Kai Wu of Sparkline Capital: Tackling Difficult Questions With Unstructured Data

Kai Wu of Sparkline Capital: Tackling Difficult Questions With Unstructured Data

"While independence comes at a cost, it frees one up to pursue new lines of inquiry. The greatest ideas often stem from meandering research that connects the dots across many disparate areas."

Much ink has been spilled on the recent struggles of value investing and in particular on the underperformance of the value factor (expressed through ratios such as price-to-book and price-earnings). Wealthfront recently abandoned the value factor “as research suggests it is no longer as effective as it once was” while others vigorously defend it. One reason undoubtedly is accounting which, as Michael Mauboussin pointed out, “has not kept up” with the rising importance of intangible assets. “There is a good argument to be made that the ineffectiveness of the value factor is in part because of its diminished ability to reflect economic reality.” The solution to this issue remains unclear. How does one apply the ideas of value investing systematically in this new world?

One of my favorite researchers and writers about this question is Kai Wu of Sparkline Capital. Kai spent five years at GMO and co-founded a hedge fund before devoting himself to tackling difficult questions, such quantitative value investing in the 21st century or discerning the value of a company’s culture, through unstructured data.

“Investors have not adapted their tools as the economy has evolved from industrial to intangible. Intangible assets are the primary drivers of corporate cash flow, yet are largely ignored in standard accounting and valuation practices.” Kai Wu, Searching for Superstars

After two years of research, Kai was finally confident that the value factor could be fixed by creating a composite measure for intangible value a derive a new estimate of intrinsic value.

The following is my take on his research around value and culture as well as a Q&A with Kai about his work.

Disclaimer: I write for entertainment purposes only. This is not investment advice. Seek your own financial, tax, and legal advice before making any investment decisions. Do your own work! I am are not your fiduciary or advisor.

💡You could be sponsoring posts like this one if you’re looking to reach 8,000+ thoughtful subscribers and many more readers on Twitter.😏

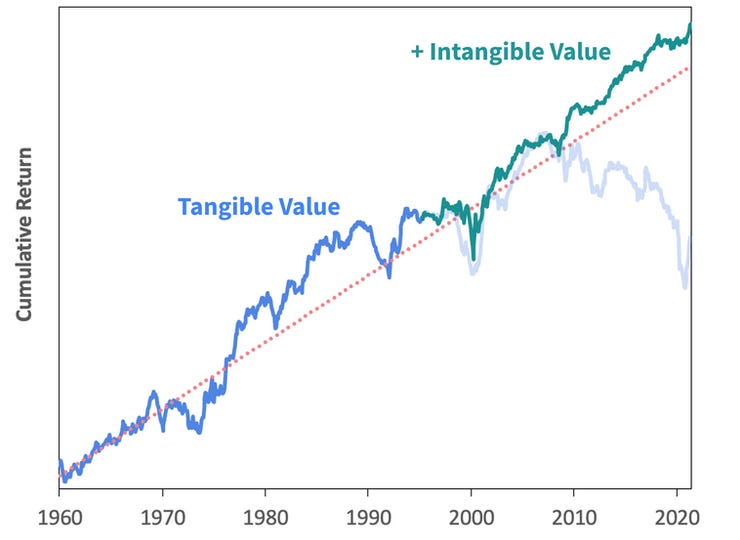

The quest for intangible value

Much of Kai’s work rests on the belief that too much capital has been chasing signals in structured data such as price and volume, financial statements, analyst estimates, and macroeconomic data. “Not surprisingly,” Kai writes, “we have witnessed standard quantitative factors, such as value and momentum, struggle in recent years.”

