Family Business

I wrote about family offices, once again.

I grew up in Southwestern Germany, Schwaben, a region shaped by its many mid-side family-owned businesses, part of the German Mittelstand. It seems that every town has at least one shop engineering parts for cars or industrial machinery. One of my college friends belonged to a family employing hundreds of people making precision metal parts. On the one hand, that’s nice. I wouldn’t mind being from a wealthy family. On the other hand, my friend’s career and family were deeply intertwined.

He had to figure out his place at the table among his siblings, all facing their father. Who would run the company? How would wealth and power be divided? This would give me tremendous anxiety. It’s very different in my family. There was never a question whether I would go into business with my father. Nor did he ever intend to take over his father’s farm. Rather, it seems that everyone in my family has an urge to create some distance, a space where they can find their own place in the world (to be fair, there has also been no generational wealth creation that would make this question more complicated).

I have tremendous respect for my father who broke out of the tiny farming village in which he grew up. Dad was the only one his age to trek to the city to attend Germany’s higher school. He went to college and landed a job at IBM (a blue chip technology job in Germany of the 80s). But rather than climb the corporate ladder, he left to build his own business. After selling his stake to his partners he was pretty much set. He built a big house, he was liquid, and he had a young family.

Unfortunately, he lost his capital in another venture. He somehow held on to the house. But instead of being able to relax, he was under immense pressure to claw his way back from near bankruptcy. Again he worked around the clock.

I admire his resilience, his ability to stage a comeback and transform himself. Even though he’s slowed down, he is still up at 5am every morning and writes code for several hours.

But his work ethic and ambition put a strain on his marriage. And it left precious little time for family life. I remember the rare late nights when he arrived from the airport with enough energy to build a Lego castle or spaceship. It took me years to understand that his absence had created a lingering resentment within me that affected many of my decisions. Our relationship has improved a lot but it took effort and time and reflection. I don’t know how we would have done that if we were entangled every day as part of running a company.

Maybe that’s why Succession is one of my favorite shows. Take an aging media tycoon, his legacy media empire slowly slipping into irrelevance, and present him with a health crisis. Then watch his children scheme and feud to gain power and his approval. It’s the Sopranos in tailored suits and private jets. A dysfunctional family glued together by the needs of the business, everyone captured by the trappings of wealth and unable to escape.

The beginning of the show sets the tone. Heir-apparent Kendall is trying to close a deal and has to decide whether to increase his offer. Someone asks him if he wants to call his dad to clear the decision.

“Do I want to call my dad? No, I don’t want to call my dad. Do you want to call your dad? Does anybody want to call their dad?”

Yeah. Tough being in business with your father.

No wonder that people get an itch to sell the family business. It’s a scenario that comes up in Succession, too. Logan solicits his children’s opinions on a potential sale. And Roman, the youngest son, responds:

“Actually do have a pitch on this, Dad. Financialization. Float hot. I mean, keep news for political power, for market manipulation capability. But the rest, we play the markets with. You and me up in a little pod above the city, f*cking start ups and shitting on pension funds. Highly maneuverable, highly mobile.” Succession season 2, episode 1

What Roman outlined, liquidating the controlling stake to “play the markets,” would be the inception of a family office.

Which brings me to a piece I wrote before going on holiday about the origins of family offices. It was published last week at Compound.

While the broader concept of staff managing a family’s financial affairs dates back to ancient Rome and European royalty, the modern family office can be traced back to Rockefeller (some argue it was J.P. Morgan’s ‘House of Morgan’ but as I understand it that was really part of the private bank). Rockefeller was an astute businessman but neglected his personal portfolio. He owned a number of scams brought to him by promoters cloaked as friends. He hired someone with no business background but with raw intelligence, work ethic, and integrity. Frederick T. Gates, a former Baptist minister, became a key Rockefeller confidante who structured philanthropic projects and re-structured the mess of a personal portfolio.

His biggest win was doubling down on iron ore properties in Minnesota’s Mesabi Range. This was brilliantly recounted in Ron Chernow’s Titan and this wonderful presentation by Peter Kaufman. Gates and his colleagues became the kernel of the Rockefeller family office (today a massive wealth manager/multi-family office called Rockefeller Capital).

While stratospheric wealth is a prerequisite, it is not necessarily the driving force behind a family office. Instead, complexity and liquidity play important roles.

