George Soros's Layers of Conviction

"That doesn’t make sense!" "What do you mean?" "Go for the jugular!"

"I've learned many things from [George Soros], but perhaps the most significant is that it's not whether you're right or wrong, but how much money you make when you're right and how much you lose when you're wrong.” -Stanley Druckenmiller

“When I’ve looked at all the investors (that) have very large reputations — Warren Buffett, Carl Icahn, George Soros — they all only have one thing in common. And it’s the exact opposite of what they teach in a business school. It is to make large, concentrated bets where they have a lot of conviction. They’re not buying 35 or 40 names and diversifying. … [In 1992] when I went in to tell Soros that I was going to short 100 per cent of the fund in the British pound against the Deutschmark, he looked at me with great disdain. He thought the story was good enough that I should be doing 200 per cent, because it was sort of a once-in-a-generation opportunity.” -Stanley Druckenmiller, The Hustle

George Soros is famous for “breaking the Bank of England,” for making a cool $1 billion when the pound was devalued in 1992. It’s a famous trade that pitted markets and speculators against the European political establishment. The sheer scale and audacity cemented Soros’s reputation even though Stanley Druckenmiller was the portfolio manager at the time. It’s a case study whose nuances are easy to miss.

There are a couple of obvious issues with taking Druckenmiller’s statement about concentrated bets as advice. There is survivorship bias (though as Gavin Baker pointed out, surviving is kind of the point). And he is Stanley Druckenmiller and you are you (think about your investor Ikigai).

“What is most interesting to me about the breaking of the pound was the combination of Druckenmiller’s gamesmanship – Stan really understands risk/rewards — and George’s ability to size trades. Make no mistake about it, shorting the pound was Druckenmiller’s idea. Soros’s contribution was pushing him to take a gigantic position.” Scott Bessent, Inside the House of Money

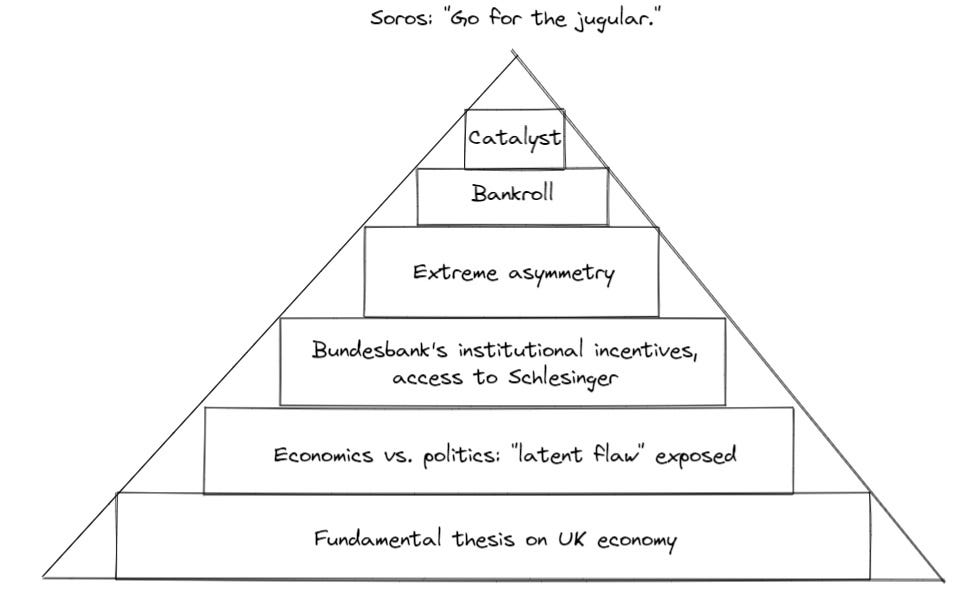

Soros and Druckenmiller weren’t the only ones betting against the pound. This was not a case of variant perception. Bank prop trading desks and macro traders like Bruce Kovner and Paul Tudor Jones were betting on the same outcome. But none had the same scale or conviction. When Druckenmiller told The Hustle that Soros “thought the story was good enough,” he didn’t capture the multiple dimensions of conviction that aligned to form the foundation of a generational trade.

What gave Soros the conviction to push Druckenmiller to lever up and bet the farm? Without understanding the conditions of the trade, any lessons are likely to get lost in translation.

It all started with fundamental research

Finding asymmetry

A behavioral perspective

Size mattered

The levee breaks

Conclusion