Q&A with Nelson Wu of Open Square: Energy and Uncomfortable Dinner Conversations

"That 'global energy crisis'? Yeah, that undoubtedly has begun."

Edit: Making this available for everyone, including readers of Open Insights.

Hello everyone,

Everything seems to revolve around the energy sector this year. I covered some energy credit managers at Aksia in 2019 and the mood was dire back then. Nobody was interested in allocating to the space. The pessimism created some opportunity as banks were selling off their exposure, credit spreads for new loans were high, and protection was good. However, portfolios were loaded with struggling companies, track records were messy after the bust, and few people thought the sector would return.

Compare that to this year when energy has been the only game in town:

© S&P Dow Jones, h/t Liz Ann Sonders

As my friend Tom Morgan wrote recently:

“The single consistent theme I’m seeing everywhere, is that energy capex has to recover from unsustainably low levels.”

“Vaclav Smil’s recent book, How the World Really Works (insights here). Essentially, he argues we’ve consistently failed to grasp the scale and energy intensity of the modern physical world.”

One energy-focused substack I enjoy is Open Insights, written by Nelson Wu of Open Square Capital. Nelson’s background is not in energy (he was an M&A lawyer). He is self-taught and simply very passionate and curious about the industry.

“After some digging, I realized there's probably an opportunity there given the structural shortage, and if demand kept rising, the prices should mean revert. Little did I know that would take pretty much the next 6 years!”

I am fascinated by people who pivot and apply their frameworks in a new sector with a blank slate. For example, this is how Nelson answered a question about tracking energy analysts’ predictions:

“For me, it's akin to deconstructing arguments and issues in a legal analysis, to understand where the crux of the issue lies. Once I become familiar with an analyst’s take, motivation, perspective, and style, it's easier to track them and understand why they're making the points, whether I agree with them, and when they pivot. The hard part is the heavy lifting that's done on the front end. It just involves a lot of reading and analysis.”

Nelson writes in an entertaining style (“What Not to Say at Polite Dinner Parties”) and if you’re interested in the topic I recommend you check out his work (which is mostly free!).

“Do you now see why I’m uncomfortable at these parties? It’s not just social awkwardness, it’s that I see tail risks coming, and despite all the well wishes and hopes and dreams for kids and their future, our global picture is about to get a whole lot dicier.”

I hope you enjoy this Q&A with Nelson!

Disclaimer: I write for entertainment purposes only. This commentary reflects a personal opinion, is not investment advice, and should not be relied on to make investment decisions. The views reflected in this commentary are subject to change at any time without notice. Do your own work and seek your own financial, tax, and legal advice before making any investment decisions.

Q&A with Nelson Wu

Q: Tell me about your background and how you came to be an active investor in energy?

NW: Unlike most hedge fund managers, I'm actually a lawyer by training. After graduating from UC Berkeley, I attended the University of Minnesota law school, then started my career in international tax at a Big 5 accounting firm. After a few years, I went in-house and worked in a few multi-national companies, focusing mostly on M&A, corporate structuring, international tax planning, corporate law, contracts, etc. My last company, Allergan, of the Valeant/Bill Ackman/Actavis fame, was acquired and I exited the corporate world. With some seed money and friends/family as backers, I started the fund, something I've always wanted to try. The energy theme was something that I fell into. At the time I formed the fund (late-2015), oil prices had just collapsed, and a former colleague of mine asked about oil prices in an off-handed way.

After some digging, I realized there's probably an opportunity there given the structural shortage, and if demand kept rising, the prices should mean revert. Little did I know that would take pretty much the next 6 years! Although it's taken a few years to play out (in violent fits and starts), I think it's finally beginning to turn. No doubt pushed along by the Russian invasion of Ukraine, but the underlying factors for a persistent shortage have always been there. With the Ukrainian catalyst, we're now off to the races.

Q: What sources / people were most helpful to you in understanding global energy markets?

NW: I honestly try to surround myself with a really diverse group of thinkers in the space. After all everyone's looking at more or less the same things, but the different perspectives really help me to frame the broader picture. I collaborate closely with HFI Research and other dedicated energy professionals, sharing and dissecting, and reassembling the vast amounts of data, and work with other fund managers, investors, operators, refiners, data service providers and other portfolio managers and buy/sell-side analysts to parse the data. I've been able to publish successfully on Seeking Alpha and our own substack account, and that's really helped broaden the network of people we can tap into.

