The Evolution of Endowment Investing

David Swensen, John Keynes, Warren Buffett, and Larry Tisch.

When I worked as an allocator, endowment investors were seen as the smartest money. Their investment philosophy and emphasis on alternative investments, called the endowment model and pioneered by Yale’s David Swensen, had shaped the allocator landscape. New managers could not do better than get an investment from Yale’s endowment, a stamp of approval that would open countless doors.

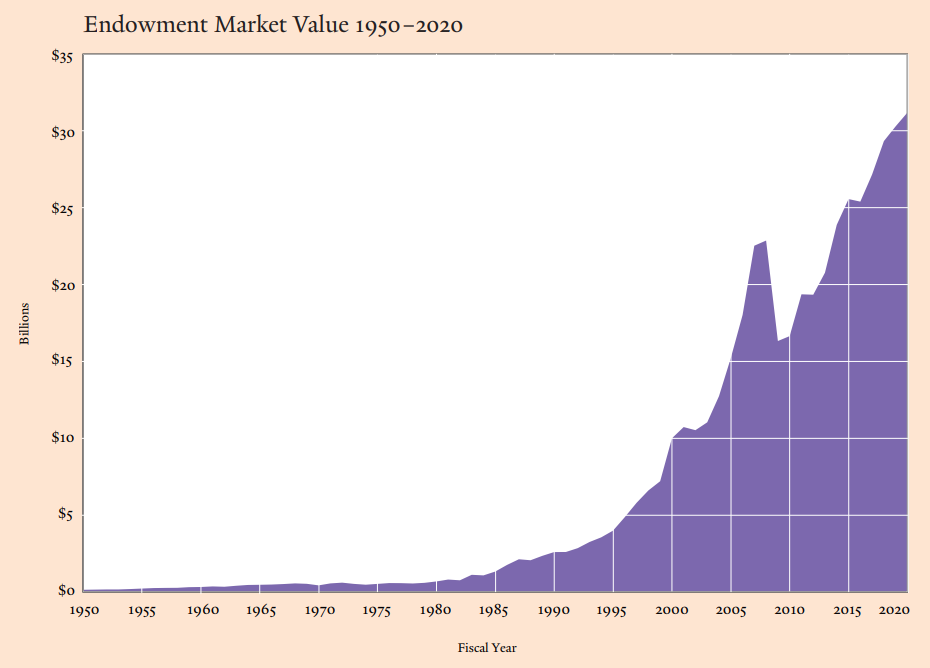

“Mr. Swensen grew Yale’s endowment from $1 billion when he started in 1985 to $31.2 billion in 2020 through an embrace of a diversified investment portfolio.

When he left a Wall Street job at Salomon Brothers (and took an 80% pay cut) to join Yale in 1985, the Ivy League school’s endowment was invested in the same sorts of assets that all college investment managers chose in those days, plain vanilla stocks and bonds. Swensen forged a new path.” David Swensen Dies at 67

Yale’s endowment under Swensen’s tenure from 1985-2020.

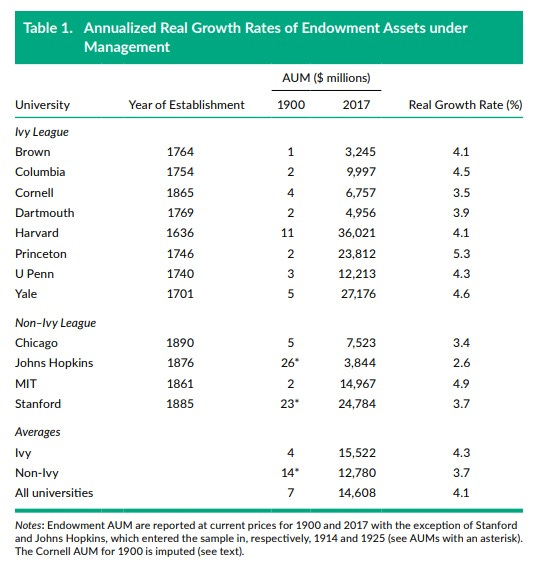

I’ve written before about the struggles of emerging managers and the importance of understanding how allocators work and I believe any serious investor should study Swensen’s ideas and legacy. Alumni of his office now manage other institutions like Princeton, MIT, UPenn, Stanford and others (Yale Endowment Chief Leaves Legacy Of Top College Investment Leaders).

