Meshulam Riklis: The Dark Side of Graham & Dodd

“My mind worked 24 hours a day on how to go about acquiring companies and taking control of them.”

What happens if you take the value philosophy of Graham and Dodd and take it to 11? If you combine it with boundless ambition, aggression, and leverage? Private equity? Close. If you go further back in time, you get the story of Meshulam Riklis.

In the wake of WWII, Riklis arrived in the US as a penniless immigrant. He combined an instinct for deep value situations with a talent for convincing aging founders that he was the right person to sell to. A creative financier, he figured out a formula for “effective use of non-cash,” or using as much as leverage as he could to expand his empire. He did all of this long before Milken made junk bonds fashionable.

Riklis’s autobiography, $950 million in 40 Minutes, is a strange read from which I will quote frequently. Its title refers to his last big buyout in which he acquired the E-II portfolio of companies from American Brands in 1987. The deal was immediately contested by creditors including Michael Steinhardt and later Carl Icahn. Riklis proudly described the secrecy in which the transaction was pulled off, giving it more the flavor of a heist than a buyout. This marked the peak of his power, when he was listed by Forbes with an estimated net worth of $500 million. By then, he was married to an aspiring actress 30 years his junior whose name he had painted on one of his planes.

Shortly thereafter, his Russian doll of nested and highly leveraged companies collapsed, leaving creditors scrambling. What started as an imaginative value investor’s adventure turned into a nightmare of bankruptcies, related party transactions, lawsuits, and SEC investigations.

A big dream

Riklis was born in Istanbul in 1923 when his parents were moving from Russia to Palestine (then under British Mandate). He grew up in Tel Aviv and served in the British army during WWII. After the war, he moved to the US with his wife and their first child. After a brief stint in New Mexico, he ended up in Columbus, Ohio and attended Ohio State University.

There he was introduced to value investing with a professor’s task to “locate a trade company with a cash reserve that is greater than its worth on the stock exchange.” In his autobiography, Riklis reminisced how “the deal of my dreams began taking shape.” This was the dream of purchasing “a company by using the company’s own funds.”

He obsessively read biographies of business tycoons, “rugged and fearless men who knew how to think outside of the box and were driven by great motivation to make huge sums of money.” Their children however “didn’t want to produce cars, iron, or textile.” The following generation was looking to live the good life and for that, “they wanted to sell the empires their fathers had built.” Riklis pondered that a lack of successors would lead to companies being offered for sale. “I began to understand that their infuriating ingratitude was my opportunity.”

After graduating, he started teaching at the Talmud Torah School in Minneapolis. To earn more money, he joined brokerage firm Piper, Jaffray and Hopwood as a part-time junior analyst. It seems he quickly built a reputation for savvy analysis. But he had bigger dreams than picking stocks for the firm’s clients: “My mind worked 24 hours a day on how to go about acquiring companies and taking control of them.”

His first step was to gather a group of investors, including friends and clients of the firm. He looked for micro-cap stocks trading at deep discounts to their asset value. Year later, Riklis told the New York Times: “I concentrated on special situations. Typical special situations were companies with a big book value, companies bringing out new products or going into new fields, companies developing large earnings potential.”

His plan was to “get together a group of people who would invest their money in a small promising company, but a company where they could have some voice in management. If this worked out, then they could move on to another situation.”

His first idea was the Marion Power Shovel Company (talk about a stock that sounds like a value investment). He corralled a dozen investors and acquired stock from the estate of a large shareholder. However, when shares jumped 30 per cent, his group decided to take the profit and sold.

Riklis tried again in 1954 with a metalworking company called Balcrank. His group acquired 30 per cent for $300,000. Having doubled their money, the investors sold a year later.

Unlocking control

His first successful deal was the Gruen Watch Company of Cincinnati in 1954. An undervalued “sleeping beauty,” the company had valuable land and real estate in Switzerland which Riklis estimated could be sold for $5 million. He raised capital from his Minneapolis group as well as bank debt to become the largest shareholder.

Riklis didn’t contribute any of his own cash: “You invest the money. I’m investing thought, planning, and work.” For his efforts he would receive an annual salary, a fee, and the first $100,000 of profit earned by the group.

