The Philosopher's Trading Experiment: Peter Thiel and the Big Short That Never Was

The Philosopher's Trading Experiment: Peter Thiel and the Big Short That Never Was

“Our mission is to make sense of the crazy world ... and to understand where there are great opportunities for returns. Not many people are asking the big questions.”

Hello everyone.

I hope everyone had a great week.

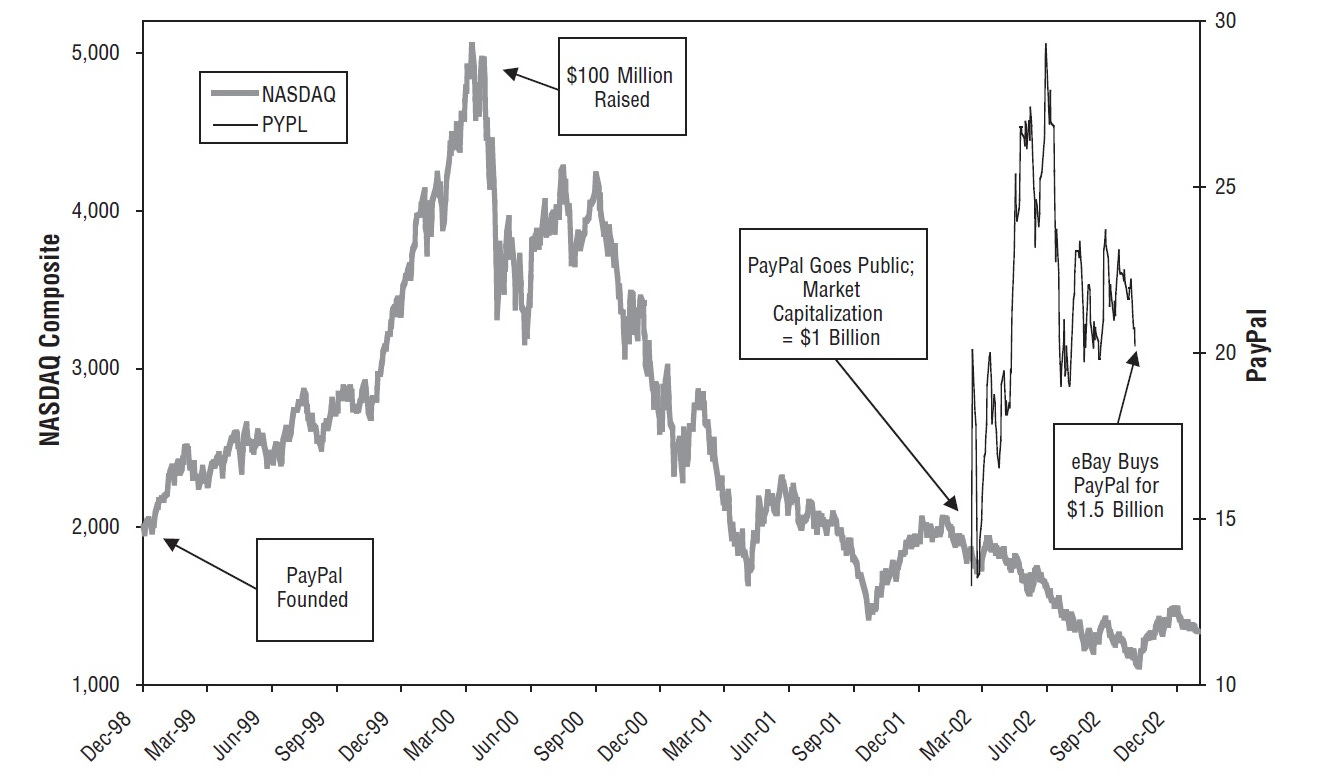

Peter Thiel is known as a venture capitalist, co-founder of Paypal, and for his controversial politics. However, for nearly a decade he was actively trading global macro with his hedge fund Clarium Capital. Thiel had started his foray into hedge funds before investing in and joining Confinity which later became Paypal. After the sale of Paypal to Ebay in 2002, Thiel returned to his passion.

Clarium started strong out of the gate. By 2004, it managed $260 million and was up 125% from inception. By 2006, this had turned into a cumulative return of 230%. By mid-2008, it managed an astonishing $6.4 billion and was reportedly up some 58% on the year.

Earlier that year, Thiel had published a lengthy essay titled The Optimistic Thought Experiment. Investors, Thiel argued, were “eerily complacent.” Their thinking was “rooted in the nineteenth century, when the march of History and Progress were more optimistic and certain.”

