The Crash of 1987: Julian Robertson’s Test of Conviction

“Probably none of us have ever lost so much money so fast in our lives.”

If investing is an exercise in decision-making under uncertainty, as well as navigating one’s biases and emotions, then I believe firsthand accounts are at least as valuable as abstract knowledge of market history. We all know the market recovered from the 1987 crash. We all know the economy eventually escaped the grips of the Great Depression or the financial crisis. But what was it like to invest under those conditions?

A good example would be the book The Great Depression: A Diary. It is based on a lawyer’s journal and shows the difficulty of doing business when banks were failing and the future looked bleak. It also highlights the upswings, the moments of hope, which were inevitably crushed by another downturn. Above all, it allows the reader to understand why members of that generation would have difficulty believing in long-term bull markets again.

I’ve started a similar project of sifting through investor letters year by year, looking for insights, wisdom, and such firsthand impressions of history. Unfortunately, it is difficult to find collections of letters by great investors (whose names are not Buffett or Munger). They’re often either not made public or were never digitized and are tucked away in private archives (hopefully they’re not lost).

I’ve started working on letters by Bill Miller and tweeted a few of his thoughts already: on concentration and whether you should sell the Michael Jordan of your portfolio, his comment on Julian Robertson’s closing of Tiger at the top of the dotcom bubble, and on when to sell.

While mutual fund correspondence enters the public domain, that is not the case for hedge fund letters. Unearthing lessons from the likes of Julian Robertson would be a gift. In the meantime, we have to make do with public sources.

The following is an account of Julian Robertson during the crash of 1987. It is based on excerpts from his letters that were published in Outstanding Investor Digest, the book Julian Robertson, A Tiger in the Land of Bulls and Bears, and articles in Barron’s.

Whereas Paul Tudor Jones anticipated the crash and profited from it, Robertson found himself in the difficult position of navigating a fierce drawdown. Robertson, a rising star, shared Jones’s view of the Japanese bubble. But he discounted the growing bearish voices in the US. The crash was a defining moment for markets and a gut punch for his fledgling fund - the biggest test of his process and conviction yet.

Rising Tiger

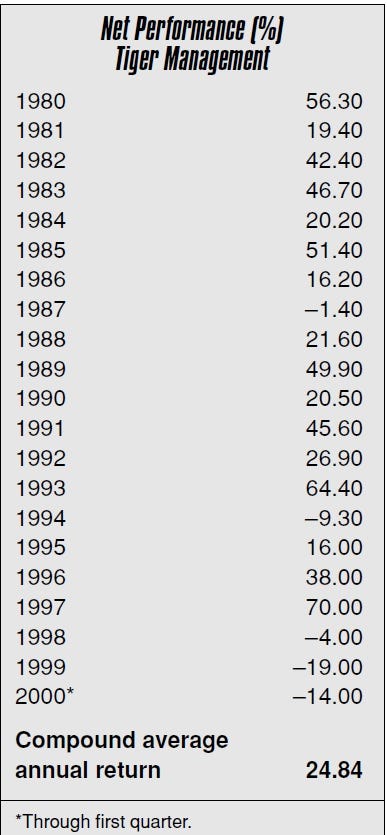

Robertson started his career as a broker at Kidder Peabody. He left in 1980 to start Tiger with $8 million in assets. While he added global macro bets over time, at his core Robertson was a value-focused stock picker.

In 2000, he commented that “the key to Tiger's success over the years has been a steady commitment to buying the best stocks and shorting the worst.” In a 2008 interview, he noted that he had started out as “a cheapskate looking for dirt-cheap stocks.” Over time and with “many talented analysts,” he realized “it was better to go for more expensive growth stocks because the analysts could project earnings well into the future. If you have high assured growth, the price-to-earnings multiple really has to be out of sight for you to be taking much risk.”