After buying into the company, he hired a new CEO. Riklis’s plan was to sell the Swiss real estate, re-focus the company in the US, and redeploy the cash in other undervalued assets. However, the new CEO soon objected to the sale of the plant and developed his own, growth-oriented strategy. When the board and investors backed him, a frustrated Riklis was forced to move on. “I was not yet enough of a glue to hold them together,” he said of his investor group.

Still, he had built a track record of successful deals and gained experience raising capital. “I raised it, me, Riklis, with an accent,” he told the Los Angeles Times in 1986. “A Hebrew-school teacher in Minneapolis, where I was the only Jew working for the firm.” (As quoted in the New York Times obituary)

In 1955, he started to look at small technology companies. He found Rapid Electrotype which produced components for typewriters and printing machines. The company had a $2.3 million market cap with $1.6 million in cash and $4.3 million in sales. It also had an elderly CEO.

Riklis studied the company, hoping to impress the man with his knowledge of “even the most esoteric details” of the business. Riklis kept meeting the CEO until the man grew to like the knowledgeable youngster and started to see him as a potential successor. In addition, Riklis arranged for other business leaders to provide positive references “which happened seemingly by chance.” Riklis recounted that when he finally acquired the CEO’s stake and became the company’s chairman, he was “31, had no money, no assets, no control in any company.” But now he had unlocked control of a balance sheet to use for further deals.

Turning the sleeping beauties into a Russian doll

After an unsuccessful attempt to gain control of typewriter manufacturer Smith Corona, Riklis was introduced to American Colortype. This was another company trading for half of its book value with cash, liquid assets, land, and inventory that Riklis could monetize. He bought blocks of shares with cash and debt, then merged the companies into Rapid-American.

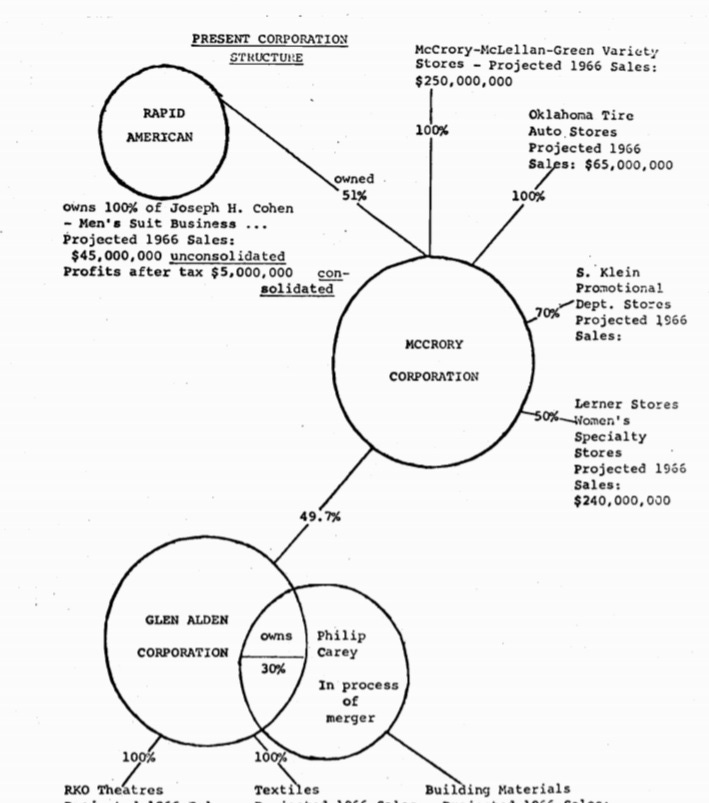

He had established his basic formula: acquire control of an undervalued company, preferably with debt, and proceed to use that company’s balance sheet for more deals. In an era before a deep junk bond market, he became an expert at finding creative ways to finance his deals through convertible debt, preferred stock, and other subordinated debt. His acquisition spree led him to companies in a variety of industries, including retail, auto parts, packaging, building materials, movie theaters, luxury goods, and spirits. His key acquisition was a chain of variety stores called McCrory with 850 locations and $300 million in sales.

“If you are a Rockefeller or a hotel owner, you build an empire based on the company's worth,'' he told BusinessWeek in 1974 when asked about his debt load. ''If you are Meshulam Riklis, you build an empire using every possible trick.”

The effective non-use of cash

In 1966, Riklis published a paper at Ohio State in which he outlined his takeover philosophy and included case studies of his various transactions.

