Hedge Fund Investing is Hard & Michael Platt's Obsession with Risk

"I don’t have any tolerance for trading losses. I hate losing money more than anything. Losing money is what kills you. Not the actual loss. The fact that it messes up your psychology." Michael Platt

Hello everyone,

Investing in hedge funds is hard. Not only are you facing a significant fee burden, you also have to consider where they are in their lifecycle (Jeffrey Tarrant wrote about this some two decades ago). Has the manager become wealthy and lost their hunger? Finally, you wonder: is the manager just outperforming because they are particularly suited to the current market regime — and unlikely to prosper in the next?

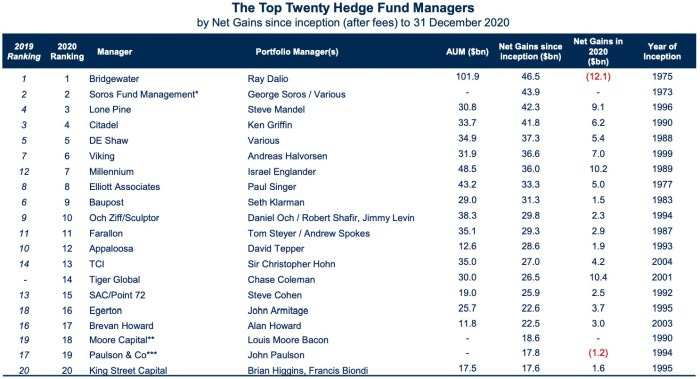

This week, LCH published an updated ranking of hedge fund lifetime gains. The FT commented on the changing of the guard with Tiger cubs fleeing the burning jungle of growth stocks.

While Citadel’s ascent to the top will generate most of the headlines, the 2022 collapse of the Tiger cubs more broadly is pretty incredible.

Citadel’s punchy bets helped it pull well ahead of its major rivals with a staggering 38.1 per cent return from its main Wellington fund last year. That helped drive $16bn of gains, the biggest annual hedge fund gain of all time. (Ken Griffin crowned king of the hedgies)

FT Alphaville’s very rough back of the envelope calculations indicate that this means that the famous Tiger cubs probably lost investors about $60bn last year. To put that in perspective, that means that Tiger cubs accounted for over a quarter of LCH’s estimate for the global hedge fund industry’s overall $208bn loss in 2022.

2022:

Vs. 2020:

The dominance of giant multi-strategy funds made me think of a kind of demarcation line in the business. Call it emotional attachment.

We all know that a stock doesn’t know that we own it. Emotional attachment to an investment is dangerous. And yet it happens, even among professionals. Alex Morris wrote a great piece on Buffett and Coca-Cola that made me wonder about the impact of decades spent discussing how many sips of sugar water the average person drinks.

The same goes for the new guard of long-term oriented growth and quality investors. On the one hand, I love the emphasis on deep analysis and business models. On the other hand, it may get very difficult to change your mind and avoid an attachment to the companies you’re so intimately familiar with.

There is a second level to this and it relates to people. Here, Buffett is unapologetically attached (as long as they behave ethically and don’t slack off). And I intuitively agree with him. Building a firm from the ground up, I would look for people I like and a culture of long-term partnership.

But maybe the top of the hedge fund ranking holds a different lesson. Some people seem to apply their trading mindset to the people they hire. The traders themselves become a portfolio of bets, ideally asymmetric ones. If they don’t work out and hit their risk limits, they’re out.

The best articulation I’ve seen of this was by Michael Platt of BlueCrest who answered “yes, completely” when asked whether he “structured his traders like they are options.” The idea is that each trader has open upside and limited downside with a trailing risk limit of 3%. Here is how he described it:

I hire specialists. I have a specialist in Scandinavian rates, a specialist in the short end, a specialist in volatility surface arbitrage, a specialist in euro long-dated trading, an inflation specialist, and so on. They all get a capital allocation.

If a trader loses 3 percent, he has to give me back half of his trading line. If he loses another 3 percent of the remaining half, that’s it. His book is auctioned. All the traders are shown his book and take what they want into their own books, and anything that is left is liquidated. We want people to scale down if they are getting it wrong and scale up if they are getting it right.

The point of a stop-loss is to overrule one’s emotional attachment to the position. Platt’s process follows the same principle: it eliminates the emotional attachment to the person. It’s not how I would build a firm. But it might be very effective.

Platt is fascinating. A trader with every fiber of his body and obsessed with risk. He’d have no tolerance for the deep drawdowns currently experienced by many:

One thing that brings my blood to a boiling point is when an absolute return guy starts talking about his return relative to anything. My response was, “You are not relative to anything, my friend. You can’t be in the relative game just when it suits you and in the absolute game just when it suits you. You are in the absolute return game.

Why the obsession with losses? Platt believes that drawdowns impair one’s ability to act and take risk. Interestingly, his own career may offer an example of this.

I don’t have any tolerance for trading losses. I hate losing money more than anything. Losing money is what kills you. It is not the actual loss. It’s the fact that it messes up your psychology. You lose the bullets in your gun. What happens is you put on a stupid trade, lose $20 million in 10 minutes, and take the trade off. You feel like an idiot, and you’re not in the mood to put on anything else.

Then the elephant walks past you while your gun’s not loaded. It’s amazing how annoyingly often that happens. In this game, you want to be there when the great trade comes along. It’s the 80/20 rule of life. In trading, 80 percent of your profits come from 20 percent of your ideas.

Keep reading with a 7-day free trial

Subscribe to Frederik's Age of Alchemy to keep reading this post and get 7 days of free access to the full post archives.