But endowments were not always the smart money. Quite the contrary. Swensen recounted in Pioneering Portfolio Management how nearly all of Yale’s initial endowment was lost in a concentrated bet on a local bank. While they are run by professional staff today, I was surprised to discover that several investment legends shaped endowments over time (Keynes, Buffett, Tisch — even Stanley Druckenmiller was involved at his alma mater though I couldn’t find a good account of his contribution).

Live chat next week Tuesday!

I will be joining Ted Seides and Jamie Catherwood this coming Tuesday, October 11th, to talk about institutional investing and its history. I expect a wide-ranging, interesting, and fun discussion. If you’re interested, you can register to join us here.

Endowment eras

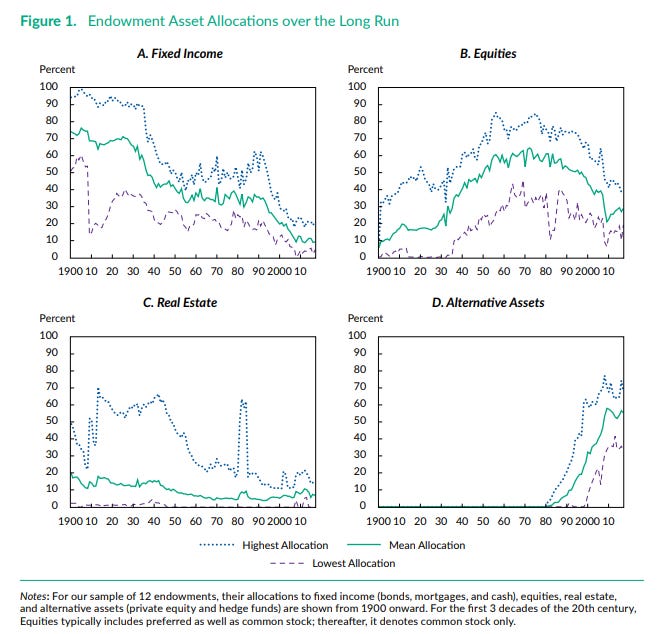

“We document here two major shifts in endowment allocations to risky assets—the first from bonds to stocks and the second from stocks to alternative assets beginning in the 1980s. In both eras, the Ivy League schools led the way in these asset allocation moves. We explore the rationales behind these major shifts in investment strategy” Seventy-Five Years of Investing for Future Generations

We can find three distinct eras of endowment investing in the chart below:

The conservative origins: primarily a bond portfolio, roughly until the 1930s-40s.

A shift to equities with a peak allocation around the 1970s and Nifty Fifty era.

The golden age of alternatives and the endowment model.

An open question is whether we are entering a fourth, post-endowment model, era.

Shift to equities: Keynes and King’s College

John Maynard Keynes managed the endowment of King’s College, Cambridge from 1921 until his death in 1946. He made a significant shift in asset allocation, though in his case he was primarily divesting out of real estate.

“His appreciation of the attraction of equities to long-horizon investors proved to be his great investment innovation. … King’s College endowment ignored equities in favour of real estate and fixed-income securities up to 1920. As soon as Keynes took over the management of the endowment he set about selling off a substantial portion of the real estate portfolio in order to reallocate these funds to equities.”

Keynes evolved from trying to actively time the market to “a more careful buy-and-hold stock-picking approach in the early 1930s.” Like any investor of his day, he was shaped by the experience of the 1929 crash.

“[Earlier] I believed that profits could be made by… holding shares in slumps and disposing of them in booms. [But] there have been two occasions when the whole body of our holding of such investments has depreciated by 20 to 25 per cent within a few months and we have not been able to escape the movement…

As a result of these experiences I am clear that the idea of wholesale shifts is for various reasons impractical and indeed undesirable. Most of those who attempt it sell too late and buy too late, and do both too often, incurring heavy expenses and developing too unsettled and speculative a state of mind.” Keynes, King's and Endowment Asset Management

Swensen quoted Keynes repeatedly and shared his views on a preference for equity exposure, long-term focus, disapproval of market timing, and value bias. While Keynes had to arrive at these conclusions through personal experience and observation in markets, Swensen could use academic research and more extensive historic data.

“As a result of his experiences and his advocacy for equities as the preferred asset class for long-term investors, the great economist had a considerable influence on the US endowment model.” Seventy-Five Years of Investing for Future Generations

Endowments go pro

It seems that Harvard was one of the first (or the first?) of the Ivy colleges to professionalize its endowment office. It was not a full-time job and they picked the head of one of the earliest investment funds, State Street.