“Financial management is perhaps the most potent factor in successful development of prosperous corporations in our time and offers a unique opportunity to capable aggressive businessmen to build large and strong industrial concerns from relatively modest beginnings.”

Undoubtedly, he was one such aggressive businessman building an empire from modest beginnings. He recounted his early journey: “I became intrigued to search for the ‘sleeping beauties’ since almost every day one could read somewhere about ‘undervalued situations.’ However, to invest was not what I had in mind – but rather to take a company out of its slump and build it into a company of strength.”

His formula reads like a blueprint for the private equity funds that would soon upend public markets.

The first key issue was to find motivated sellers: “I noticed many companies whose previously aggressive managements and owners had either passed away or grown old only to find the second generation incapable or unwilling to face the new challenges, thus allowing for a purchase of a controlling interest.”

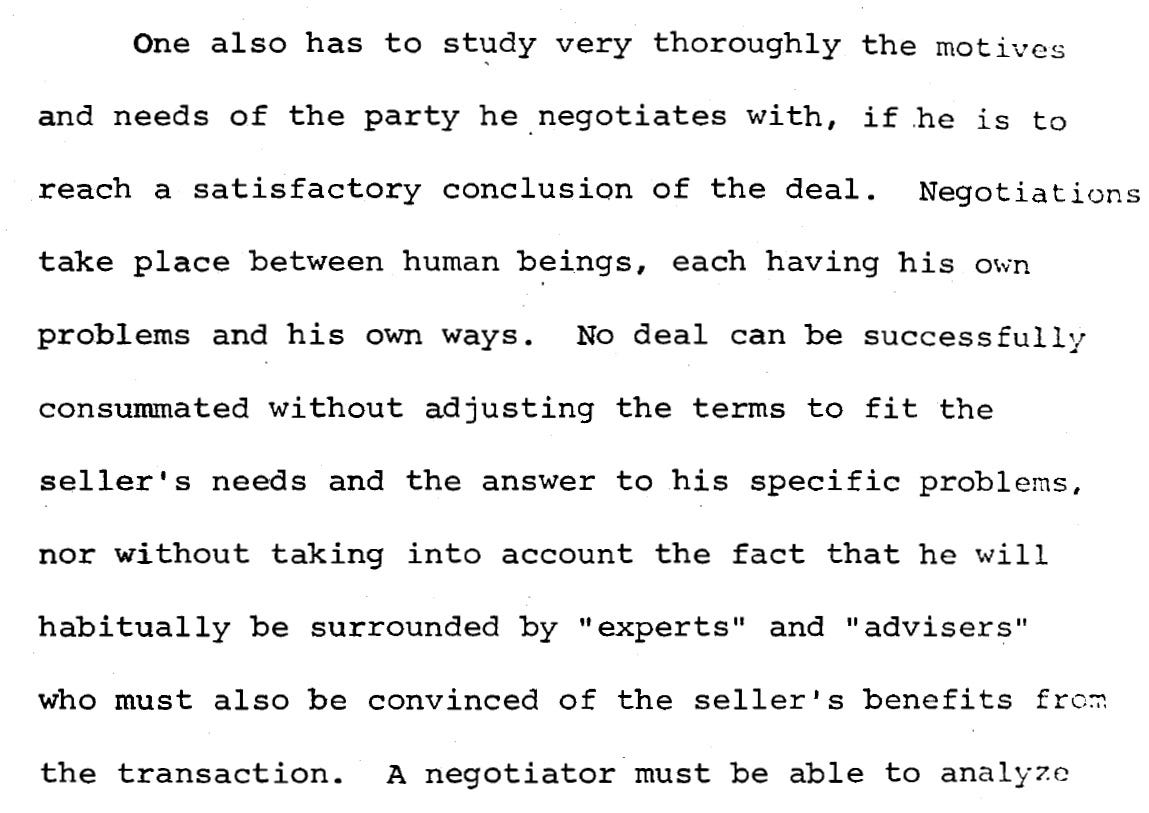

Riklis was keenly aware of the importance of understanding the individuals on the other side of the table.

The second key idea was to preserve cash and pay with “paper,” with debt, as much as possible. This he called the “effective use, or rather non-use, of cash,” and the “determining factor in the success of all subsequent deals.”

“Whenever possible, I called for an acquisition to be made without cash. If I had to pay cash, I projected the immediate generation of equivalent cash from the acquired company. Unless the above was possible, I preferred not to go ahead with the deal.”

