On The Other Side of Bubble Mountain

With Paul Singer, Todd Combs, Sam Zell, George Soros, Warren Buffett, and Michael Burry

“An extraordinary confluence of extremes and problems have made possible a set of outcomes that would be at or beyond the boundaries of the entire post-WWII period. Investors should not assume that they have ‘seen everything’. … The world is on the path to hyperinflation, which is the direct route to global societal collapse and civil or international strife. It is not baked, but that is the path that we are treading. Uplifting, right?” Paul Singer, Elliott Management 3Q22 letter

“More than any other time in history, mankind faces a crossroads. One path leads to despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly.” Woody Allen

About a year ago, I watched people smash toilets and party at the crypto conference NFT New York. This now feels like a fever dream from another life. With FTX submerging (the “next Buffett curse” has struck again) we are, in the words of Elliott’s Paul Singer, on “the other side of the bubble mountain.”

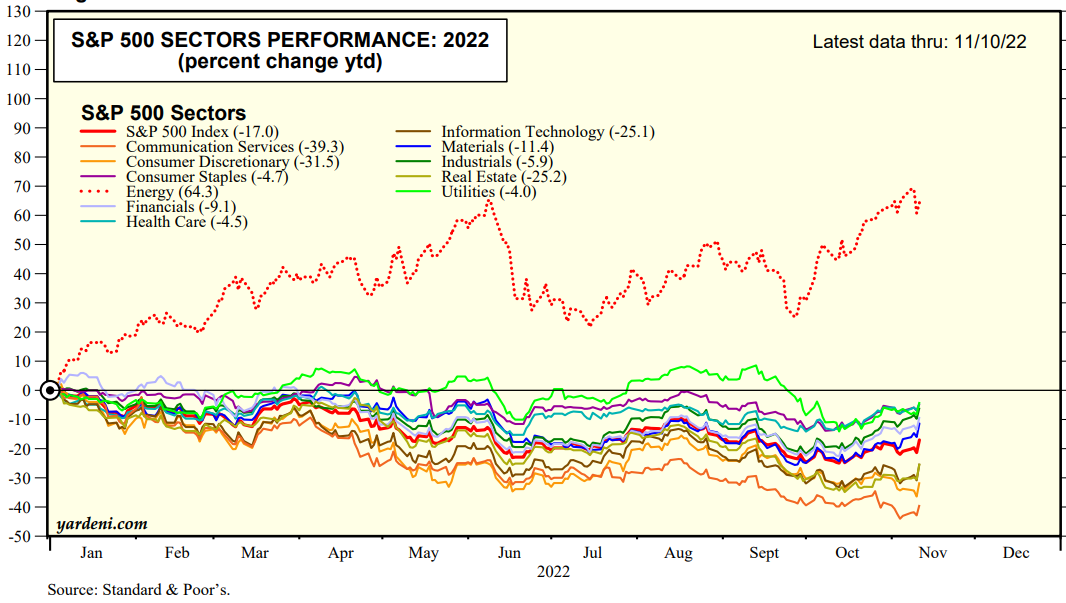

It was easy to be wrong in 2022 (energy is the only sector up on the year!).

And news flow has been especially noisy (war, Twitter takeover, inflation, Fed, election, pay attention!). It’s been a draining year for many. Exhibit one is a viral tweet, a George Soros quote about working less.

“I don’t like working. I do the absolute minimum necessary to reach a decision. There are people who love working. They amass an inordinate amount of information, much more than is necessary to reach a conclusion. They become attached to certain investments because they know them intimately. I am different. I concentrate on the essentials. When I have to, I work furiously because I am furious that I have to work. When I don’t have to, I don’t work. This has been an essential element in my approach.” George Soros

I took the quote’s popularity as a sign that investors are getting just a little bit tired and burned out.

Because the nuance is that Soros combined his trading instincts with the “furious work” of his analysts. Early on this was Jim Rogers who once described his process as follows:

“If I owned airline bonds, I would have visited all the airlines, I would have spreadsheets on all the airlines, I would have been to the trade associations, I would have been to see Boeing, I would have been to see Airbus. I would have done an enormous amount more work and have been sitting on top of it every day. I would have been watching every tick, every trade—not trading them, but just so that I would know what is happening.”

