Magic Words in the World of Magic Money

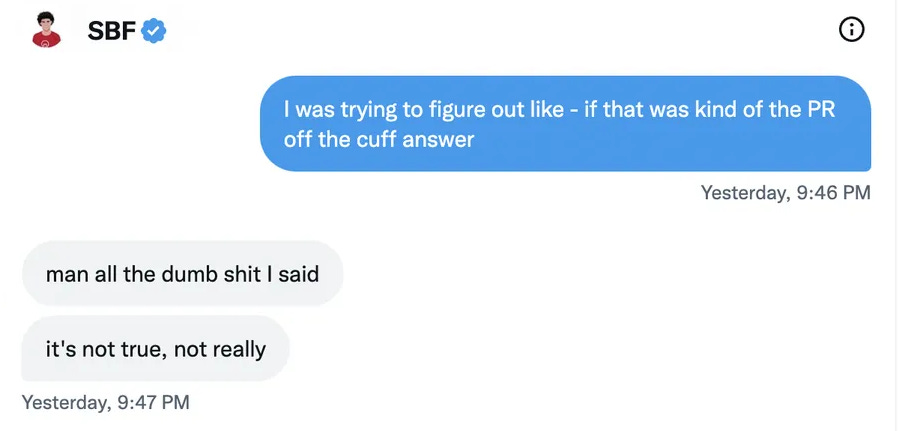

"man all the dumb shit I said; it's not true, not really" Sam Bankman Fried

Hi everyone,

I hope you all had a terrific week. A friend of mine invited me to a beautiful Friendsgiving and I felt very grateful to have community far away from family. It reminded me of a Buffett and Munger quote (everything does these days). In 2003, they were asked about their definition of success in life:

When you get to be my age, you will be successful if the people that you would hope to have love you, do love you. Charlie and I have talked a lot of times. If we could just buy a million dollars’ worth of love, it would be so much more satisfactory than to try and be lovable. But it doesn’t work that way. The only way to be loved is to be lovable.

Something worth keeping in mind when writing about money.

There is nobody I know that has the love of people around them, people they work with, their family, and their neighbors— that feels other than a success. Look at people older than you are. You will not see an unhappy person who is loved by those around them.

Buffett doesn’t criticize by name but he’s not shy to point out that plenty of people lose their way in the pursuit of wealth.

Charlie and I know a few people that have a lot of money. They get their names on buildings. And the truth is nobody loves them. Not their family, not the people who name the buildings after them. It’s sad. It’s something you can’t buy. The nice thing is that you always get back more than you give. And if you don’t give any, you don’t get any. It’s very simple.

To which Munger added a zinger: “You don’t want to be like the motion picture executive in California. They said the funeral was so large because everybody wanted to make sure he was dead. There’s a similar story about the minister saying at the funeral, ‘Won’t anybody stand up and say a good word for the deceased?” And there was this long silence. Finally one guy stood up and he said, “Well,” he said, “his brother was worse.’”

Speaking of names and buildings, I continue to be bewildered by the saga of Sam Bankman-Fried and FTX (which had sponsored Miami’s arena). The next Warren Buffett curse remains undefeated. But what are the lessons?

Coverage by major news outlets remains weirdly benevolent. Billions of dollars of customer deposits were moved from the exchange to the hedge fund where they disappeared (lost? stolen?). And yet SBF is still inextricably linked to his philanthropic aims.

I think the effective altruism angle broke some people’s brains. Here is a profile of philosopher William MacAskill, one of the pioneers of the movement.

MacAskill limits his personal budget to about twenty-six thousand pounds a year, and gives everything else away. He lives with two roommates in a stolid row house in an area of south Oxford bereft, he warned me, of even a good coffee shop.

Fair enough. That’s a virtuous life.

