Statistically Speaking, You Are The Patsy

When betting against capitalism, you can never take your eyes off the ball.

Hello everyone,

Of course by ‘you’ I don’t mean my dear readers, but shareholders of the average company. This is a little counterintuitive because we know that historically and over the long-term, the stock market has produced an attractive return. Yet most individual companies have not.

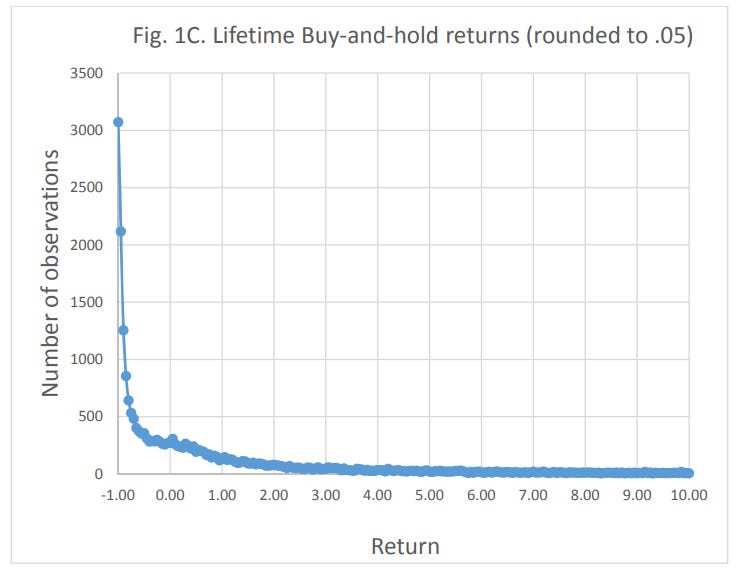

Hendrik Bessembinder has done the work on this (original paper and 2020 update). A small number of outliers was responsible for the vast majority of market gains.

The best-performing four percent of listed companies explain the net gain for the entire U.S. stock market since 1926, as other stocks collectively matched Treasury bills.

And “four out of every seven common stocks” returned less than one-month Treasuries. Markets do well, but the average stock does not.

When analyzing individual companies, there is a disconnect between our expectations and this base rate of performance.

Consider how investors value companies. We are trained to think about intrinsic value as the present value of the company’s future cash flows. This is of course technically correct. But it bumps up against reality.

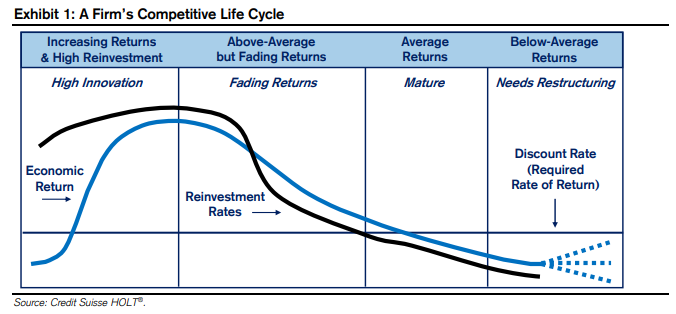

I find it useful to think of companies as organisms. They operate in an ecosystem and they are subject to both a life cycle and natural selection. Some are resilient and adaptable, but most perish rather quickly. Eventually, they will be replaced by an entity better adjusted to the changing environment. Public companies have typically achieved reasonable size and are often mature, if not in decline, already.

But when projecting cash flows, investors collectively fall into a mental trap of optimism. Unless a business is already in terminal decline, people rarely model the free cash flow to taper off. Instead, businesses that should be expected to fail over time are being collectively valued as if they were going to experience perpetual growth alongside the economy.