It’s easy for the Jim Rogers-type analyst to get exhausted after this kind of year.

In the words of Monty Python, it’s time to bring out your dead. It’s a tall pile this year, including crypto, SaaS, ARKK-style names, work from home, ecommerce, cable and media, even real estate and bonds. I’m contributing my own deluded bubble trade to the funeral pyre. I loaded up on warrants in a SPAC that never closed a deal. I’m embarrassed to even think about it now. I mentally quoted Soros, “When I see a bubble, I rush in to buy it,” and somehow believed there was a meme stock fortune waiting for me.

But it was just the same old mix of greed, hope, and delusion.

I mention the funeral pyre because we tend to obsess with learning from mistakes (Ray Dalio: “pain plus reflection equals progress.”) and miss that forgetting and letting go are equally important functions of the investment process.

“We learn by studying history and our own mistakes and actions. But if we hold on to our memories too tightly, we close ourselves off from the present. We view new situations through an aging and outdated prism. In your quest for knowledge and better understanding, don’t be afraid to forget.” The Market Has No Memory. Should We?

We must, after all, carry on. And the market outlook is about as clear as Klarman’s minestrone.

We’re constrained by limited time and attention. Should we spend our time trying to discern the chances of a Fed pivot?

“When investors think they see a path for central banks to ‘pivot’ toward ending the rate hikes and commencing rate cuts, investors need to jump in.

To this narrative, Elliott offers an emphatic: MAYBE.”

Thanks Paul, very helpful.

Or perhaps dig through the pile of discarded securities? In How to Invest, Sam Zell commented on his 1976 articled “The Grave Dancer” about buying out-of-favor and distressed assets:

“Yes, I wrote the article called “The Grave Dancer,” but what I was really trying to point out was that buying distressed assets requires you to walk very close to the graves, and that if you weren’t careful, the best of intentions could have you falling in.”

Careful on the other side of bubble mountain. The right question is not ‘how much is it down’ but ‘what is it worth in this new world?’

As Buffett commented in 2000, “You’ll see everything if you’re around markets for a reasonable period of time. It's extraordinary what happens.”

“We have seen companies sell for tens of billions that are worthless. We have seen perfectly decent things sell for 20% of what they were worth. … We saw a few businesses earlier this year with an equity evaluation of $10 billion where the business itself could not have borrowed, probably, a hundred million dollars in debt.

The business as a private business would not have been able to borrow a hundred million. But the owners of that business, because it’s public, can borrow many billions of dollars on their little pieces of paper, because they have this market valuation.”

If I may offer some thoughtful questions from a recent conversation with Berkshire’s Todd Combs:

“98% of what Buffett and Combs discuss is qualitative. ... The worst business grows and needs infinite capital with declining returns. The best business grows exponentially with no capital.”

“One question is constantly asked [at Berkshire], usually daily, and that is if the moat is wider or narrower on any of their businesses.”

“Combs recalled the first question Charlie Munger ever asked him was what percentage of S&P 500 businesses would be a “better business” in five years. Combs believed that it was less than 5% of S&P businesses, whereas Munger stated that it was less than 2%.”

“You can have a great business, doesn’t mean it will be better in five years. The rate of change is significant, making this exercise difficult.”

If you can find good answers to these, you’ll do fine in the long-run.

To paraphrase Buffett, the tide has gone out and a lot of nudity is being exposed. That doesn’t mean it’s a good use of time to sit on the beach and watch the spectacle.

In the game of compounding, the number one goal is stay in the game. So make sure your mind and body get proper recovery. Cultivate your resilience. Remember Soros: “When I don’t have to, I don’t work.” Integrate the lessons but absolve yourself from honest mistakes.

Because no matter how bad it could get, even Singer acknowledged that after getting something wrong the next step is to “shrug and try to make some money.”

Bring out your dead trades, your bad decisions, and set them on fire. Cleanse your palate. On we go.