Q: Global energy seems like a massively complex system which mixes markets and geopolitics. It seems to favor players with inside knowledge at oil producing nations or embedded into integrated oil companies. How do you think about competing and making predictions in such a market? How much conviction can you develop?

NW: It is very difficult. For an investor, it's inherently not just a sector bet, but it's also having to make a macro call and a micro call. How will the global economy perform? How does that inform demand? How will global liquidity adversely or beneficially impact that demand? Those are all questions you need to try to answer continuously. On the supply side it's a mixture of politics, shareholder activism, and labor/resource/capital constraints that impact whether more or less barrels flow.

Once you get those broad themes pinned down (to the best of your ability), then it's a matter of selecting the right companies and securities to express the thesis. So definitely agree on the "massively complex" portion of your question. Yet, if you invert that question, however, you realize that it deters many analysts from venturing into the space. So if you can make an incrementally better decision on those pieces, then ultimately you may have something. Supply and demand factors are difficult to judge, but if we keep grinding at the open-ended questions, then we can get to some inherent truths. Shut off capital, whether it's because of ESG and/or shareholder activism, you'll shut off supplies. Fiscally stimulate the global economy with fiscal and monetary largesse, you'll undoubtedly spur demand.

In some sense, it's following Elon Musk's idea to distil things down to first principles, and then rebuild from there. Truthfully, none of this is easy and the sheer amount of work means you have to be willing to dedicate the time to parse what's important vs. what's not, and collaborate with others to figure out the puzzle. If you are, then it can be fruitful because whereas other investors would put it in the "too hard" basket (a la Buffett), you can really discover some hidden gems. Interesting enough, Buffett just recently dove into that basket and purchased 20% of Occidental Petroleum, so maybe there's really something there.

Q: Do you track your own predictions/expectations?

Yes, because each prediction/forecast is a mile marker. Whether the thesis is coming true or not depends on whether we get those forecasts correct. Since it's a complex puzzle, we always want to make sure that each of the components are tracking to our expectations, and if not, why not. After that, we can then determine whether the deviation is material or immaterial. As an investor we have to be very humble, and we have to acknowledge that there are many things in the theses that we won't know, but if XYZ does happens, then we're on the right track, so it's crucial to set-out the XYZ beforehand.

Q: Is it fair to characterize your macro view as that of an impending "global energy crisis"? I've seen this from several funds and analysts - can you explain what it means to you in a nutshell and how likely you think it is?

