Filtering The Idea Funnel

The people who have a lot of opportunities tend to make better investments than people that don’t have a lot of opportunities. — Munger

“Jay was the smartest financial guy I ever met,” Sam Zell wrote. That’s high praise from a legend and immediately triggered my curiosity. Turns out Jay Pritzker, long-time patriarch of Chicago’s Pritzker dynasty, had tried to hire Zell when the latter was still a young lawyer. However, Zell was already succeeding in real estate and had no interest in working for anyone. Instead, he pitched Pritzker on a deal and won him as a mentor and occasional partner.

I am working on a short post exploring how the Pritzker family created much of the blueprint Buffett used for Berkshire Hathaway. But first I wanted to figure out why Zell thought so highly of Jay Pritzker. Zell admired him for his ability to “look at deals and focus on what would either make them or break them.”

He had a laser focus on risk. I like to say my father taught me how to be, law school taught me how to think, Jay taught me how to understand risk.

In 1969, we were working on a deal. I put together a very complex presentation and sat down with him and it took me 25 minutes to explain how we were going to do this and do that and do this and do that. At the end, he looked at me and he said, “Well, step seven is the only step that’s really relevant. That’s where the risk is.” In this case, it was a multi-use complex and the risk really was, could you re-lease the office space? If you could lease the office space, everything else worked.

Zell adopted this mindset which he called a focus on simplicity.

Jay taught me to use simplicity as a strategy. He had an uncanny ability to grasp an extremely complex situation and immediately locate the weakness. He always said that if there were twelve steps in a deal, the whole thing depended on just one of them. The others would either work themselves out or were less important.

For example, he abandoned development in favor of acquiring undervalued assets because development “required multiple steps, and every step meant one more chance for something to go wrong.”

Zell is not the only master of the money game who valued simplicity. Take Bill Miller, who used to rely on elaborate long-term DCF projections:

“For every company, there are a few key investment variables,” he says, “and the rest of the stuff is noise.”

“I’m not that smart and there’s a lot of information out there. So when I look at a company, I just ask myself: “Are things getting better or are they getting worse?” If they’re getting better, then I want to understand what’s going on.’” — Richer, Wiser, Happier

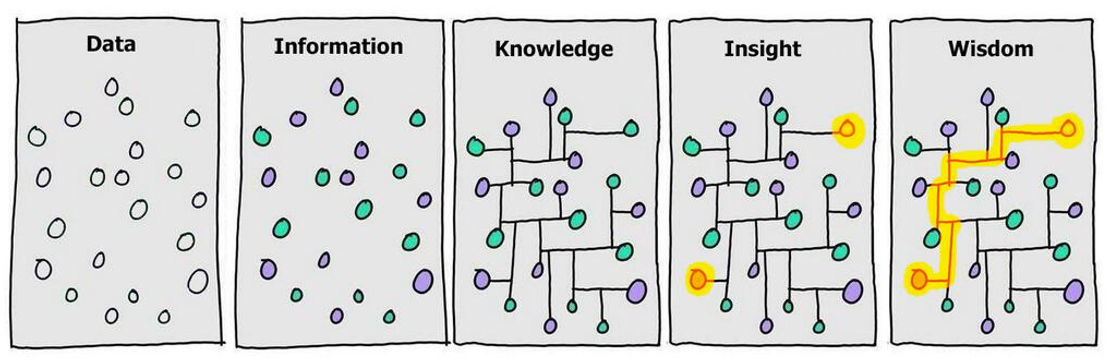

But I think this is about more than simplicity and recognizing what is important in a complex situation. Investing, business, and life require managing what I think of as the ‘funnel problem’, the process leading from ideas to action, from input to output.

My friend Dan McMurtrie boiled it down even better: “Every investor is limited by one or more of the three levels of the funnel: source, analyze, observe / flow / action.”