In addition, the rise of intangible assets seems to slowly devalue traditional financial information for an increasing number of companies:

“The constant rise in the importance of intangibles in companies’ performance and value creation, yet suppressed by accounting and reporting practices, renders financial information increasingly irrelevant.” Baruch Lev and Feng Gu, The End of Accounting

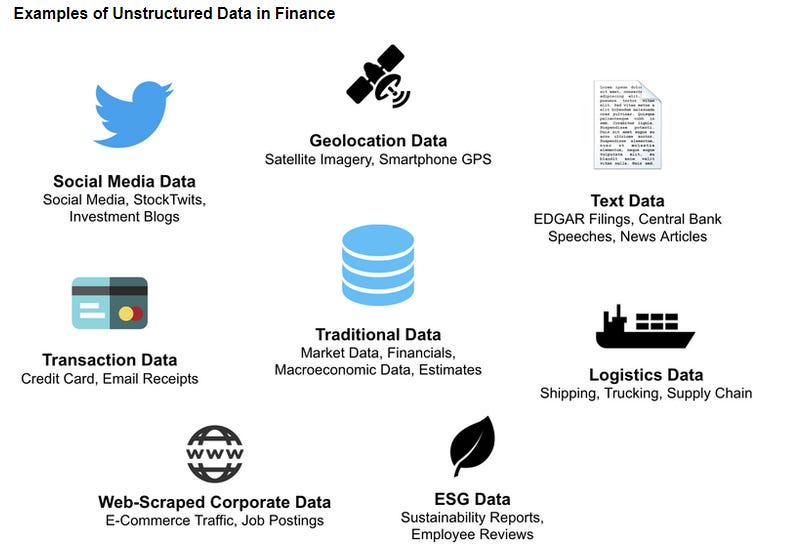

Instead, Kai focuses on unstructured data – everything from text in SEC filings, earnings calls, Twitter, LinkedIn, Glassdoor, even patents. “Given that the quantitative community is still extremely focused on linear models,” he writes “there is a significant advantage to be gained by using machine learning models.”

“As investors, our goal is to explain the economy, but structured data provides only a very incomplete picture. Ultimately, we have no choice but to rely increasingly on machines to help us process the exponentially growing volume of data,” Kai writes in Investment Management in the Machine Learning Age, one of two foundational pieces on his research process.

In the other piece, Deep Learning in Investing: Opportunity in Unstructured Data, Kai lays out his process for using natural language processing to extract signals from text such as earnings transcripts. For example, machine learning models can be pre-trained on large language data sets, such as websites and user reviews, and allow the researcher to detect sentiment categories in earnings commentary.

“Given that these innovations are less than a few years old, we believe there is opportunity for entrepreneurial individuals and firms to profit from the impending transformation.”

Anyone familiar with the buzzword bingo that can appear in earnings releases and on calls knows that management teams are aware that their language is being parsed for keywords. Thus, for Kai this was merely the start of his learning journey.

One can trace the evolution of his work through his research papers, starting with an evaluation of how value investing has been structurally short disruption. Kai assigned companies “disruption scores” based on an assessment of SEC filings and patents. “Once we neutralize its anti-disruption bet,” he wrote “we find that value’s lost decade disappears.”

Kai then took deep dives into different forces shaping the economy today: from rising industry concentration (that piece is full of excellent industry consolidation charts) to the rise of the intangible economy and the emergence of platform companies with strong network effects. He even found a way to tackle human capital by assessing companies’ ability to attract graduates from top universities and searched for “hidden tech companies” by canvassing the workforce for PhDs and software developers. It’s that kind of quantitative yet investigative work on original questions that blew my mind.