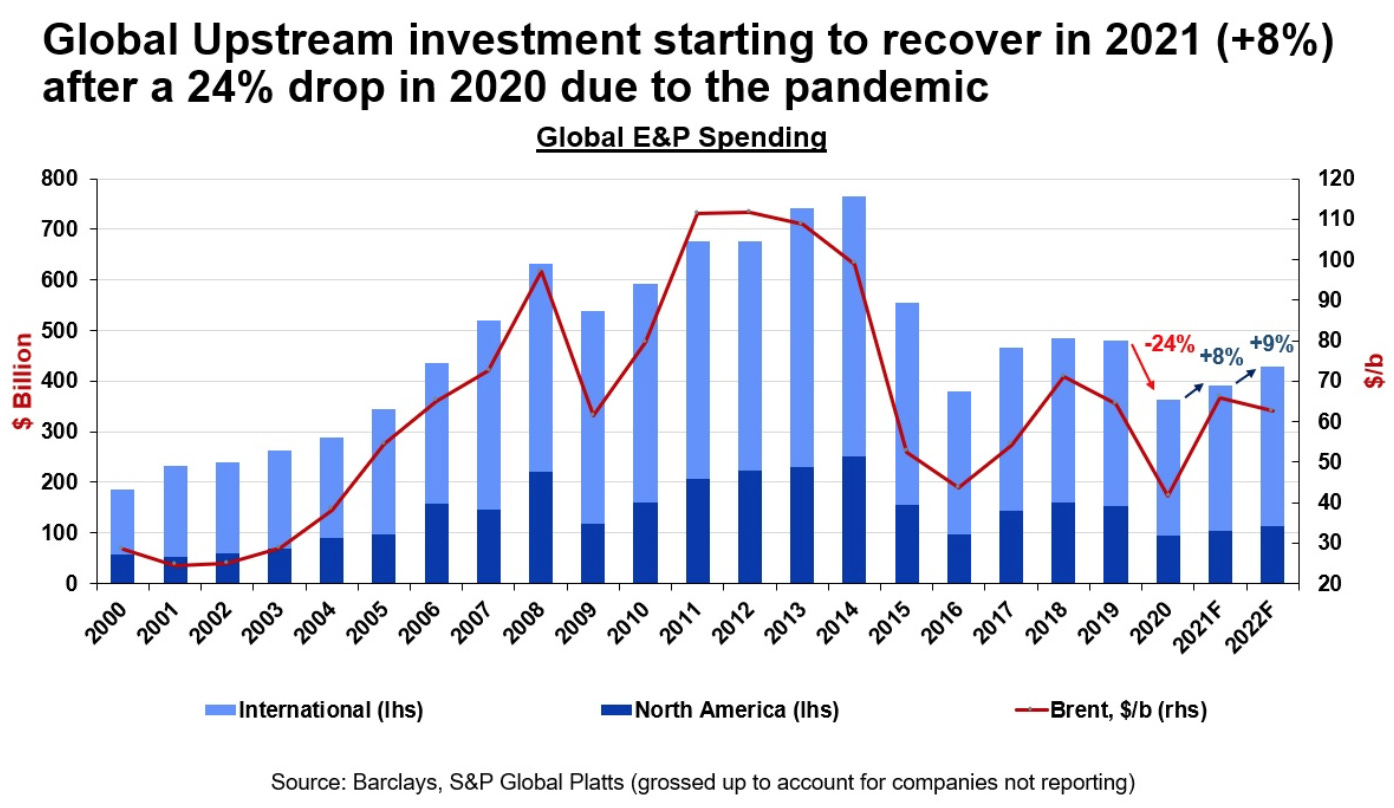

Well, I'll use a statistic borrowed from Goldman Sachs. In 2014, energy producers spent a collective $1.3T on energy investments, and in 2020 it was $800B. If you think 2020 was artificially low because of COVID, it's actually fairly close to what we've been spending since oil prices collapsed since 2014. Said another way, prior to 2014, we spent over a trillion a year investing in long-lead energy projects, but for the last 6-7 years, we've spent only half of that.

Now you can blame ESG, environmental activism, poor corporate returns, abysmal returns on investments, etc., but the fact remains, we have been woefully short in committing capital to this space. Oil and gas wells deplete, an the reservoirs they reside in decline. New wells need to be drilled to replace the declining production of older wells and new fields need to be developed to supplant older fields, yet little of that has happened in the capital constrained sector. Attached is a Barclay's chart from a few years ago illustrating the fall (on the upstream side). So one or the other has to be true, either we overcommitted capital for no reason prior to 2014 to produce energy, or we're under-committing capital today. We think it's the latter.

Even before the Russian/Ukrainian invasion threatened the flow of energy (i.e., because of government and/or self-imposed sanctioning), we were anticipating that the world would be collectively short 1-2M barrels per day (bpd) (one in which we consume ~100M bpd of oil). A 1-2% shortage, should already garner triple digit oil prices. With the Russian/Ukrainian sanctions, we're looking at nearly double that amount heading into H2 2022. Energy prices, specifically oil, has yet to reflect the true price of what's coming (either in price or in how long the higher prices will last). We think the release of strategic petroleum reserves coupled with China's recent COVID flare-ups are suppressing the market demand, and when both fade by the summertime, we'll be left with an even tighter market, less "winter stores," and a smaller buffer for emergencies. As base production levels further decline into 2022 and beyond (because of underinvestment), we're looking at even tighter markets not just into year-end, but for years to come. That "global energy crisis"? Yeah, that undoubtedly has begun.

Q: The energy sector and energy have already rallied a lot. At this point, what are the key actors and data points do you watch most closely?

