Thinking About the Next Warren Buffett

“We get this question a lot from the enterprising young. It’s a very intelligent question: you look at some old guy who is rich and you ask, ‘How can I become like you, except faster?’” Charlie Munger

It’s natural to see someone wildly successful and imagine yourself in their shoes. At least that’s what happened to me when I first read about Warren Buffett as a teenager. Buffett and Charlie Munger are wealthy, wise, and widely admired. They love what they do and spend their days learning, solving interesting puzzles, and painting their canvas at Berkshire Hathaway. They are surrounded by people they like, trust, and enjoy working with. They even have their own cult-like community of students and admirers.

Of course I asked myself, ‘Well, how can I be the next Warren Buffett?’ But like most people, I was too self aware to say it out loud. And over time I forgot about it.

A couple of months ago, I heard someone ask it at the 1997 annual meeting:

“If someone were to form a company doing what you did 30 or 40 years ago, what is your suggestion to them?”

Buffett: “First thing we’d suggest is they send us a royalty.” (Laughter)

Munger: “That’s a question I ordinarily duck. … I always believe in getting the fundamental mental tools in place. … I argue for sound thinking. But the exact specific techniques of turning yourself into another Warren Buffett, I leave to you.”

What a bummer, Charlie. But once the question was back on my mind, it refused to let me go. It felt like a Rubik’s cube each new generation of investors has to solve, worthy of an open-ended exploration. How valuable would it be to know the answer?

Would you like to make 167,000x your money?

How much money would Buffett’s first outside investor have made? I was surprised I couldn’t find this calculation all over the web. The world’s most famous investment track record and nobody has done the math? (Someone on Reddit helpfully pointed out that Lowenstein did a similar calculation in American Capitalist — but as of 1995.) So I put together my own back of the envelope calculation. To be clear: I know this is not the correct number. If you’ve done the math or have seen a detailed calculation, please let me know.

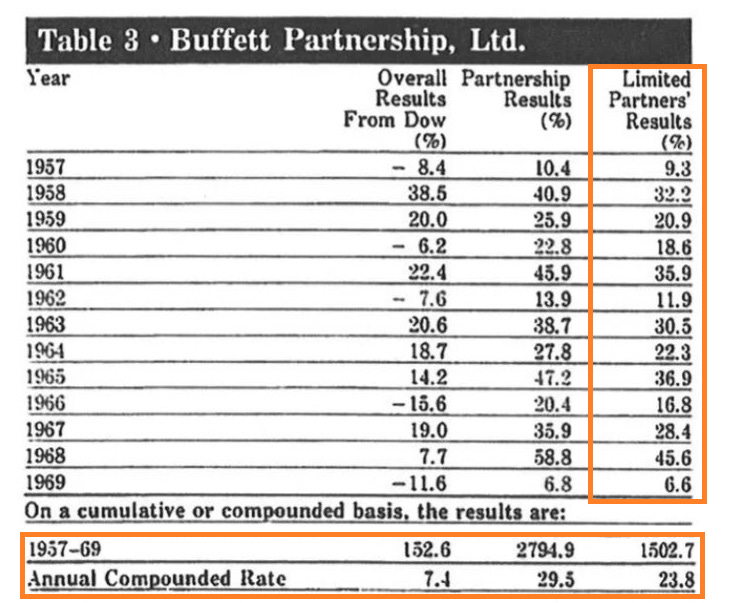

First off, Buffett’s investment partnership absolutely crushed the market from 1957-1969 (really multiple partnerships which he ended up consolidating):

By 1967 however, Buffett felt “out of step with present conditions” (read: the roaring bull market). And by 1969, he decided to shut down the partnership. Per the Snowball, he distributed a combination of cash and securities, including stock in Berkshire Hathaway and Diversified Retailing (which was later merged into Berkshire). For simplicity’s sake, I assumed that an investor in the partnership swapped their entire stake for Berkshire stock at the end of 1969.