“In 1948, Harvard University had made the decision to appoint Paul Cabot as university treasurer with responsibility for managing the university’s endowment. Cabot undertook this job successfully while continuing as chief executive of his investment firm, State Street. This appointment represented the first time an outside investment professional had been assigned to run Harvard’s endowment.”

Cabot was profiled in John Train’s Money Masters but I couldn’t make out much about his philosophy other than a focus on fundamental analysis and sober stock picking.

“As early as February 1928 we felt it wasn't safe to assume that the past four years of good returns would continue. Therefore, we did some selling ahead of time and then turned into buyers when stocks became cheap (in the 1930s),” says Cabot, who rarely advocates market-timing except when valuation levels are absurd.” Financial Services Week, 1993

Outrageous: Buffett at Grinnell

While endowments were getting more professional, there are examples of very creative investing. The Snowball outlines how Buffett served as a trustee at Grinnell College where he worked with Joe Rosenfield, a local department store owner. Rosenfield was rebuilding Grinnell’s endowment after the college “had nearly gone broke.” Buffett and Rosenfield talked regularly and sourced a variety of profitable deals:

“The more outrageous the act might seem for a college endowment, the better Joe and I liked it. Every investment move was always entertaining for us and always (well, almost always) profitable. In fact, we truly had more fun making money for the college than we did in making investments for ourselves.

We conspired to have the college buy convertible debentures in a startup (Intel); shorted securities in a ‘can’t-lose’ arbitrage (AT&T); made a leveraged buyout of a network television station (WDTN in Dayton); and the list goes on.” Buffett recounts in the forward to “Mentor: Life and Legacy of Joe Rosenfield”

Even though Grinnell’s endowment invested in Intel, Buffett passed on it. A technology startup was outside his circle of confidence.

“At Grinnell College, [Buffett] showed up for a meeting to find his fellow trustee Bob Noyce itching to leave Fairchild Semiconductor. Noyce, Gordon Moore, and Andy Grove had decided to start a nameless new company based on a vague plan to extend the technology of circuits to “higher levels of integration.” Joe Rosenfield and the college endowment fund each said they would put in $100,000, joining dozens who were helping to raise $2.5 million.

As much as Buffett admired Noyce, he did not buy Intel for the partnership, thus passing on one of the greatest investing opportunities of his life.” The Snowball

Later, Tom Murphy of Capital Cities introduced Buffett to an opportunity to buy a television station. Buffett’s involvement with the Washington Post prevented him from buying the asset for Berkshire so he took it to Grinnell. Per the Snowball, the endowment bought it “for $13 million, putting down only $2 million. Sandy Gottesman arranged debt financing for the rest. The broker who sold it to Grinnell called it the best deal he had seen in the past twenty years.”

For Grinnell and Cambridge, the involvement of famous investors was a blessing. But at New York University it turned into an expensive lesson.

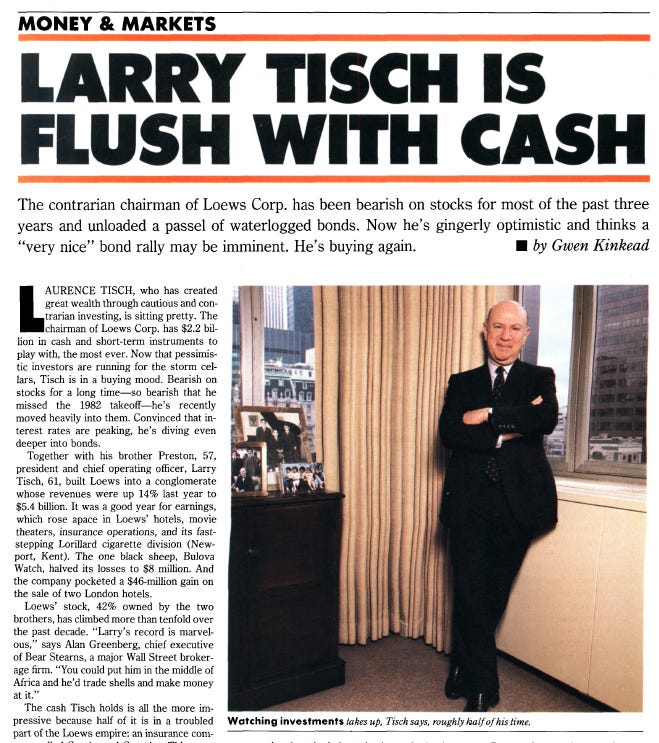

Too cautious: Larry Tisch and NYU

This is an important anecdote in Swensen’s book. Laurence Tisch of Loews was an important donor at NYU and instrumental in the university’s restoration.