“I don’t want to look at other's projections. I’ve never seen a projection from an investment banker that didn’t show the earnings going up over time. And believe me, earnings don’t always go up over time.” Buffett in 2011

The second issue with discounted cash flows is that public shareholders are last in line to receive them. As an extreme example, Ben Graham used to invest in companies that traded below their net current assets as these could be liquidated and the cash be distributed to shareholders. While that does happen on rare occasions, it is more likely that the company organism will fight to survive until it has exhausted all of its energy and fails. The tail of cash flows ends up captured by management, employees, and creditors.

One way to think about an investment in a public company is as a combination of two bets: a bet on the company’s future and a bet that shareholders will get their share of said future despite a lack of control.

Another way to think about the investment is as a bet against competition, innovation, unions, other industry players trying to capture more of the value chain, and management’s greed or lack of integrity. Shareholders forget that capitalism, in the form of competitors, innovators, and insiders, is happy to eat their lunch.

On top of that, investors bet against all sorts of forces and unforced errors that can kill a company: bureaucracy and complacency, empire building, bad risk management, leverage, and plain old strategic mistakes. Competitive moats, corporate cultures, and customer goodwill built with great effort by generations of employees can be blown up with a few terrible decisions.

Munger once commented that if he were to teach at business school, he would do it through charts. He would “try and relate the changes in the graph and in the data to what happened in the business.” That’s a very useful idea and I am surprised there is no central repository with the charts of failed companies (does anyone know where to source this data for companies that have long gone under?).

Nothing sharpens one's sense for risk like a chart showing a once great company getting wiped out.

DISCLAIMER. I write and podcast for entertainment purposes only. None of this is investment advice and any information contained in my work should not be relied on to make investment decisions. Do your own work and seek your own financial, tax, and legal advice before making any investment decisions.

Invert!

Because the stock market has done so well, it can be tempting to think of public companies as shareholder enrichment schemes. Instead, they can be schemes to enrich others at the expense of shareholders. To see markets clearly means to fully grasp that you are not guaranteed a fair handshake. Buffett grasped this in the 1970s:

The essence of Warren Buffett's thinking is that the business world is divided into a tiny number of wonderful businesses well worth investing in at a price and a huge number of bad or mediocre businesses that are not attractive as long-term investments.

I believe this leaves the non-controlling public shareholder investor with three options (it’s a different game for controlling investors):

Be a long-term ‘business investor’. Identify a group of wonderful businesses that will compound long-term and are shareholder friendly and priced attractively as investments.

Trade securities. Whether your timeframe is a few seconds or a few years, you trade the security as opposed to becoming a long-term partner in the business. People make a lot of money long and short as companies go through their life cycles, but value investors of the Buffett and Munger school can get uneasy with this notion. It can feel a little stigmatized. But once you realize that most companies are not attractive long-term investments, this approach to the market seems perfectly rational. That said, if trading is a losing game on average, it brings us to the last option:

Opt out of the game. Stop trying to pick long-term winners or trading the bag of future losers. Invest in an index that, over time, allocates more to the winners and cuts the losers. Accept that at any point in time you are buying some great companies above their fair value as well as some awful companies that are about to go under. It’s just a cost of doing business

You can of course mix these options, be an investor in some companies and a trader in others. But what you must never do is confuse them. Don’t allow ideology to turn you into a long-term investor in a company that will destroy shareholder wealth.

And if you decide to play the game, if you actively pick securities, you can never truly take your eyes off the ball. Survival and prosperity are not guaranteed. Even wonderful companies will decline eventually. They may prosper and reward you, and possibly even your descendants, for a long time. But they will not flourish forever. And there is no need to stick around for that.

Thank you for reading,

Frederik

We don’t have to do many things that work. One or two things every now and then that work really well. That’s the beauty of this business. [But] you can’t have a big disaster. That is what we try to avoid. We do not ever want to lose a significant percentage of Berkshire’s net worth.

"One way to think about an investment in a public company is as a combination of two bets: a bet on the company’s future and a bet that shareholders will get their share of said future despite a lack of control." That last part seems to be what most people overlook, you are (as Whitman called it) OPMI -- Outside Passive Minority Interest, so you are in a disadvantaged position from the get-go.

Great essay. Thank you.