sudden, we made twenty times our investment in a year. So it’s not the time that does it. It’s the fundamentals.

Similarly, in their December letter Nick Sleep and Qais Zakaria urge us to think long-term: Thinking about how to think: Short-term vs long-term.

It seems to Zak and me that for most companies to thrive over the long-term, one constituency must be looked after before all others and, contrary to what some on Wall Street or in Westminster may suggest, that constituency is the customer.

In our opinion, (reasoned) confidence, (deserved/earned) trust and (resultant) patience is what seems to be lacking in so many business, charity and political ecosystems.

Thinking long-term sounds great but is near impossible if your constituency is not aligned. That’s the beauty of Berkshire’s capital structure and the challenge for any mutual fund manager. It’s difficult too for companies trying to hit their earnings number, as Sleep and Zakaria point out:

Companies are not immune: firms that cut (vital) investment spending to “protect (this year’s) profits” or make acquisitions to plug revenue growth holes are borrowing from their future.

There is another tension here: low turnover, long-term investing is a tough learning environment for a young investor. You just don’t swing the bat a lot. While Buffett emphatically recommends holding off until the fat pitch, he did so after a period of actively looking at a lot of situations and having a portfolio that turned over regularly at his own partnership and Graham-Newman.

Paul Tudor Jones also emphasized the benefit of short feedback loops:

The great thing about being a commodity trader is that in a space of 3-4 years, you’d have huge bull markets and huge bear markets. I very quickly learned the psychology, how quickly they could change. I saw fortunes made and lost.

I sat there and watched Bunker Hunt take a $400 million position in silver to $10 billion in 1980, which made him the richest man on earth. Then he went from $10 billion back down to $400 million in five weeks. I learned how quickly it can all go away.

As Henry Kravis said, there’s no substitute for experience in this business. The next best thing is to study history, which brings us to Mark Leonard.

Lessons from Mark Leonard’s life (and what he’d do differently)

Check out this thread by Jay Vasantharajah on a recent talk by Constellation’s Mark Leonard. General advice: be curious, experiment, and look for leverage:

3 forms of leverage: knowledge, people and capital. Mark says knowledge leverage is actually relatively easily to obtain if you focus in a specific area. People leverage is hard, need leadership skills. But you want to eventually have all 3.

Read a lot, especially business history and business biographies. Mark thinks they should teach way more biz history in schools.

Interesting that he didn’t mention technology as a form of leverage despite being in the business of software. Perhaps he considers it part of ‘knowledge.’

Experiment frequently in business. The scientific method is the best method for any business.

Set up a system of iterative improvements in your business. Sooner you can learn and iterate, the better. After each deal, CSU does a post mortem 1 year in. They discuss and share learnings, improve process accordingly.

What stuck out to me was that the one thing he’d do differently related to the core of Constellation’s business model.

Change incentive structure to be focused on organic growth. The current incentive structure caused managers to become acquisitive over everything else. That said, he still mentioned that organic growth is lower IRR on invested capital.