“In 1978, when Mr. Tisch became chairman, NYU was recovering from two brushes with insolvency. Its endowment was minuscule, and the university lived primarily off tuition revenue. As a small amount of income was needed for operations, the investment committee … opted for bonds. Bond yields then were high. Given NYU's precarious image, Mr. Tisch & Co. didn't want to risk even a small operating deficit.”

Tisch also served as chairman of NYU’s board of trustees. He was also a conservative investor and skeptical of the new bull market that started in the 1980s. Even with NYU’s finances mended, he stuck to a cautious posture and high allocation to bonds.

“Mr. Tisch, I believe, harbored an irrational and all-weather fear that stocks were "too" expensive. As the market rose and time passed, the subject increasingly dogged the committee, though its discussions were always gentlemanly. More than once he responded, "The train has left the station.” How Larry Tisch and NYU Missed Bull Run, WSJ 1997

This is the issue with getting a famous investor involved. As Peter Lynch put it: “In this business, if you're good, you're right six times out of ten.” But who is going to tell the legend they have it wrong? Swensen wrote about the implications of NYU’s mistake:

“Unfortunately, the bond-dominated portfolio left NYU on the sidelines during one of the greatest bull markets in history. … From 1982 to 1998, an endowment wealth index for colleges and universities increased nearly eightfold, while NYU’s endowment grew 4.6 times.”

He made sure this would never happen at Yale under his watch.

Big ideas: David Swensen’s philosophy

Even if you don’t work as an allocator or follow the endowment model, I’d recommend reading Swensen’s Pioneering Portfolio Management. It’s well-written and Swensen comes across as a very clear thinker. I would focus on the sections around investment philosophy, asset allocation, and different asset classes. The following quotes are from the book, including this crucial one:

“I have come to believe that the most important distinction in the investment world does not separate individuals and institutions; the most important distinction divides those investors with the ability to make high quality active management decisions from those investors without active management expertise. Few institutions and even fewer individuals exhibit the ability and commit the resources to produce risk-adjusted excess returns.”

Swensen’s core ideas are straightforward:

Equity Orientation. Don’t ever fall into the NYU trap. And don’t attempt to time the market. As an endowment with a long-term time horizon, focus on equity exposure.

“Effective equity exposure is the overwhelming determinant of risk and return, with 99% of return variance explained by stock and bond indexes alone in return composites.”

Diversification. It’s the only free lunch there is. However, find a way to diversify with higher returning assets than fixed income.

“Commitment to an equity bias enhances returns, while pursuit of diversification reduces risks. Thoughtful, deliberate focus on asset allocation dominates the agenda of long-term investors.”

“By identifying high-return asset classes that show little correlation with domestic marketable securities, investors achieve diversification without the opportunity costs of investing in fixed income.”

Active Management. Find the best active managers and focus on asset classes that are inefficient and thus reward the skilled manager.

“Absolute return, real estate, leveraged buyouts, and venture capital exhibit dramatically broader dispersions of returns. Selecting top quartile managers in private markets leads to much greater reward than in public markets.”

Private Markets.

“Market participants willing to accept illiquidity achieve a significant edge in seeking high risk-adjusted returns. Because market players routinely overpay for liquidity, serious investors benefit by avoiding overpriced liquid securities and by embracing less liquid alternatives.”

Value Bias. Swensen cut his investing teeth during the golden age of value investing and just in time to watch a major growth bubble unfold (Pioneering Portfolio Management was published in 2000). I don’t know whether this should still be considered part of the endowment model given the challenges of value managers/value factor post ‘08 and the massive shift into venture capital and growth strategies.

The end of history?