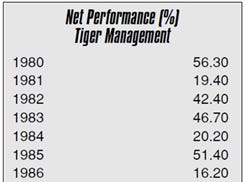

By early 1987, Robertson was still a traditional value investor and had built a remarkable track record:

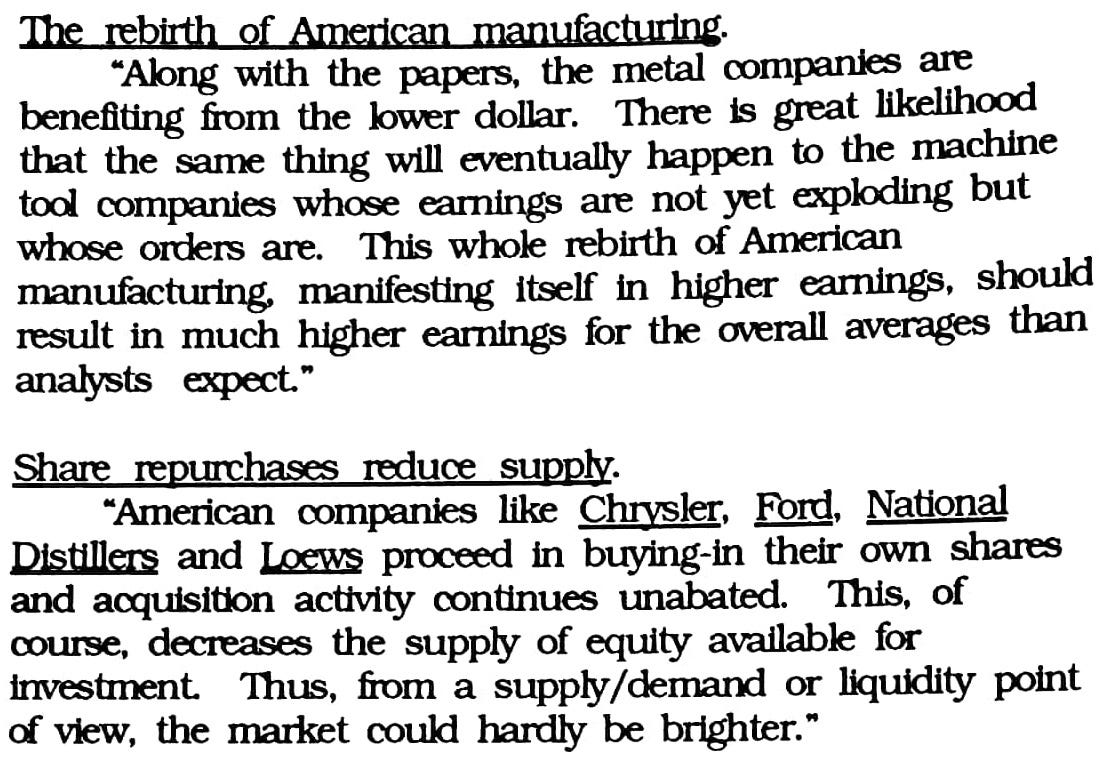

While Robertson saw a bubble in Japan, he found value in American markets. He expected Japanese investors to recognize the valuation discrepancy which would lead to “potential Japanese investment in American equities.” The dollar had been declining which Robertson expected to work “magic among manufacturing companies.” He saw a “rebirth of American manufacturing,” and expected “exploding earnings” among his companies. With a combination of cheap valuations and active share repurchases he felt optimistic about his portfolio holdings such as Jefferson Smurfit, a forest products company “selling at only 10 times 1988 earnings.”

1987 started off well and the fund was up about 20 per cent by March.

Japan

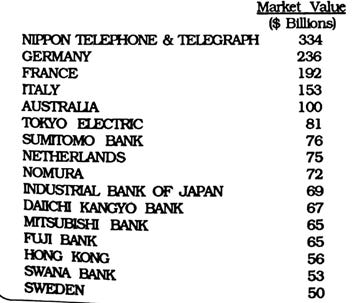

Robertson highlighted the excess of the Japanese bubble. Valuations were out of control with Nippon Telegraph selling at “about 250 times earnings,” exceeding the value of entire stock markets of nations like Germany and France.

The bubble was also visible in leverage, with Japanese treasurers buying stocks by “placing available funds in the market on margin.” Robertson saw the “same irrefutable logic that developed into Holland’s tulip mania in the late 1600s and the 1982 bust in Kuwait.”

He expected the Japanese market to fall before the US market, offering “some warning signs before the inevitable downturn. That warning should come … in the form of a severe crack in the Japanese market.” Robertson viewed his Japanese shorts as an “insurance policy.”