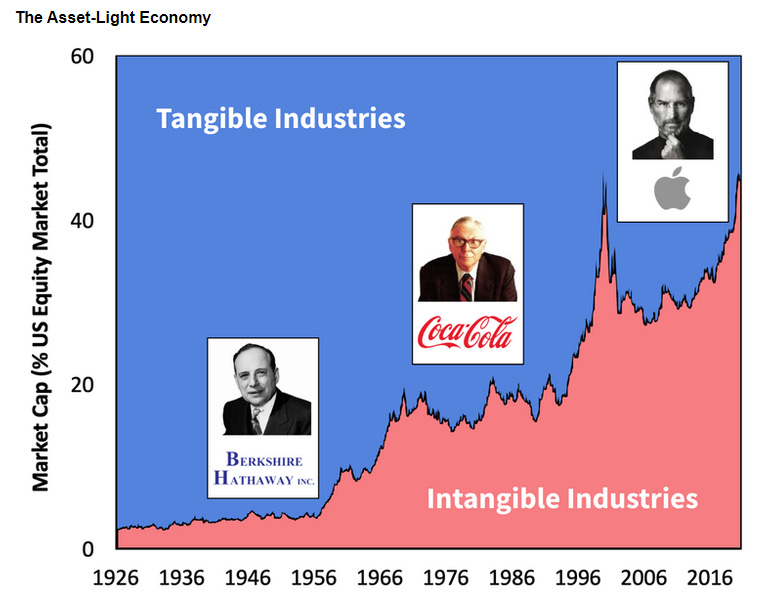

Kai built a portfolio of factors surrounding intellectual property, human capital, brand equity, and network effects which he integrated into a new valuation framework with “a single cohesive measure of firm-level intangible value.”

If you read only one of his papers, Intangible Value is the one I’d recommend. It integrates his prior research and can spark new ideas and questions even if you have no further interest in quantitative investing.

He picked Buffett’s own evolution as an investor as an example of moving from tangible assets to brands and, finally, network effects:

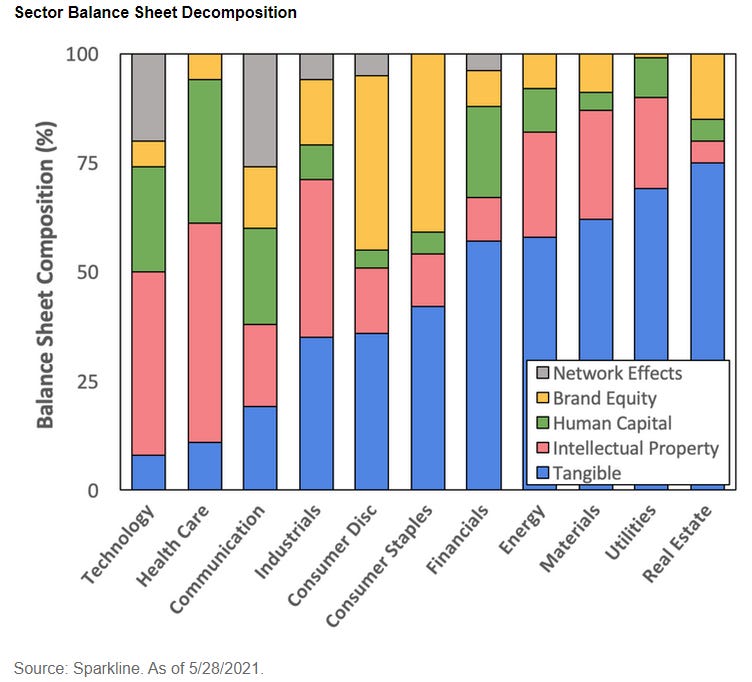

The composition of his intrinsic value across sectors is intuitive and fascinating:

Kai launched an actively managed ETF based on his factors and metrics such as R&D spend, PhDs, patents, and the “disruptiveness” score (obviously not investment advice!).

