Stanley Druckenmiller, Part 1: The Young Gun Finds His Game

“I’ve always loved to play games, and face it, investing is one big game. You need to be decisive, open-minded, flexible and competitive.”

Hi everyone,

I’ve decided to break up my longer profiles and experiment with shorter, serialized posts. This should allow me to publish more frequently, more consistently, and with more variety. Today, we’re going to take a first look at Stanley Druckenmiller and his early days.

Today’s sections:

A legend stumbles

The intuitive trader: an anachronism?

Finding the great game

The first mentor

Key lessons: motivation, passion, and competitiveness; developing a personal style

A legend stumbles

"I never thought the Nasdaq would drop 35 per cent in 15 days. This business is a bit like a drug. When you are doing well, it's hard to quit." Stanley Druckenmiller

In March 2000, Stanley Druckenmiller was glued to the screens in his office at Soros Fund Management in Midtown Manhattan. The dot-com bubble was still underway, with mind-boggling volatility. Watching as a biotech stock skyrocketed, he turned to a fellow trader: “This is insane. I've never owned a stock that goes from $40 to $250 in a few months.”

Druckenmiller had been competing to beat the market since 1981, trading everything from equities to bonds and currencies. The New York Times once dubbed him “Soros’s Alter Ego.” But now it seemed he was losing his edge.

In 1999, he tried to call a market top and shorted $200 million of high-flying technology stocks. His Quantum fund promptly lost $600 million and started the year down 18 per cent. To climb out of the hole required a herculean effort. To find religion Druckenmiller attended the Allen & Co. Sun Valley Conference. Afterwards, he hired two young stock pickers who were not afraid to buy “all this radioactive shit that I don’t know how to spell.”

The move was a textbook example of his mental flexibility and Quantum ended the year up 35 per cent.

But Druckenmiller remained uneasy. By early 2000, he worried the bubble could burst at any moment. Finally, he walked into George Soros’s office: “I’m selling all the tech stocks, selling everything. This is crazy.”

“I’m really glad you’re doing it,” Soros replied. “I haven’t been comfortable with this.”

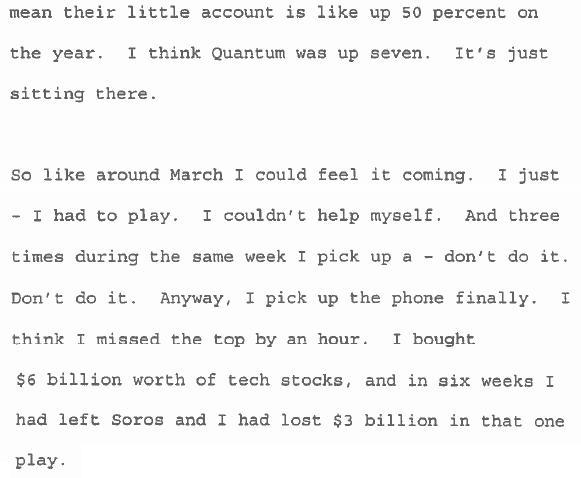

At the same time, the Wall Street Journal noted that Druckenmiller had lost more than $1 billion over two years in bets on the euro. He had also missed out on a new macro theme: the rise in oil prices. Meanwhile, the dotcom bubble kept going and his two young gunslingers, trading smaller portfolios at Quantum, were already up 50 per cent for the year. It was driving him nuts, as he later recalled.

“I just had to play. I couldn’t help myself. Three times during the same week I pick up a - don’t do it. I pick up the phone finally. I think I missed the top by an hour. … and in six weeks I had left Soros and I had lost $3 billion in that one play.”

On April 28, with the Nasdaq in freefall, George Soros called a press conference. He announced that Quantum was down 22 per cent and that Druckenmiller was leaving the firm. The fund would become a lower risk endowment-style portfolio with outside managers. It was the end of an era and of an iconic mentor-protégé relationship that had dominated the world of global macro in the 1990s. Michael Steinhardt once called it a rare “lasting Wall Street marriage.”

"It would have been nice to go out on top, like Michael Jordan," Druckenmiller said. "But I overplayed my hand."

One of the best traders of his generation fell prey to his emotions, his gambling instincts even. His career was deflated by a textbook bubble, exactly the kind of situation he and Soros had studied and exploited before. But why?

Keep reading with a 7-day free trial

Subscribe to Frederik's Age of Alchemy to keep reading this post and get 7 days of free access to the full post archives.