The crash

By September, Robertson wrote about growing bearish sentiment on Wall Street, noting “a great hue and cry around the investment community” about high stock prices. He noted that “almost everyone is looking for an excuse to sell stocks” or hedge “in the event of a severe break.”

However, he reiterated the “excellent values available in today’s market” and therefore in his portfolio. These included “Metropolitan Financial … at 44 per cent discount to book value and at less than 4x earnings” and “recently authorized [re]purchase of 10 per cent of shares.”

In October, he interpreted the growing bearishness as a contrarian bullish signal: “I do not see great danger of a drastic market decline until we all get a great deal more complacent.”

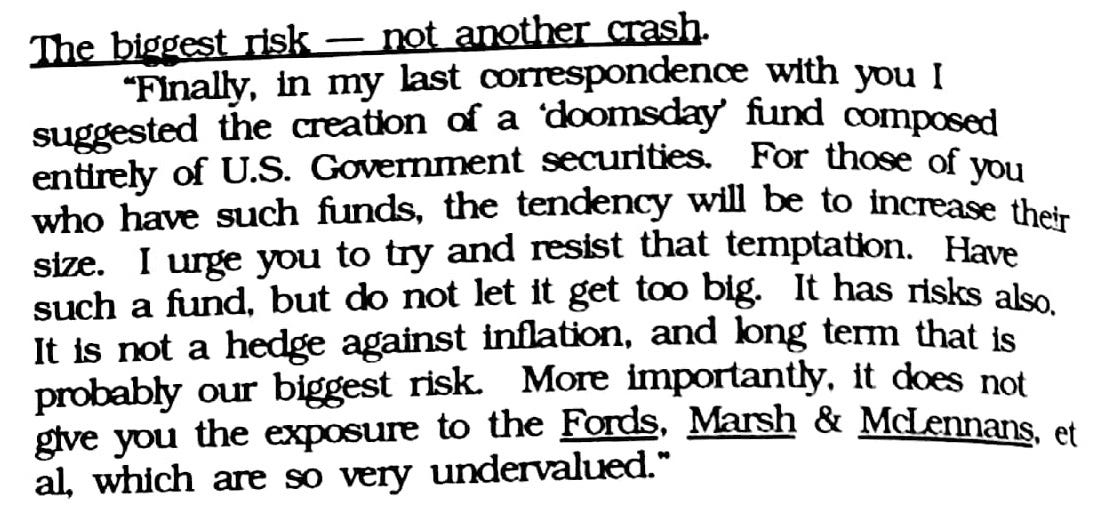

Any worried investors he advised to maintain a “doomsday fund” of safe investments