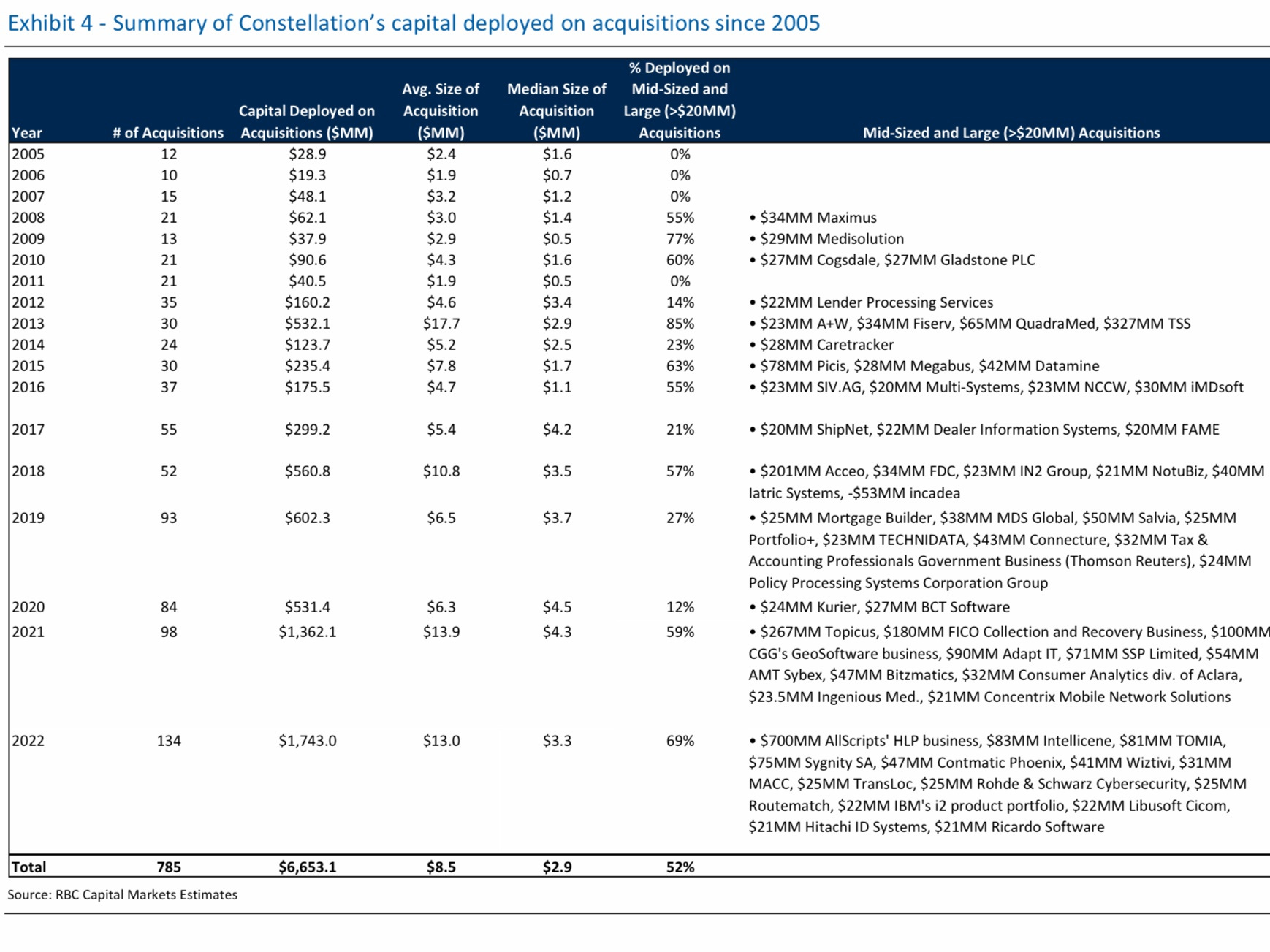

It made sense that Constellation focused on the highest IRR opportunity (underpriced acquisitions) first. Now that there is a lot more competition, the relative attractiveness of acquisitions vs. organic growth has shifted. But now there is a cultural bias for deals embedded in the business? Liberty just shared the incredible number of acquisitions they still do every year:

Like us, Leonard studies the eminent dead and successful contemporaries:

Mark studied a bunch of successful business builders, almost none of them had any real work life balance. If you want to build something great, need to dedicate a large amount of your time to it.

Dunbar number - basically states you can only really have ~50 meaningful relationships max. If most of those are people you work with, doesn’t leave much for people outside of work. Makes work/life balance statistically difficult.

Which brings us to his biggest regret:

Not spending enough time with his family. Was hard to tell this was going to be a regret while in the midst of his career.

Buffett would say that intensity is the price of excellence. This is the recurring and perhaps unsolvable tension behind much success (and something I talked about with David Senra).

Would Leonard have been better off if he had spent more time with his family? Did he need a better internal advocate of his future self? What would have been the implications for Constellation? We simply don’t know. But it’s a question we must answer for ourselves every day.

Thank you for reading.

Frederik

Excellent stitching of wise tidbits! Thanks so much. Food for thought on many things.

The overarching theme of the post on long term horizon. It really is harder than expected, but also even more rewarding than initially thought for many people. Makes me want to start writing about these musings too!!

"Interesting that he didn’t mention technology as a form of leverage despite being in the business of software. Perhaps he considers it part of ‘knowledge.’"

I bet that's what it is.