📰Henry Singleton in 1978: “The Sphinx Speaks”

“Teledyne is like a living plant, with our companies the different branches and each putting out new branches and growing so no one business is too significant.”

Hello everyone,

I enjoy reading old profiles because they can get me one step closer to observing masters “at work.” They can offer context, showcase an evolution in strategy and process, and illustrate how the market thought about an investor or company at the time. After reading

’s recent piece on Henry Singleton, I was interested in revisiting the lessons from his story. So I found myself back in my happy place at the New York Public Library, going through microfilms to dig up an old article on Singleton.

I found an interesting one from 1978 when Singleton had just bought back a ton of stock. Earnings per share were rising sharply but the market was still skeptical. Singleton’s purchases of stock in other conglomerates sparked rumors that he would go on another takeover binge. This was the catalyst for him to sit down with Forbes.

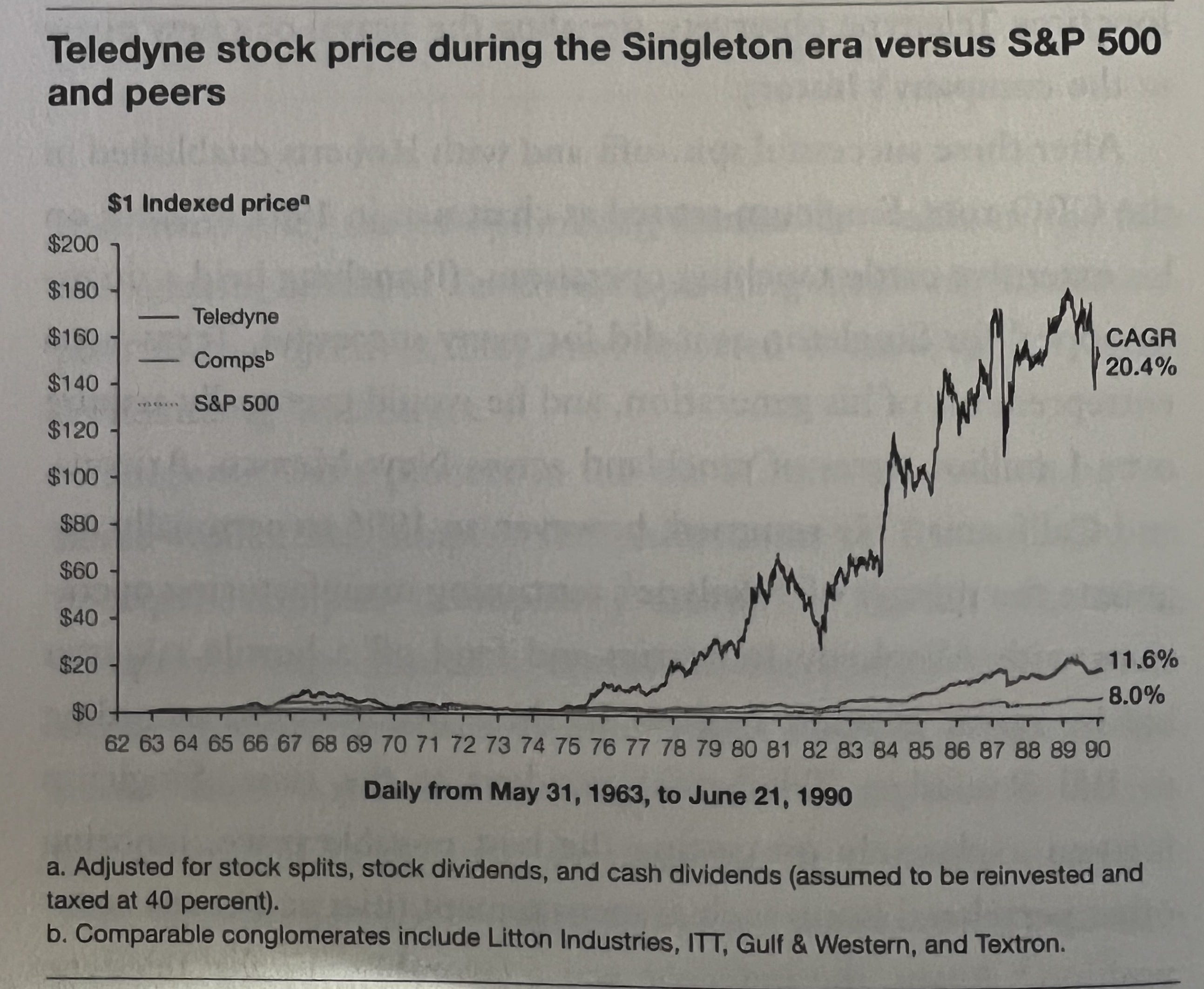

The chart below is from The Outsiders. You can see how the stock was just starting to break out.

Some key lessons:

Capital allocation was crucial. Teledyne’s earnings per share grew ten times during a very challenging decade. But it didn’t happen smoothly and it would not have happened at all without Singleton’s ambitious stock buyback. Shares outstanding declined from 38 million to 11.8 million! As the article pointed out, “if earnings tripled from operations, they rose another sevenfold from asset management.” This was only possible because Singleton had stopped acquisitions and built up cash instead at the peak of the boom.

Investors needed to be patient. Initially, the market didn’t care about Singleton’s massive buyback program. The stock sold off regardless. Investors had to be patient until suddenly “Teledyne shares jumped from 20 to almost 80 in the space of a few months.”

Wall Street missed it. Few analysts covered the stock. One of the few who did believed that investors were “missing one of the great investment stories of our generation because they concentrate on Teledyne's minor aberrations, such as not paying a cash dividend.”

How badly did investors miss the train here? Teledyne was selling “at less than four times” the earnings it could earn that year. Forbes concluded the market was treating the company “like a laggard—ignoring its uniqueness and that of the two men who run it.”

The era of conglomerates was over and investors were skeptical of the company’s prospects. It seems to me Singleton gave the interview for two reasons: to dispel the acquisition rumors and to offer some case studies of companies in his portfolio that had grown organically. Teledyne with its 130 business units seemed to suffer from a severe case of conglomerate/complexity discount.

Singleton managed to maximize value, not to please expectations. Singleton did not care that Wall Street wanted smooth earnings. He noted that Teledyne’s volatile quarterly earnings would “reflect the real world.”

Our accounting is set to maximize cash flow, not reported earnings.

The double-edged sword of insurance. Like Buffett, Singleton had acquired insurance companies whose float he used to invest in stocks. However, one of those acquisitions came with mispriced malpractice insurance liabilities that required a turnaround and forced Singleton to reserve cash in preparation for a worst case scenario.

Buy what you know. Other insurers invested in blue chip stocks and bonds. Singleton saw that his fellow conglomerates and smaller industrials were particularly cheap. So that’s what he bought. Forbes noted that “Singleton buys value wherever he perceives it.”

Stocks vs. acquisitions. Even though stocks were cheap, Singleton explained that he couldn’t pull off acquisitions at those same valuations. Therefore he stuck to being a part owner in undervalued companies rather than expanding his empire.

And how did Singleton think about his own role?

“I define my job as having the freedom to do what seems to me to be in the best interest of the company at any time.”

I recreated the below text from the spotty microfilm and did my best to clean up all the misspellings. If you find any errors just let me know.

Thank you for reading,

Frederik

Keep reading with a 7-day free trial

Subscribe to The Age of Alchemy to keep reading this post and get 7 days of free access to the full post archives.