An illiquid, concentrated position in a family-controlled company does not need much additional financial management. But any excess liquidity to be reinvested creates a potential need for professional management. I think this is one reason why we have thousands of them now: private equity has been buying up countless midsize companies turning illiquid stakes into liquid fortunes that need to be redeployed. It’s also why we find a lot of family offices in the world of technology: not only does the sector create significant fortunes, venture capital financing desires timely exits through sale or IPO, creating liquidity for founders and early employees alike.

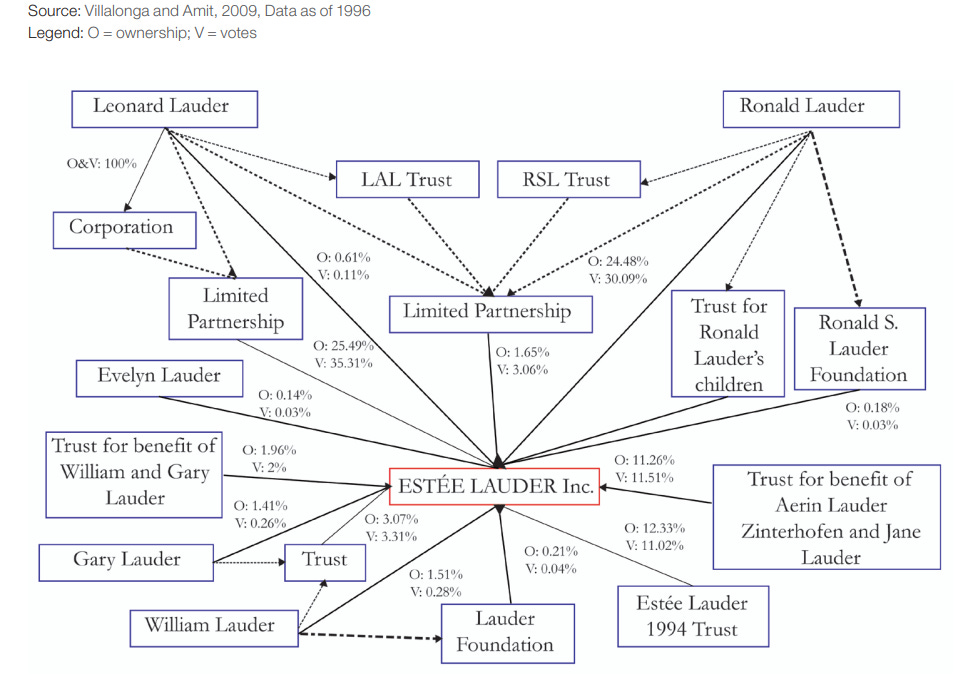

A second key driver is complexity as ownership gets distributed across generations and family branches. Estate planning adds to this and things can get complicated quickly.

I’ve written before about my experience working in this opaque world. Afterwards I had numerous conversations that revealed an interesting business conundrum. Family offices are an audience with enormous purchasing power but seem to lack high quality media dedicated to it. By comparison, I know a private newsletter catering to America’s community of institutional allocators (endowments, pensions, etc.). It’s a small group of readers but an enormous pool of AUM. Their overlapping investment strategies and recruiting needs make the publication a compelling business.

But family offices have far less in common (“If you’ve seen one family office, you’ve seen one family office”). They’re defined by the right side of the balance sheet, their ownership structure. Maybe that makes it impossible to create a great publication for them. Or perhaps that publication exists and I’ve just missed it. Or maybe one of my readers will start it?

It’s striking that the families controlling so much capital still find themselves trapped. Unwilling to show much of themselves, I wonder if their members find enough space for reflection and self development. I wonder if there is growth across the generations or if people spend their lives stuck in the same loops. Can the family become a team tackling challenges together, or are they doomed to an endless verbal knife fight for power?

Great article Frederick. Working for a family business business is like trying to carry a cat by the tail.... it is a unique experience. 😑

If you don't know where you are going , any road will take you there. Is a family office a vehicle for more efficient and/or broader passive investment? Will it be entrepreneurial? Is it based around a central business to which a majority of the family is committed or is it an investment channel for a group of linked by familial bonds and/or shared values ? Is it big enough and does it have a diversified client base and professional management that it ultimately transcends its founding family?

This isn't just an investment issue . It is a question of the continuing appropriateness of a consolidated vehicle.