While it's true that the energy sector has rallied off the lows, we expect there's much more upside to go. What few people understand is that we're facing a structural issue and not a cyclical one. Outside of a few million barrels of spare capacity (located primarily in the Middle East) we're largely tapped out from a supply standpoint. We can thank years of low/negative returns, ESG, and high volatility for scaring off many investors from the space. With fewer investors, we're seeing lower capital investments, and that underinvestment has ultimately constrained supplies. Throw into that equation the COVID black swan, and we're now dealing with the unintended consequences. As we like to say, tail risk events also beget tail risk consequences. What started as a cyclical issue, morphed into a structural issue, that was then compounded by a black swan issue.

So even though energy has rallied, we haven't seen the full impact. At this stage we're monitoring the actual barrels, oil/NG, etc. are physical commodities, and that will inevitably drive pricing. It disciplines the financial markets, so focus on that, get that physical side correct, then the pricing of the commodity, and in turn the investment vehicle (whether stocks, bonds, etc.), will play itself out. As for actors, OPEC+ and their policies are what to watch out for right now. We think the US administration is more motivated to repair its Saudi relationship than it is to incentivize US producers in drilling more, simply because doing the latter would anger environmentalists, a core constituency they need to hold onto going into the midterms. So for now, let's all watch what OPEC+ will do, and how much spare capacity they'll release to the world.

Q: What would invalidate this view?

If demand falls off catastrophically that would certainly delay the thesis. If producers (e.g., public, private, OPEC+, etc.) collectively decided to produce more and invest for the future, then the deluge of supplies could tame oil prices rather quickly. Yet, for various reasons, it's unlikely any of that will occur. For private and public companies, shareholders today are demand now constrain production. Stakeholders have emphasized a return on capital in addition to a return of capital. This has driven almost every management team/board of directors to promise shareholder returns.

By extension, this means even though oil prices have increased (as have free cash flows), companies are looking to dividend the cash out and/or buyback shares. There's little appetite to plow the profits back into the ground. Add that to public pressure from ESG, we can see why production growth has stayed muted. Similarly for OPEC+ producers, Russia is sanctioned, and Saudi Arabia (and Gulf Coast countries) are more concerned with maximizing oil prices, especially as the "days of oil" are coming to an end (or at least so says the media). Moreover, many of these countries recognize that to stay relevant and maintain their geopolitical influence, oil prices need to stay high. Otherwise they can be shunned or discarded in a low price environment. Look no further than Saudi's Crown Prince, Mohammed bin Salman. So whether it's stakeholder demand, geopolitics, economics, producers preserving spare capacity in case there's outages (e.g., stemming from attacks), or pure pettiness, there's just little appetite to increase production materially.

As for demand, sure the global economy could fall off, but that means we need to perform a sensitivity analysis. If it does, do we/should we assume a minor fall? A major fall such as the Great Financial Crisis ("GFC"), or something even larger? Even if we used the GFC as a low (i.e., -2.7M bpd in the worst quarter), we would still be short supplies, and if we didn't, then our supply gap widens. Lastly, oil demand is very inelastic, people still need to commute, things need to be delivered, and goods need to be manufactured. In the end, that inelasticity reasserts itself, and consumption climbs. So for us, yes we have to assume demand falls a bit, but it's again a range and may not necessarily invalidate the thesis.

Q: How do you pick stocks (or ETFs) in energy?. What do you look for?

We typically invest in energy stocks. We'll occasionally trade the ETFs, but that's more of a directional call on something short/medium/long-term. Outside of betting on the commodity itself, the equities of E&P producers offer pretty compelling risk/reward tradeoffs. We primarily look for free cash flows and balance sheet leverage. Having done this awhile, we've already modelled most of the E&P companies. There really aren't that many in the public sphere, and eventually you can grind the numbers out. It's frankly old fashion "rock turning." We then deduce the quality of their management teams, and once comfortable with everything, take the position.

At current production levels many of the producers have years of inventory left, but that's neither here nor there as the market isn't ascribing much value to those assets. It's only really looking at cash flows and even then only giving us partial credit for today's high oil prices, believing this will all turn lower shortly. Eventually the market will rerate these stocks once the world realizes that the issues are structural in nature, and that oil prices are here to stay for awhile. Then we'll go from valuing these companies at a discount to their current cash flows, to valuing them as producers with valuable (or invaluable?) inventories. Right now, it's still a shunned corner/sector of the market, representing ~5% of the S&P 500 in terms of value, but generating ~9% of its profit. We're not anywhere close to full value.

