📚 Can't Escape the Capital Cycle

Capital Returns by Marathon Asset Management and Ed Chancellor

Hello everyone,

The best frameworks apply across domains. You could look at the book Capital Returns, a collection of investor letters, and consider it exclusively relevant to value investors. Who else would be interested in how an industry’s return on capital changes in return over time?

But the capital cycle described in the book is playing out all around us, whether we are aware of it or not. We can ignore it, but it will affect our careers, our investments, and our communities.

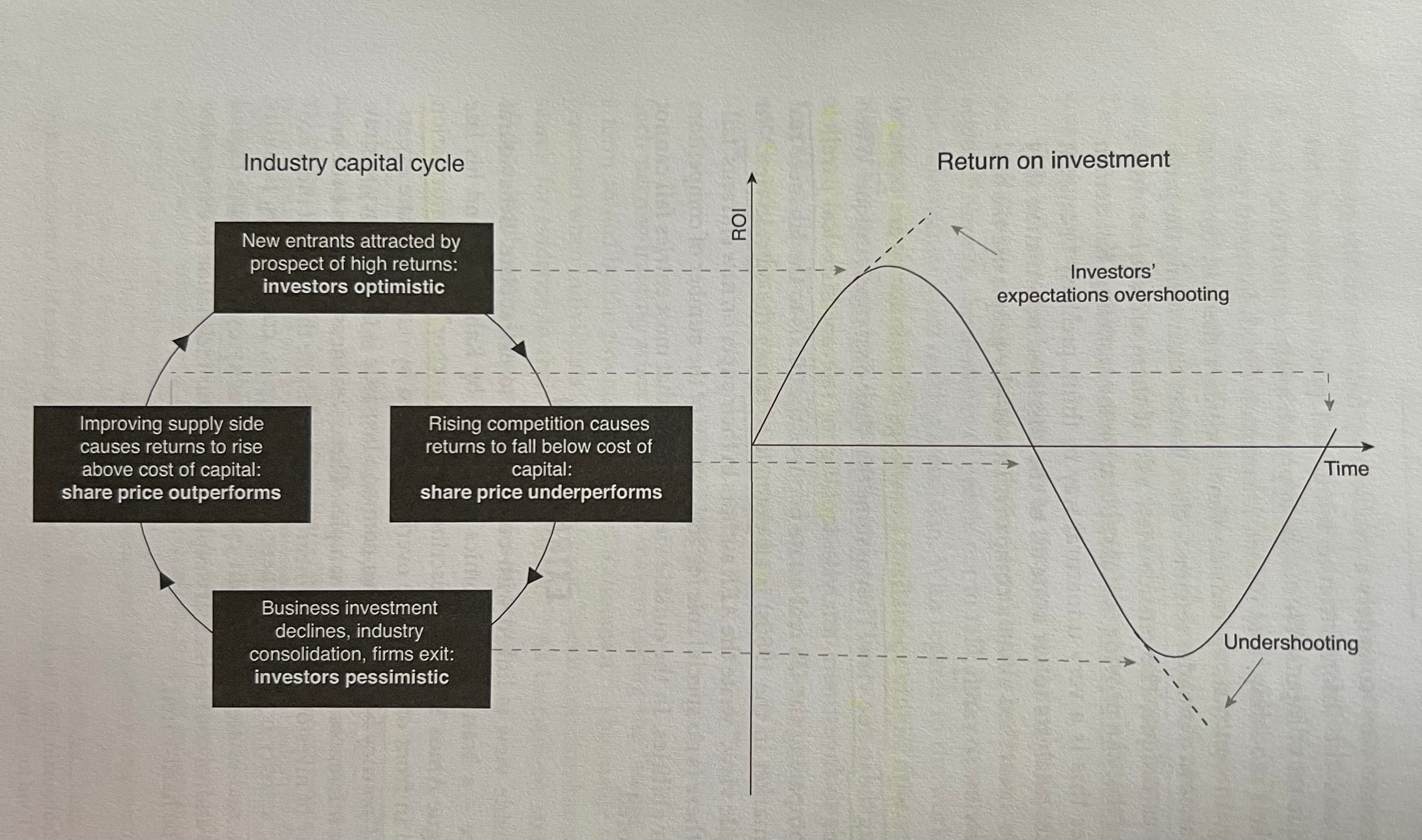

It’s a simple idea and as old as commerce: high returns attract competition and increased capacity leads to declining returns. The return on capital over- and undershoots the cost of capital. Investor expectations, sentiment, and share prices follow along.

Capital cycle analysis looks at how the competitive position of a company is affected by changes in the industry’s supply side.

The great strength of the capital cycle approach lies in its adaptability. The basic insight doesn’t change. Both high and low returns are likely to revert to the mean as valuation influences corporate behaviour and brings about shifts in the supply side.

Capital Returns is filled with great examples and anecdotes and I consider it a must-read for professional investors. Marathon Asset Management did not invent the framework, they just clearly articulated it in their letters and used it to navigate markets.

Marathon often entered investments during the down cycle, when the industry consolidated and capacity was removed. Stanley Druckenmiller applied the same idea as did Peter Lynch. Marathon also invested in the inverse: companies protected from competition. That’s the same as Buffett looking for wonderful businesses or Peter Thiel’s search for monopolies. The two ideas are joined at the hip and rely on an accurate analysis of the industry.

Why does this cycle keep happening? Human nature, incentives, and the delay in feedback.

Both analysts and investors are given to extrapolating current trends. In a cyclical world, they think linearly. High current profitability often leads to overconfidence among managers, who confuse benign industry conditions with their own skill.

Both investors and managers are engaged in making demand projections. Such forecasts have a wide margin of error and are prone to systematic biases. In good times, the demand forecasts tend to be too optimistic and in bad times overly pessimistic.

The delay between investment and new production means that supply changes are lumpy and prone to overshooting.

You can apply the same idea to your career. Let’s assume there is a lack of software engineers which leads to competition among employers. Compensation increases, which is to say the return on your investment in education increases. This attracts competition: more people study to become engineers in college or coding camp. Eventually, the supply of engineers overwhelms demand and the cycle turns down. Returns on the investment in education decline.

Barriers to entry vary for each profession. Engineers may face competition from labor in other countries. Not the case for plumbers whose competition will always be local. The most extreme case of protection from capacity would be something like a sports league with a static number of players.

What can investors do with this idea?

Change your focus from demand to supply.

Play the cycle (but timing is very tricky).

Look for changes in industry structure.

Invert! Look for competitive advantage.

Be mindful of factors that disrupt or prolong the cycle.

Summary: key tenets of the capital cycle.

A few recent examples.

👉 This post is for subscribers. If you enjoy my work, consider supporting it.

DISCLAIMER. I write and podcast for entertainment purposes only. This is not investment advice and the information contained in my work should not be relied on to make investment decisions. Do your own work and seek your own financial, tax, and legal advice before making any investment decisions.

Keep reading with a 7-day free trial

Subscribe to Frederik's Age of Alchemy to keep reading this post and get 7 days of free access to the full post archives.