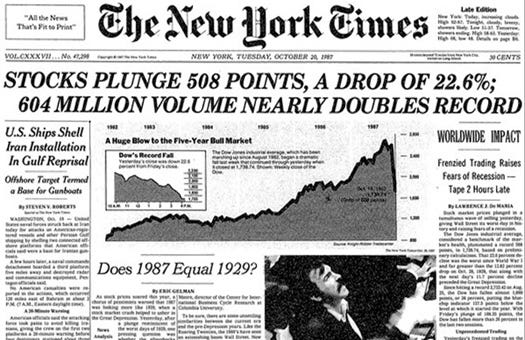

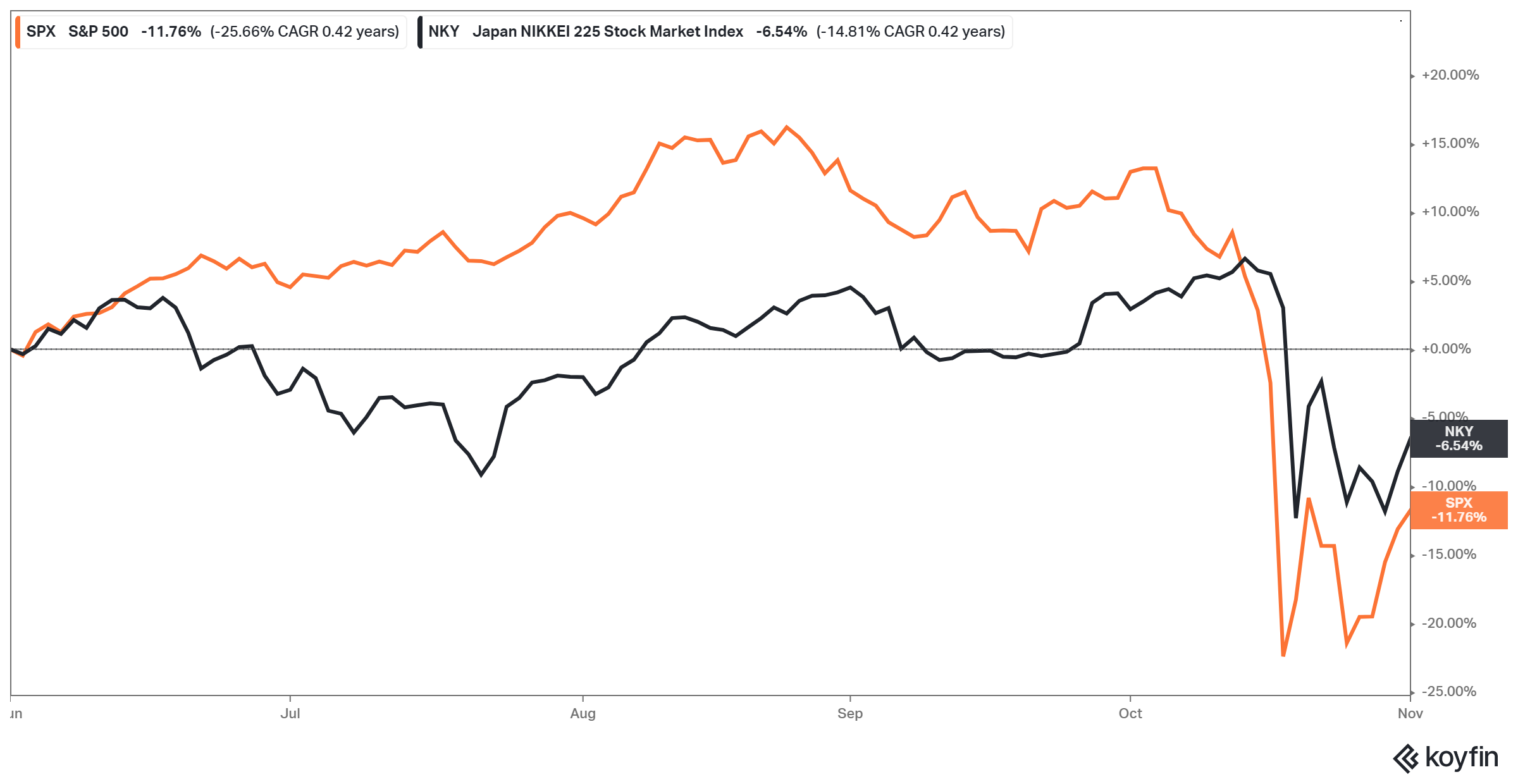

Despite, or perhaps because of, the lack of complacency, the market unraveled shortly thereafter. On Monday October 19, the Dow Industrial fell 508 points, or 22.6 per cent. The combined losses of Monday and the preceding Friday were 30 per cent and erased the year’s gains for a year-to-date loss of 8.3 per cent.

Mea culpa

In his November 10 letter, Robertson broke the bad news to his investors: his fund had declined 30 per cent from September 30 to October 31. “Probably none of us have ever lost so much money so fast in our lives,” he admitted. He was “shocked” and wondered what to do.

Being long the US market and short Japan, Robertson’s portfolio had significant basis risk: long and short positions were mismatched. And instruments he had added to hedge during a calm and liquid market were suddenly illiquid and expensive to exit.