Q: Do you see this as a long-term investment opportunity or are you looking to catch a limited leg up? At what point or under what circumstances would you exit?

If we're right, then this will last for years. The dearth of investments for the past 6-7 years means that the repercussions should last just as long and severe, if not more. This is after all a depleting resource, which we have to constantly renew. We've only had triple digit prices for 6 weeks, whereas we've underinvested for 6-7 years by nearly $2-3T. So yes . . . we have a long way to go.

Q: Are there any investors, CEOs, analysts or others in the space whose views or actions you track closely?

I frankly track as many people as I can. So for instance, there's always a range of opinions. Some shops tend to be more conservative than others. Sell-side tends to have a view, data service providers another, and buy-side PMs another. It's helpful to layer on government/quasi-government analysis as well (e.g., EIA, IEA, OPEC). Once you understand what their assumptions are, you can then decide whether they make sense or not. I tend to look for government/quasi-government data as the starting point. Most use the IEA's figures, and we think that works. Then start layering other analysts assumptions, after which you can see where they fall in a "dot plot" of sorts. After you beat up their assumptions (and create mile markers for them to see if they're on track), you can then decide where you land.

For me, it's akin to deconstructing arguments and issues in a legal analysis, to understand where the crux of the issue lies. Once I become familiar with an analyst’s take, motivation, perspective, and style, it's easier to track them and understand why they're making the points, whether I agree with them, and when they pivot. The hard part is the heavy lifting that's done on the front end. It just involves a lot of reading and analysis.

Q: What has been your experience running a fund as a solo operation? What does a typical day look like and what takes up most of your time?

It's been a really thrilling, enlightening, all-consuming, at times exhausting and fascinating/fun experience. I've told other aspiring managers that starting and running a fund is essentially throwing yourself into the start-up world. It's not just the investing side that's important, but you're also creating a product that you have to market, advertise and sell. It's the difference between practicing a craft/hobby vs. creating a business. On the investment side, managing assets for other people is also a wholly different experience than running money in your own personal portfolio. The psychological pressures and emotional swings are more intense, especially if you place significant importance on being a fiduciary of the funds, which I do. I worry more about my LPs capital than my own, and I think that's the right way to think about it.

I also tell new fund managers that you have to be brutally honest with yourself about what you're good at and what you're not good at, so you can course correct whenever challenges come up (and they almost certainly will). Managing outside money means that everything is usually magnified, emotionally and psychologically, and the up/down cycles of the market will fully expose a manager's weaknesses, so you have to be humble enough to admit fault, address the issue, and move on. So you have to balance ruthless honesty with yourself, humility and grace. Lastly, you have to surround yourself with some great people, colleagues, friends, or confidants that you can bounce ideas off of and vent to, when you need an outlet. I've been fortunate to meet many of those through the years, and am forever grateful for them in generously sharing their time.

Most of my day is spent researching and writing. I typically try to wake up with one or two questions I'd like to answer by the end of the day or week. How does XYZ work, who puts together the data, how's the data constructed, how does something fit into this puzzle. So one question a day, one answer a day. It usually guides my day, and I get to spend some time digging into something. So for instance, today I was wondering why people use the 2/10 Year Treasury spread vs. the 3 month/10 Year Treasury spread to see if they can forecast a recession. It's typically something "niche" or esoteric like that. Once I learn the reasoning, I move on. I like to think that Charlie Munger and Buffett are right, that knowledge just compounds, so today it's Treasury yields as a predictor, then tomorrow the components of CPI, the next PPI, etc. etc. Eventually that day-to-day grind helps you build out a bigger/broader picture of the world, and adds another toolkit in the box as an investor. So one question a day.

Q: Where can people earn more about your work?

I write a weekly article on my substack account: Open Insights.

Occasionally I will also publish on Seeking Alpha as Open Square Capital. Many of my prior essays/analysis can be found on those two sites. They're just an extension of my research. I figure if I can explain something clearly to an audience, then I'll have a better understanding as to what it is.

Thank you so much, Nelson!

/ Twitter")

Wow, that Open Square newsletter is a gem. Burning through their posts.