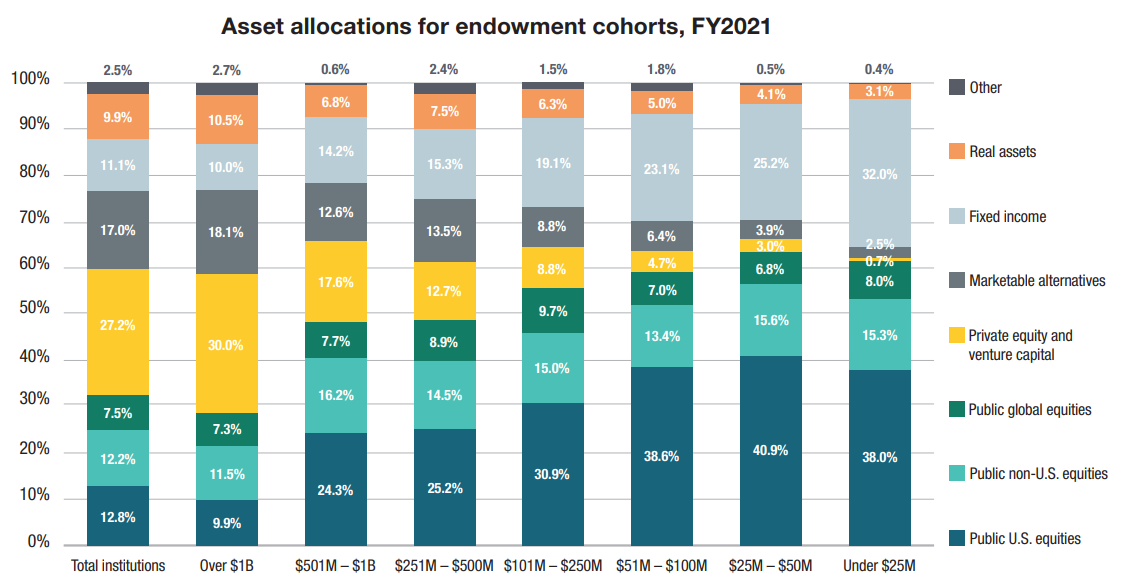

Today, large endowments have adopted Swensen’s ideas. Fixed income is barely a sliver in their portfolios and private markets dominate (see the $1B+ cohort on the right side of the chart):

But Swensen was well aware that private markets were no panacea. His success rested on the right strategy and strong execution. After picking the right asset classes he had to identify and gain access to the best managers.

“While illiquid markets provide a much greater range of mispriced assets, private investors fare little better than their marketable security counterparts as the extraordinary fee burden typical of private equity funds almost guarantees delivery of disappointing risk-adjusted results.

Median results for venture capital and leveraged buyouts dramatically trail those for marketable equities, despite the higher risk and greater illiquidity of private investing. In order to justify including private equity in the portfolio, managers must select top quartile managers. Anything less fails to compensate for the time, effort, and risk entailed in the pursuit of nonmarketable investments.”

By definition, it’s impossible for all allocators to pick top quartile managers. Worse, once allocators flood capacity-constrained strategies like distressed or venture with capital, returns should decrease for all investors. And not only have endowment assets grown significantly, Swensen’s philosophy influenced even larger allocators like pensions. The massive shift into alternative assets affected all investors and created some fortunes along the way thanks to the “extraordinary fee burden”.

Perhaps it’s just no longer feasible to put capital to work the way Rosenfield and Buffett did back in the day. Then again, it seems some managers are implementing similar ideas with concentrated co-investment heavy investing (see a good recent podcast with Scott Wilson).

Swensen wrote about Keynes:

“Keynes writes of the contrarian investor that “…it is in the essence of his behavior that he should be eccentric, unconventional, and rash in the eyes of average opinion.” Managers searching among unloved opportunities face greater chances of success, along with almost certain tirades of criticism.”

What investor, or type of investor, is now (wrongly) viewed as “eccentric, unconventional, and rash” by the mainstream? Whose ideas will shape the next era of institutional investing? Fortunes will be made by those who figure out the answer and offer a compelling solution.

Mike Simanovsky at Conversant Capital has the most innovative strategy I have seen in some time. Public/Private cross-over fund focused on real estate broadly defined. Because real estate is so capital and leverage consumptive, opening up public and private opportunities means there’s always something to do. This solves one of the biggest challenges of institutional investment: through cycle deployment. It’s obviously niche but I think as volatility increases, investors that can always be effectively deploying capital will be increasingly in demand.

Such different ways to deal with investing. Thank you for showing quite a few different approaches in this article and able to find my way in to investing. Loved the article and the way you have dealt with different aspects at the right time while reading.