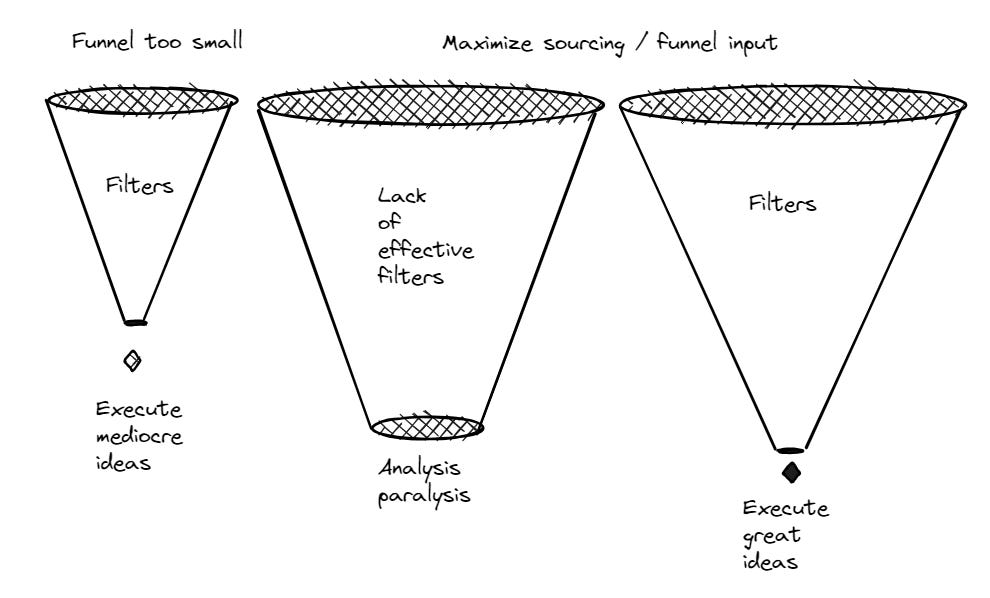

Say you are searching for great ideas, be it investments, ventures, or knowledge. On the one hand, you want to be exposed to a large sample of ideas from which you can select the most valuable ones. You want a wide funnel. On the other hand, your time for analysis is limited. You want to spend as little time as possible to filter out ideas that are either bad or just not a fit for you. If you’re trapped in analysis paralysis, you don’t get to execute and finish.

I believe great investors master their funnel, particularly by developing effective filters which protect their most valuable asset: their time.

This is another observation of a kind of ‘laziness’ or preservation of energy: when there is nothing to be done, do nothing.

They show an urgency to cut to the chase either discard ideas or move downward in the funnel. Pritzker admitted to an ‘overdeveloped sense of urgency’ and was said to get ‘antsy’ when his counterparts were slow-moving. Or take Buffett, usually the epitome of patience. Buffett patiently waits for the market to present a fat pitch but he does not patiently (that is politely) listen to ideas that are a waste of time:

98% of the conversations we can end in the middle of somebody’s first sentence. It works. It’s efficient. We don’t want to listen to stories all day. There’s other things to do with your time.

Zell demanded that same attitude from his team:

I’ve had a number of brilliant people working for me who didn’t make it because they couldn’t grasp how to think about a deal.

I remember walking into the office one night around 8:00 p.m. to find a guy working on a ten-year projection … I realized how many hours he’d spent laboring over his calculations. His approach was ass-backward. You’ve got to be able to look at the deal and know what it hinges on to know whether it works or not. If you realize that the key component works, then you use the numbers to test it. You don’t do the numbers to find out eight hours later whether it was worth starting.

I’m sure his IQ was higher than mine. But that isn’t how we operate. You have to be able to effectively assess the initial picture and see where the greatest risk is most likely to be, or you’ll spend your life doing numbers just to find out if a deal will work. And all that time lost is time you could have been looking at other opportunities.

Or take legendary dealmaker Richard Rainwater. Meetings at his Fort Worth office left some visitors dizzy as he toggled between the phone and multiple conference rooms with deal meetings. His office had glass walls, two doors, and plenty of whiteboard wall space to map out deal structures. It was designed to be an idea factory. Said one partner:

Richard thought his deals out on the walls. We all did. The power lay in holding the Magic Marker.

👉 The remainder of this post and the opportunity to reflect, share, and discuss in the comments are reserved for the community of subscribers. If you would like to support my work and join the conversation, consider subscribing.

Keep reading with a 7-day free trial

Subscribe to Frederik's Age of Alchemy to keep reading this post and get 7 days of free access to the full post archives.