Modern markets failed to consider the apocalyptic dimension, scenarios such as nuclear war and the collapse of capitalism. Investors systematically discounted left tail scenarios because if the world came to an end, “all the money in the world would prove of no value. There would be nothing left to buy or sell.”

Major bubbles, he argued, were driven by globalization (a meta theme used for an increase in trade, communication, and transportation; everything from railroads to cars, radios, and the South Sea bubble). This trend would ultimately either usher in a new age or fail. If it prevailed, bubbles such as the dot-com mania could be viewed not as exuberance but as moments of “unprecedented clarity” when investors could see the farthest. If however it failed, the consequences were too dire for investors to consider.

“There are no good investments in a twenty-first century where globalization fails.”

Thiel argued that macro investors failed to consider the “central question”:

“How should the risk of a comprehensive collapse of the world economic and political system factor into one’s decisions?”

Even great investors, he claimed suffered from a “failure of the imagination about the possible trajectories for our world, especially regarding the radically divergent alternatives of total collapse and good globalization.”

Thiel saw a world of “wholesale madness” and a “wildly mispriced macro context.”

“What is truly frightening about the twenty-first century is not merely that there exists a dangerous dimension to our time, but rather the unwillingness of the best and brightest to try and make any sense of this larger dimension.”

Investors need not despair however. For implicit in the essay was that Clarium was willing to wrestle, profitably, with these thorny question. Thiel honed in on the history of market bubbles and busts. And in particular the unfolding housing debacle:

“Consider the strangeness of the American context. One would not have thought it possible for the internet bubble of the late 1990s, the greatest boom in the history of the world, to be replaced within five years by a real estate bubble of even greater magnitude and worse stupidity.”

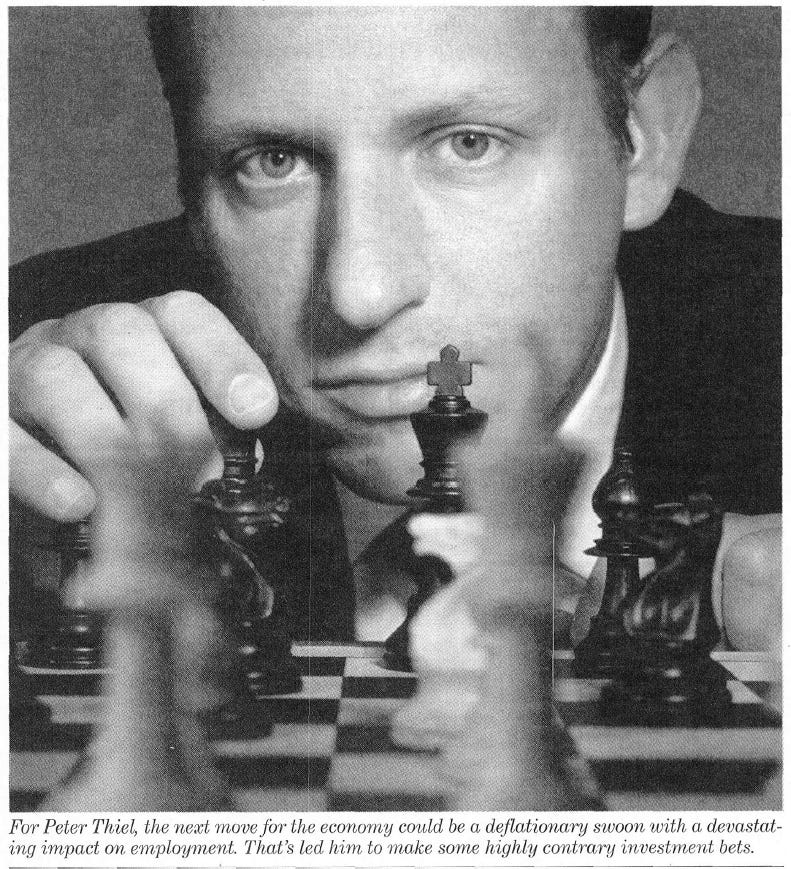

In the years leading up to the financial crisis, Thiel had discussed his macro views. He had anticipated the housing crisis, a deflationary bust, and the bull market in oil. One would have expected 2008 and the following years to be a celebration. But things turned out differently.

Fast forward to 2011, and Clarium’s assets were down 90%, due to investor redemptions and “losses of 65 percent from the mid-2008 peak.” It was a stunning reversal.

According to one LP on Twitter, the remnants of the fund were profitably invested in private stock of Palantir (“I thought that Thiel … wanted to make it up to investors with one of the best things he had access to”).