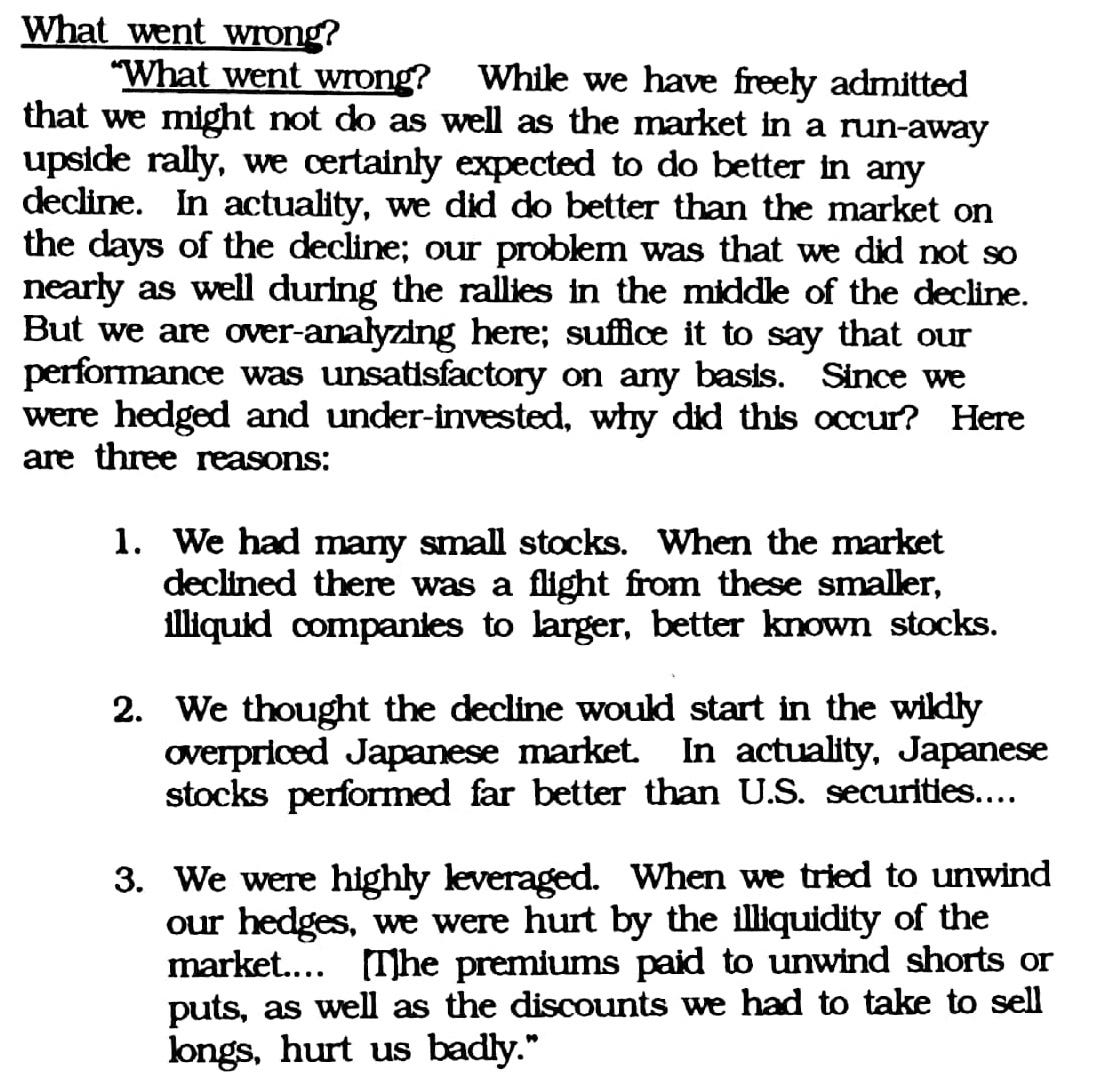

Robertson identified three key factors that accounted for Tiger’s poor performance:

The fund was concentrated in small caps when the market experienced a flight to quality.

Tiger was short the Japanese market, expecting it to break first. But Japanese stocks performed better than U.S. stocks.

The fund was leveraged which was costly to unwind in the chaotic market environment. Tiger cut back its gross exposure from around 250 per cent before the crash to 162 per cent (115 per cent long, 47 per cent short).

Now what?

Robertson noted the damage inflicted by the “sudden erosion of capital” was not just financial but also emotional. He had to make decisions. What was the right next move: protect his investors from further losses or go on the offensive?

The emotional response would have been to give into fear. “In my last correspondence I suggested the creation of a ‘doomsday’ fund,” Robertson reminded his investors, before warning them: “the tendency will be to increase their size. I urge you to try and resist that temptation.” The doomsday fund was risky in a different way: it was exposed not to the sudden volatility of a market crash, but to the steady erosion in value through inflation which Robertson called “our biggest risk” long term.