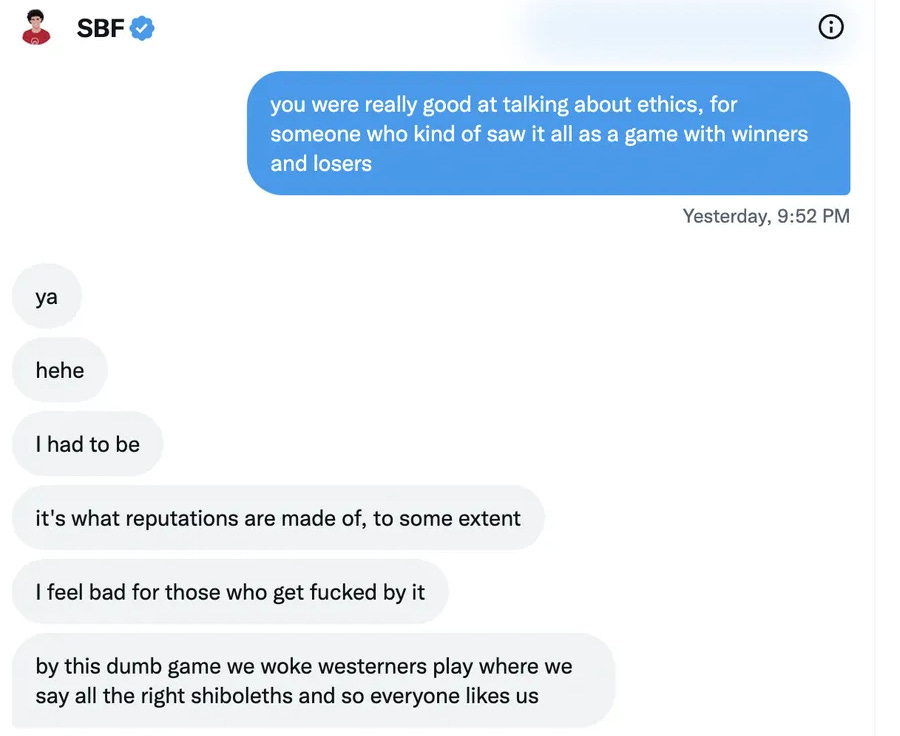

SBF subscribed to one of the ideas of effective altruism, “earning-to-give”, and took it to another level. Maximize wealth now to maximize impact later. He did this by first being a trader, then by running a hedge fund, and, finally, by creating a casino (I mean, crypto exchange).

In all cases he extracted capital from markets. He moved money from less skillful (or lucky) players to himself. Nothing wrong with that. But it’s strange that people considered this to be commendable. We know nothing about the values or intentions of the people who lost the money.

All we know, all we need to know, is that the person aggregating the money could cut big checks and buy political influence. Which gets me to a Munger on fraud in asbestos claims:

Once you get wrongdoers rich, they get enormous political power to prevent change in the laws that are enriching them. It means that we should all be more vigilant about stepping on these wrongs when they’re small. When they get large, they’re very hard to stop.

I have no issue with him building a seemingly useless marketplace. It’s part of what we do as a society. But it’s not a net positive for the world, even if it had been a legitimate operation.

That was one lesson of the past few weeks. A major crypto exchange goes up in flames and unless you were a customer, investor, or otherwise involved in the crypto ecosystem, it didn’t have an impact. There was no ripple effect outside the world of crypto. Just a lot of noise and justified outrage. Still a technology looking for a use case beyond gambling (and perhaps store of value in the case of something like Bitcoin, tbd). If on the other hand Twitter had shut down even for a few hours or days…

Nothing of lasting value was created and yet SBF achieved sainthood because all the clothes he owned fit in his backpack.

Well, after reading his insane interview with Vox’s Kelsey Piper, one has to conclude that even if SBF believed in effective altruism early on, he came to view it as a tool. A nerdy open sesame. Magic words that opened doors to capital and made him invulnerable to criticism. He became a living manifestation of the post truth world.

And sure enough, the man whose clothing fit in his backpack appreciated having a jet and some fancy living quarters for himself, his executives, and even his parents (and apparently loads of Jimmy Buffett margaritas).

In Why Are There So Many Cheaters These Days? Ben Carlson decries that we “celebrate [hucksters and charlatans] with books, documentaries, podcasts, movies and streaming mini-series where A-list celebrities portray these fraudsters.” He’s right. Streaming companies are already fighting for the rights of Michael Lewis’s book on this.

I don’t condone the behavior but I also get why so many type-A young people are opting to cheat.

If their scheme works out they walk away with millions or even billions of dollars.

If it doesn’t work out they become famous (or infamous) in the process and cash in on their story.

I just find it gross that we’ve decided to put these fraudsters, charlatans and jerks on a pedestal.

In other words: we collectively get the SBF’s we deserve.

How did FTX’s sophisticated investors end up with so much egg on their faces? Was it all just an episode of severe FOMO and social proof of following other high profile investors?

In The Hacker's Guide to Investors Paul Graham of Y Combinator wrote that “most investors are ‘bottoms’ in the sense that the startups they like most are those that are rough with them.” (hat tip to Jason)

When Google stuck Kleiner and Sequoia with a $75 million pre-money valuation, their reaction was probably "Ouch! That feels so good." And they were right, weren't they? That deal probably made them more than any other they've done.

In The Power Law, Sebastian Mallaby described the meeting between a young Mark Zuckerberg and Sequoia.

Zuckerberg and his buddy Andrew McCollum appeared at the Sequoia headquarters. They were not merely late. They were dressed in pajama bottoms and T-shirts. … The pajamas were a provocation, a challenge.

Zuckerberg had risen, washed, and then decided to dress up in pajamas and show up insolently late. A deliberate snub was worse than an unintended one.