In The Most Important Thing, Howard Marks writes that “extraordinary performance comes only from correct non-consensus forecasts.”

“You can’t do the same things others do and expect to outperform. … Unconventionality shouldn’t be a goal in itself, but rather a way of thinking.”

Unconventional investment predictions are “hard to make, hard to make correctly and hard to act on.”

Thiel had been contrarian and right. And yet he’d stumbled when it came to execution.

Before we dig into his story, let me make something clear. I am not writing this to point fingers. Rather, the journey of becoming a better investor should include the study of both success and mistakes. If the game of macro investing is difficult for someone like Thiel, what does that mean for the rest of us?

This past summer, Josh Wolfe told me he disagreed with Peter on this.

“He likes to study successes and I like to study failures. I think that failures are more repeatable, you can see errors that are made over and over and again, that end up with the same bad outcome.” A Conversation with Josh Wolfe: Macro, Mentors, Motivation

Clarium is an interesting case study because it highlights the importance of execution, focus, and risk management. One Clarium employee bemoaned they “could have been the big short.” And indeed they could have been. Intellectually, they were on the right track. But having the right idea is just the beginning.

And having differentiated framework for markets and in itself can present a challenge. There is nothing more detrimental to keeping an open mind about the next move than having been proven right on a really big contrarian idea.

Why macro?

Before jumping into the case study, I want to highlight two comments made by Thiel. First, his motivation for choosing global macro. For Thiel, the philosopher turned investor, it was an irresistible intellectual challenge:

“Macro was, and remains, the most promising way to invest. A macro manager can extract value wherever it exists; he isn’t pigeonholed by some narrow brief as in convertible arbitrage or the like, where managers wear style-imposed blinders.

Global macro offers the best investment opportunities and it is probably the most stimulating style out there. Because of that big-picture view, macro is intrinsically very interesting. There isn’t much that’s more engaging than thinking about how the world works.”

Generations of traders agree. As George Goodman wrote in The Money Game about a macro play:

“It is impossible to resist: international intrigue, the mockery of socialism, the chance to profit by the tides of history. “Tell me the game,” I said.”

A second reason was Thiel’s experience during the height of the dotcom bubble. Thiel pushed Paypal to close a big $100 million funding round in March 2000, “at the very peak of the bubble.” He saw anecdotal evidence of the bubble all around him, “inflating on our Palo Alto doorstep.” Raising capital right before capital markets shut down was a formative experience.

“Had we done what everybody else was doing, which was to ignore the forest and just work on our particular tree, we wouldn’t have seen this enormous forest fire coming and we would have been burned along with everybody else. That really drove home the importance of the macro view.”

However, this seems like a treacherous way to start an investing career. Having outsmarted the market once, the investor is primed to look for the next bubble, the next major contrarian play that allows them to re-experience that intellectual high. Thiel already started with an intellectual contrarian bent. I believe his early experience further reinforced this approach and may have ingrained a bearish bias.

Macro vs. startups

A second interesting comment relates to the difference between macro investing and building startups. Thiel was in the unique position of having done both.

How does building a hedge fund compare with building a tech start-up?

“Both involve themes that take time to play out, and both reward managers and investors willing to take the long view. A start-up is about building a business, which is a multiyear proposition. Similarly, we develop themes that may take months or even years to mature. Both require a coherent vision and patience.

In an early stage tech company, the options are limitless: You can work with business, government, or consumers; you can pick your product; you can locate wherever you want. But as time goes on, history starts to dictate the future. The chess metaphor I use is that at the start of a game, you can play any set of moves, but as the game progresses, you become locked into a strategy.

At a macro fund, optionality remains broad. Every day is a new day—you can trade any product, in any country, largely unconstrained by what happened last week, last month, or even last year. That can be daunting, but it’s also what makes the job so interesting.”

While Thiel is right in theory, every day can start with a blank slate in macro, realistically, the investor can become mentally locked in. It’s a key strength of successful global macro players to remain open-minded. To be able to discard ideas. Optionality only remains broad if the mind lets it.

“Life at a fund can be much more emotionally volatile than at a start-up. Fairly large daily swings in the P&L are normal, but they can cause both euphoria and depression in our staff, and managing those emotions is an important part of running the fund.”

These comments, made shortly before the financial crisis, seemed to foreshadow his own experience.

Alright. Let’s get into the lessons:

“Anyone who thinks the market is efficient gets fired.”

A world out of balance.

Deflation and the right historical analogy.

Big ideas: bonds, oil, and stocks

The great real estate bubble.

And then what? “We could have been the big short”

The year 2008.

Ego, experience, and a treacherous metaphor.