“Capabilities in two arenas have played a predominant role in achieving the success as outlined herein: The ability to read the needs of the other party to the negotiations and know what will satisfy these needs and the constant effort to conclude the transactions without depletion of cash in the process.”

Courting sellers

Riklis became a master at convincing elderly founders to sell to him. He found ways to meet them through unofficial channels, spent months or even years courting them, and arranged for them to hear positive references. He preferred to source and create his own deals rather than compete in an auction process where he was unlikely to succeed with a bid which relied on leverage that was barely sustainable.

In 1968, he acquired Schenley International, one of the nation’s largest liquor distillers and distributors with $518 million in sales. Schenley was owned by Lewis Rosenstiel who was 75 by the time he finally sold. According to Riklis, Rosenstiel had declared that he would “probably never retire,” was considered “stubborn, bad-tempered and mysterious,” and had blown up prior merger deals. It took Riklis five years of relationship building during which Rosenstiel hired investigators to ensure Riklis wasn’t working for his competitors, the Canadian Bronfmans. As part of the deal Riklis also agreed to personally buy Rosenstiel’s six-story Manhattan townhouse.

“To make a deal with Lew Rosenstiel,” Riklis said, “you had to sit down and listen to his crap and smother him with love and affection and cajole him and laugh at his jokes and get used to all the stories. When he calls you to come to Florida, you get on a plane and come to Florida, and normal businessmen don’t do these things. They feel that a transaction is worth a certain price and that’s it. That’s not the way deals were made in those days. You had to be a real lover.” (LA Times, 1986. A Borrowed Empire)

“What was crucial to Abe List and Rosenstiel was the question of who would be the inheritor and successor of their life’s work. For each, the company was the epitome of their creativity, an inseparable art of them.”

Buying time

As Riklis grew his empire and managed his way through crises and restructurings in 1963 and the early 70s, it became clear that one didn’t want to be on the receiving end of this paper.

“I made my famous statement that I don’t do business unless I can give ‘Russian rubles’ or ‘Castro pesos.’ In other words, you give paper,” Riklis recalled. “And the SEC called my lawyers and said, ‘Will you keep Riklis’ big mouth shut?’” (LA Times 1986, A Borrowed Empire)

“You must understand a basic principle: I have 20 years to pay it. In 20 years, the rabbi and the dog will be able to converse,” he said. He was referring to a Jewish parable in which a rabbi is ordered to teach the local landowner’s dog to talk. The rabbi agrees but says it will take 20 years (there seem to be numerous versions of this parable and the number of years differ). People in his community call the rabbi crazy but he responds: “Well, in 20 years, who knows? Maybe the landowner will die, maybe the dog will die ... or maybe the dog will learn to talk.” Every dollar paid as debt rather than cash bought Riklis more time and optionality to do more deals. (LA Times, 1986, A Borrowed Empire)

The nested structure of his companies was treacherous. In 1963, retail chain McCrory reported profits that were half of what had been forecast and its stock was cut in half. This impacted the balance sheet of Rapid-American which owned the McCrory stock. Rapid-American stock fell from a high $37 to $4. Riklis sold off most of Rapid-American’s business units to avoid bankruptcy. “You must remember,” he told the LA Times, “I was the financial wizard rather than the company’s operating guy.”

If Riklis had used his formula to buy strong companies at a conservative pace, I wonder what he could have achieved. Instead, he acquired a basket of mostly cyclical companies. Every time he recovered from a near-death experience, he immediately went back to acquiring assets at breakneck speed.

Jumping the shark

“From 1970 to 1973, I went berserk. I did not have a good marriage. I wanted some action. I invested money in all this crap. Real estate in Italy. A company in Germany; they ended up with a $20-million loss. That’s how my fortune was dissipated.” He acquired Kenton Corp., the owner of Cartier, Mark Cross and Valentino, “because if you go out with girls, it’s very impressive.”

In control of a sprawling empire, Riklis lived lavishly. He had a fleet of “five planes and two helicopters” and bought the Riviera hotel and casino in Las Vegas, gaining an appetite for glamour and nightlife.

A strange and uncomfortable part of this autobiography are the sections devoted to his sexual escapades and “15 paramours,” his girlfriends whose livelihoods he paid for (perhaps what would be called sugar babies today). Some sections are downright disturbing, such as when he described “buying up businesses that could supply me with young beauties. That was why I decided to gain possession of casino, hotel, and nightclub businesses, along with women’s high fashion brands, jewelry and diamonds.” He mentioned a “former stockbroker” turned talent agent who “tracked down girls who dreamed of becoming actresses” and became “an endless resource for lustful parties and wild nights.”