Mallaby called the moment “a watershed for venture capital.” The balance of power had shifted from venture capital to founders. Not only could the best founders pick who to partner with, countersignaling became the norm. SBF played video games while pitching Sequoia. The lack of respect made him more attractive, not less.

“I sit ten feet from him, and I walked over, thinking, Oh, shit, that was really good,” remembers Arora. “And it turns out that that fucker was playing League of Legends through the entire meeting.”

“We were incredibly impressed,” Bailhe says. “It was one of those your-hair-is-blown-back type of meetings.”

Whoever we’re looking for — the next Warren Buffett, Steve Jobs, Mark Zuckerberg — we won’t find them by looking for people eating McDonald’s for breakfast, wearing black turtlenecks, or negging us in meetings.

In How VCs can avoid being tricked by obvious frauds Rohit Krishnan calls FTX Dumb Enron, “where someone ‘trust me bro’-ed their way to a $32 Billion valuation.” Krishnan doesn’t blame VCs for not doing enough financial due diligence. But he correctly points out that a lot of basic questions were not asked.

What they should have known however are the basic red flags - does this $25 Billion company, going on a trillion by all accounts, have an actual accountant? Is there an actual management team in place? Do they have, like, a back office? Do they know how many employees they have? Do they engage professional services like lawyers to figure out how to construct the corporate structure maze? Do they routinely lend hundreds of millions of dollars to the CEO?

… The problems were barely skin deep. The gotcha questions here were of the grade-school variety, like “who holds most FTT coins?” or “what the hell is Serum?”. This isn’t a failure of forensic accounting, this is a failure of basic logic. Buying everyone $300 million of mansions in the Bahamas doesn’t sound like things hidden under the radar.

I think he’s both right and that it doesn’t matter. These are lessons investors collectively relearn every cycle. Ben Hunt explains why in The MacGuffin, Part 2: The Story Arc of SBF and FTX. Ben dissects the maze of entities and flows of capital.

Once upon a time, Sam Bankman-Fried found a Magical Money Machine he called Alameda Research. Or at least he thought he had found a Magical Money Machine.

I’ve known that feeling (briefly!), and it’s the best feeling in the world if that’s your life’s MacGuffin, as I suspect it is with SBF. Not for the money itself, mind you, but for what you can DO with it. And not even for what you can do with it, but just for knowing that YOU solved the biggest puzzle in the world.

Ben believes that when the Magical Money Machine Alameda stopped working, SBF went looking for a replacement. Alameda turned into a ponzi scheme sucking capital out of FTX. It’s a great piece, go read it.

Compare Alameda’s pitch deck promising 15% with no downside to Francois Rochon who recently gave a wonderful interview to William Green. Rochon looks for great companies that grow — but not too quickly. Companies with a track record — but not too old. Not too small, not too big. Not too high of a multiple — but they don’t have to be bargains either. All put together in a portfolio that’s neither extremely concentrated nor very diversified.

It’s boring by design. And it worked. Rochon’s Giverny has compounded at 15%+ since inception in 1993. But not by promising no downside. That’s the kind of return that looks like magic in retrospect. And it exists in no small part because most investors don’t have the patience for it. As George Goodman wrote in The Money Game, people want the excitement of the game. “It doesn’t make sense, or the kind of sense you expect, but it makes a nutty kind of sense if you see it for the way it is.”

They want to outsmart the market and their peers. They want to believe the Magical Money Machine is out there waiting to be discovered. Ben called it “the best feeling in the world.” And who wouldn’t want to chase that feeling.

That’s how institutional investors, smart but saddled with record amounts of money to deploy, find themselves in what looks like a massive case of affinity fraud.

SBF got away with it because everyone knew that everyone knew that Sam Bankman-Fried was a Boy Genius who had discovered a Magical Money Machine and was intent on doing a certain kind of Democratic-leaning, woke-ish Good in the World with his riches. It was common knowledge.

FTX won’t be the last time investors meet someone with a seemingly magical solution saying all the right words. In 2002, Buffett and Munger discussed fraud in insurance and Munger quipped about what kind of person would take Berkshire for a ride.

I’ve always said that the guy who takes us is going to have a modest little office and a modest demeanor and —

Buffett: He’ll carry around Ben Franklin’s autobiography, I can —

Munger: The kind of people who defraud us are not going to be the kind of people who are defrauding everybody else.

Remember that the person most likely to defraud you will be saying your magic words, whatever they are. It can be difficult to imagine that some people believe in nothing. That those words, to which you attribute great meaning, can mean nothing to them. But a big part of investing is to study people and to see them clearly. Even if it’s unpleasant or contrarian. Especially when it’s unpleasant or contrarian.

Food for thought.

Subscribers can find the regular collection of links and readings below.