Culture

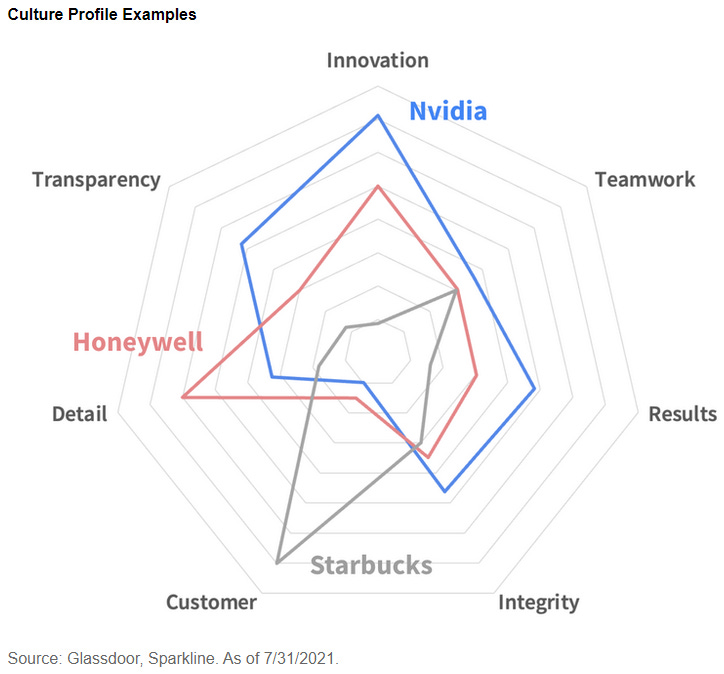

Kai published another thought-provoking paper on a topic that is on my mind: culture, which he called the “ultimate intangible asset.” He created “company culture profiles” and used Glassdoor employee reviews to score companies on seven dimensions of culture (innovation, teamwork, results-orientation, integrity, customer-orientation, detail-orientation, and transparency).

“Nvidia focuses on innovation, Honeywell excels at details, and Starbucks cares about the customer. Given the nature of their respective businesses, this makes sense.”

Interestingly, he found that merely having a strong and distinctive culture seems to be valuable, musing that “perhaps cultural uniqueness is itself an intangible moat.” Unfortunately, it’s not that simple as the causality could be reversed if “only leaders who are already successful ‘earn the right’ to be culturally idiosyncratic.”

“In any case, investors should pay special attention to firms with strong cultures.”

Perhaps unsurprisingly, he found that companies scoring high on innovativeness outperformed generally, they won “not only in the technology sector, but in many other industries.” High employee satisfaction was also valuable whereas toxic culture detracted from performance. Other cultural factors seem to be more contextual. A culture of stability was valuable in “procedural” but not in “creative” industries.

I really recommend the paper because I used to think about culture as something that had to be evaluated bottom-up by the analyst (and firms like WCM made it integral to their investment philosophy). And yet it was never quite clear to me what the analyst should look for. There is no uniform “great culture” and what matters differs across industries. Even within an industry, successful cultures can look very different (I compared the collaborative culture of Atlassian to the performance culture of Snowflake). Perhaps the answer lies in a combination of quantitative and qualitative work. Research such as this paper can give the analyst pointers on what to look for during a deep dive.

Q&A with Kai Wu

Q: What drove you to set up your own firm and do this research on your own? What makes this so interesting or important to you?

The ability to conduct independent research is very important to me. While the investment industry attracts extremely smart and hard-working people, it is paradoxically not all that innovative. Unfortunately, large investment managers often face a classic innovator’s dilemma due to the myriad handcuffs of organizational constraints and institutional client demands.

While independence comes at a large cost, it ultimately frees one up to freely pursue new lines of inquiry with far fewer constraints. The greatest ideas often stem from meandering research that connects the dots across many disparate areas. This research is often “blue sky” or involves taking contrarian positions. We believe that being an independent boutique helps ensure we can take the intellectual risks required for innovation.

Q: What questions interest you most? How do you decide what to research next?

I focus on research topics that meet two criteria. First, they need to be big problems that many people care about. We have done a lot of work on how to modernize value investing, which is a strategy followed by trillions of dollars of capital. Similarly, our most recent paper provides a framework for investing in crypto. Given the great potential of Web3, this is a question on many investors' minds.

Second, I will only tackle problems if I think I can offer unique insights. My analysis tends to be extremely data-intensive and often relies on machine learning and natural language processing. Thus, I tend to stick to topics that lend themselves to this data-driven approach. Fortunately, with the exponential growth of data, an increasingly dominant share of questions are now addressable using these techniques.

Q: Why is unstructured data so important in your work and what are its limitations?