Food for thought

“It’s just the nature of markets. They produce wild, wild things over time. The trick is, occasionally, to take advantage of one of those wild things and not to get carried away when other wild things happen.” Warren Buffett

Todd Combs and Michael Mauboussin

From the Graham & Dodd Annual Breakfast 2022 (my notes on Twitter).

“Combs said that it’s a red flag if a company is too focused on external relations.”

“A big signaling effect for Combs is when management changes the key performance indicators for which it will get compensated by, presumably because management won’t get compensated if the KPIs are left as is.”

“Every time Combs meets with a company, there are two questions he asks: (1) How long do you spend talking to investors (median response is 25% of time is spent talking to investors, and (2) what would you be doing if you were not publicly traded?”

“When looking at a company, Combs begins inside out versus outside in.

Combs explains there’s a lot of outside in. You hear a narrative, you meet with management, and it’s extremely intellectually dishonest. The goal of investing is to have intellectual purity. There’s facts and numbers, and then there is a narrative.

Combs tries to wall himself off from the narrative until he has a view. As mentioned before, Combs would start with delta reports. Put together your view without looking at the market cap. Limit the pollution. Then think about the future of the company and pressure test your assumptions.”

On the overlap between managing and investing:

Investment Framework: Michael Burry

Investment strategy one pager via Brandon Beylo (also check out Brandon’s terrific podcast).

Elliott Management: the quarter’s most bearish letter

I can’t tell if this was the real letter or a GPT3 prompt for 28 pages of maximum bearishness (leaked letter). Also important to remember that Singer has always been very bearish.

“Real bear markets (ones that feature 40% to 50% declines from the top) tend to crush a generation of speculators. That has not remotely happened yet.”

“Every period of financial market stress is unique. Knowledge or experience of past periods of market adversity adds to the richness of one’s ability to envision the range of possibilities and combinations of forces, but only in the broadest sense.

In our more than 45 years of trading, we have never been able to identify (in other than the most general terms) the pockets of risk that turn into quick-moving blowups.”

“The third and trickiest goal, especially challenging during adverse financial market periods, is to gauge, in the midst of rapidly shifting facts, trends, and financial and economic conditions, when it is the right time and at what price to add risk, in what magnitude and hedged in what way.”

“It would be “normal” to expect that the top-to-bottom fall in stock prices in the current bear market could be in the 50%-ish range, in line with the most severe bear markets of the post-Depression era.”

“We urge all investors (including ours) not to count on making a lot of money, because just avoiding losses will be tough. It is not possible to know how things will work out.

A hard landing in the global economy appears to us quite likely, and if this hard landing is a deep recession, a decline in the rate of inflation will probably accompany it. The probable policy response to the recession is likely to cause a new round of even-higher inflation.”

Buffett on oil in 2009:

Frederik, new to your Substack. Thank you for the time you give to crafting these insightful essays. I have a portfolio of investments, but I am not a market player. I do see a crash or a collapse coming. I see the financial as only one part. The one that I see as much more significant is the structural collapse of institutions. The millions of people who work in the administrative offices of large corporate and governmental businesses are going to find themselves, like employees at Twitter and Meta, out of work with no transferable job skills to a world where the centralized institutions are much smaller. I see as a relationship between Two Global Forces. One is the global force of centralized institutions of governance and finance. There is also the global force of decentralized networks of relationships. They are two trends passing in the night. The former having reached its apex will decline. The latter will grow until some thing like a digital collapse takes place. Ultimately, our global world will become more local. There will continue to be global institutions, but they will be much smaller, and, to surprise of only those at the top of those organizations, no one to take care of their daily needs. I think what is coming is unprecedented. This isn't the repeat of the 1920s and 30s. This is going to be something new and more ancient the end of the Roman Empire, the Mayan civilization or the Mesopotamia civilizations of the Fertile Crescent. What we have to our advantage is that we know what happened then, and we have a technical knowledge that no previous civilization had. We'll respond and adapt. Hard times will be with us. And a new world will begin to form as a result.

Did you get the title for this newsletter from Jon Stewart 's bullshit mountain?