What Riklis called “an insatiable ego trip” culminated in the marriage to an aspiring young actress named Pia Zadora in 1977. He was 53, she was 24. Riklis got involved in her career, financed the production of movies, had her name painted on one of his planes, and bought and razed the massive Pickfair home in Beverly Hills.

When the boom of the 1980s ended, Riklis’s empire and second marriage disintegrated (Zadora kept the mansion and sold it in 2005 for more than $17 million).

Heist money

“Riklis has gutted so many companies over the years that I call him Freddy Krueger, the Bondholder's Nightmare on Wall Street,” financial columnist Allan Sloan wrote in 1992. “He is famous for laughing at the bondholders and lenders he victimized.” (quoted in the New York Times obituary)

One of Riklis’s last big transactions was the acquisition of E-II. In 1986, private equity firm KKR and executive Donald Kelly acquired the Beatrice Foods conglomerate which previously had acquired another conglomerate named Esmark, whose CEO Kelly had been. While dismantling Beatrice, some assets were contributed into a new company, E-II or Esmark II, that was to serve as Kelly’s second act (I wrote about Beatrice in my profile of Reginald Lewis).

Kelly then tried to buy American Brands, formerly American Tobacco. Instead, American Brands acquired his E-II in a “Pac-Man defense.” Looking for a way to lower their debt load, the new owners struck a deal with Riklis. For $950 million in cash, $250 million preferred stock, and the assumption of $1.5 billion in subordinated debt, Riklis took over the E-II assets. This portfolio of nine companies included luggage maker Samsonite, a maker of water softeners, and producers of flavorings, frozen foods, snacks, and pet food.

Riklis remembered: “We had to keep everything top secret, as there was real anxiety that others might suddenly get a similar idea.” He noted dissenters to the deal who “claimed that the deal would furnish me with a gift worth hundreds of millions of dollars, and they were right.” It was his final “treasure cave.” Except it was not a deeply undervalued company.

The market’s verdict on being a creditor to Riklis was clear: E-II’s bonds traded down from 110 per cent of par at their peak to 80 percent when the deal was announced. Michael Steinhardt, one of the debtholders, unsuccessfully sued to prevent the transaction.

What had started as a journey to find and acquire undervalued assets ended with abusing control for personal enrichment. According to BusinessWeek, in 1989, Riklis had E-II buy a money-losing retail chain from his other company McCrory. Six months later, the chain was shut down and E-II was left with a $221 million loss. Money was siphoned out of the company through other related party transactions and fees until Carl Icahn successfully removed Riklis and eventually pushed E-II into bankruptcy.

Conclusion

Stories from the worlds of business and finance sometimes resemble Necker Cubes, optical illusions revealing different shapes depending on where you focus. Riklis started out following a traditional value philosophy, except that he focused on control deals. He built his nested conglomerate without an Ivy League background or network and long before private equity and junk bonds became fashionable.

But once in control, he increasingly acted for his own benefit, treating creditors as the suckers at the table. He acquired companies that barely made it through recessions and used them to finance an extravagant lifestyle.

I kept wondering if he could have stopped, if there was a point where he could have liquidated his holdings and retired from the game. But such is not the mindset of one who bootstraps their way to the top through sheer ambition (or greed), grit, and ingenuity.

In the end, Riklis even owed Donald Trump rent for his suite at Trump Tower. Battered with lawsuits and discredited by a string of bankruptcies, his arc was complete.

Rapid-American, his original holding company, filed for bankruptcy in 2013 due to asbestos liabilities of a company acquired in 1974. Riklis passed away in 2015. In the end, he was known as much for his marriage to Zadora as for his financial exploits.

His story is a reminder of both the creative power and the destructive force of ego. And a cautionary tale to be mindful of a CEO’s character. If they treat you like the landowner who waits 20 years to see if the dog will speak, run for the hills.

making it a habit to re-read your posts. this piece is underrated

My favourite article. Thank you for both the finance and moral lesson. :) I am sending it to everyone in my finance class. I read the biography while it was on Apple Books and they removed it :/ so you have a monopoly on Riklis lore.