Robertson believed that sentiment had turned very bearish, that people expected “the collapse of the stock market will lead to recession or worse.” He disagreed and doubted that the crash would tank the economy. He pointed at “the other 80 per cent of America” whose “main asset is their home.” In fact, he argued, lower interest rates and a cheaper dollar would positively impact the economy.

“I am not quite sure what will happen next,” he admitted. But looking at his portfolio, he was bullish. “But I know that Ford Motor Co. is a value at four times earnings and twice cash flow.” Another holding, West Fraser Timber, was “a value, family-owned, sells at only fractionally over four times earnings, three times free cash flow.” He stuck by his north star: value investing. “There are great values around – we should do well.”

While the fund would, for the time being, “keep a conservative posture,” Robertson believed things were “setting themselves up for one of the major buying opportunities of our time. Industrial America has not been this competitive with the rest of the world in years.”

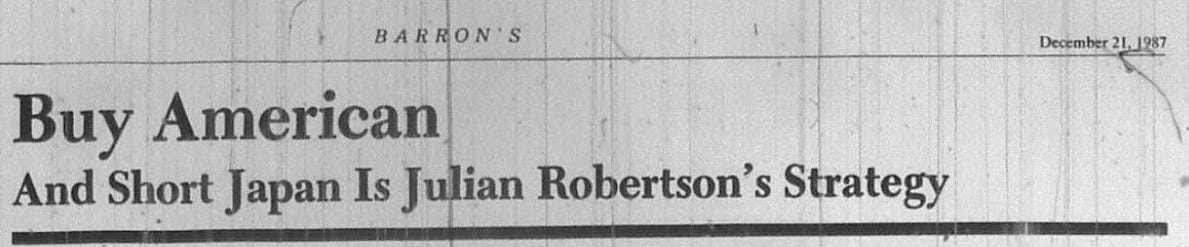

In December 1987, he sat down for a rare interview with Barron’s. He reiterated his mea culpa: “I would love to say we did as well as we thought we would have. We did not. We thought the break would come in Japan first. And we were in a lot of smaller companies and our leverage hurt us, too.”

He was still bearish on Japan, which he called “absurdly overvalued” and “practically the only place where we can find good shorts now.” If Japan crashed, it would be “very bearish for markets all over the world” He compared Japan Airlines, trading at six times book value and “infinity times operating earnings,” to American Airlines at two-thirds of book and 7.5 times earnings. “It just doesn’t make sense to me,” he concluded. “There’s never been one of these things that’s succeeded.”

Still, bottom-up research in the US told him to be long. After cautioning that “we are more stock pickers than market judges. We don’t make big market bets,” he outlined his bottom-up, bullish outlook. He was having “a very difficult time finding shorts at the present time.” And after reaching out to his portfolio companies, he found the real economy doing well: “I don’t talk to anybody in industrial America who isn’t absolutely tonning it. I’m talking about smokestack America. They are making a fortune.”

This disconnect between a healthy economy and a bearish market made him utter a legendary quote:

“There are so few bulls that I can’t imagine who’s going to impregnate the cows.”

A question to ponder

We can take away several lessons:

Intellectual honesty: Robertson did not make excuses for the poor performance. He laid out the reasons and mistakes, then explained his strategy going forward.

No style drift: Robertson took a more defensive stance and lowered his fund’s leverage. But there was no change in strategy, no big new macro bet.

Back to basics: Robertson and his team stuck to their bottom-up research process and looked to business leaders for real-time information on the economy. When they found business activity to be healthy, they had confidence in holding their undervalued stocks.

Maintaining conviction: Only a couple of months after the most dramatic loss of his career, Robertson talked about “one of the major buying opportunities of our time.” There was a lot of blood in the streets, and he told his investors that raising more cash was exactly the wrong thing to do in a world flooded with bargains.

The most important question to ask ourselves is whether, as investors, we would have stuck with Robertson. After a string of good performance, he found himself ill-positioned with a wrong-way macro bet. Investors counting on his hedge fund to weather the crash must have been shocked to see how much he lost over the course of a month. Would we have stuck with him? Would we have trusted his judgment and backed his conviction to stay the course? Would we have resisted the siren song of bearish sentiment?

Enjoyed this piece? Let me know by hitting the ❤ like button.👇 Thank you!😉