Structured data constitutes less than 20% of all outstanding data. Furthermore, in finance it mainly consists of traditional market and accounting data that has been picked over by academics and quants for many decades. If the important research questions could have been answered with this data, they would have been solved by now.

In contrast, unstructured data has really only become “unlocked” in the past several years. The data are large, high-dimensional, and messy. One cannot read a patent abstract with a linear regression. Fortunately, advances in natural language processing and computing allow us to tame this unstructured data. Unstructured data can be extremely valuable, giving us insight into firms’ human capital, culture, and brand perception (among other things).

We believe that unstructured data will see much greater adoption by the investment industry in the next decade. Its main current limitation is that it is much harder to work with. However, this bottleneck will be gradually resolved as more data scientists are trained and machine learning tools are made more accessible to the masses.

Q: How do you determine which data sources to use in your research?

As mentioned, data is huge and growing at a dizzying rate. Rather than randomly walk through this data, we start with a fundamental investment thesis – that intangible assets drive value creation but are underappreciated by the market. From first principles, we can derive the four pillars of intangible value: intellectual property, brand equity, human capital, and network effects.

From here, we search for data sources that might help us quantify each pillar. These data vary widely across pillars. For example, job postings help us measure human capital but patents are more useful for IP. The key is that we do not use the “brute force” approach employed by some quant investors. We have found that throwing massive datasets into a deep neutral net leads to extreme overfitting. We try to be quite thoughtful in first narrowing down our search space.

Q: There is evidence that traditional quantitative factors have decayed as more capital is deployed to exploit them. How do you think about the risk of competition catching up to the new factors you’re identifying and staying ahead on innovation as a small firm?

First of all, we agree with this point around alpha decay. The capital cycle operates across firms and industries, so why wouldn’t it also operate in investment strategies, styles and factors? Profitable strategies attract risk capital, which competes down returns. Investors would be wise to accept this inconvenient truth.

We do believe that we’ve found ways to quantify intangible value that are overlooked by the market. Furthermore, we believe there are structural barriers protecting this lead. Our lens straddles both the “value-growth” and “quant-fundamental” borders. We believe that institutional constraints (e.g., Morningstar “style boxes”) discourage researchers from venturing into these borderlands.

Of course, we do not expect our head start to last forever. This is why we place innovation at the center of our platform. Over the past year, we’ve added dozens of new facets to our models (e.g., culture, brand personality). We believe our independence and small size fosters a nimble and iterative approach, which has in turn enabled these results. In other words, our boutique size is not a bug but a feature. Most firms fail to innovate not because of limited resources but due to perverse incentives that stifle creativity.

Q: What is the destination for Sparkline? What would you like the firm to look like in 5-10 years?

Sparkline’s goal is to build a world-class investment firm. The base layer of this organization is our research platform. We’ve invested considerable resources in building the AI/ML tools required to extract insight from unstructured data and are continually reinvesting in this tech. These tools allow us to answer an ever-expanding set of questions. We have an ambitious research agenda and believe our “intangible value” framework provides a jumping off point for many exciting areas of exploration.

On top of this research platform, we are building a family of innovative investment products. Our goal is to provide clients with exposure to “intangible value” and other insights in an efficient and scalable way. We believe our unique philosophy will produce differentiated investment returns over the next decade.

Finally, we hope to improve the broader discourse of market participants. We are discouraged by the dogmatic squabbling of “value vs. growth” and “quant vs. fundamental.” We believe that the future of investing lies in bridging these warring factions. One reason we are so committed to sharing our investment research publicly is to show investors that there is a middle path.

Thank you so much, Kai!

Enjoyed this piece? Please let me know by hitting the ❤ button. It makes my day to see whether my readers like the content (it really does!) Thank you!

If you enjoy my work, please consider sharing it with friends who might be interested.🙏

You have a typo: This is not investment advice. Seek your own financial, tax, and legal advice before making any investment decisions. Do you own work! I am are not your fiduciary or advisor.

It should be Do your* own work! Thank you so much for the great interviews.

Thanks for this very informative article.