Boone Pickens: High Stakes Games in a Tough Industry (Part I)

“Looking back, it seems as though I have spent my whole life raising money for a deal.”

Hi all,

What would you do if you had built an oil company and one day found your life’s work at risk due to falling prices, horrendous drilling expenditures, and loads of debt on the balance sheet?

If your answer is: find partners, raise junk bonds, and attempt to take over a company twenty times your size - well, your name must be Boone Pickens.

Energy is a tough industry, you don’t need me to tell you that after a year like 2020 (now the only sector with a dividend yield higher than its historic average). Still, after reading Pickens’s two autobiographies (the 1987 Boone and 2009 The First Billion is the Hardest) I was struck by how much even his life was shaped by the energy cycle. When the sector was being beaten up he found opportunities to drill cheaply and take over other companies. But even he overextended himself and eventually lost his company when prices dropped to rock bottom.

Today' we’ll look at some lessons from his life in a difficult industry:

How the energy cycle shaped his career

How he built his company from scratch

How he pulled off his first takeover

How he pivoted to public markets and took on the energy establishment

As gas prices declined in the 90’s, his company had to be restructured and Pickens was forced to leave. He reinvented himself as a hedge fund manager and profited off the 2000’s energy bull market. This last period of his life I’ll write about in another email.

"I am frequently asked by high school and college students how they can attain success from modest beginnings. My answer is simple. Like many business executives, owe my success to the free enterprise system. I started with a good education, $2,500 in capital, and an opportunity to do something—the sky was the limit, and fortunately the same opportunity still exists."

How the energy cycle shaped his career

Pickens was born in 1928 and entered the energy industry after WW2 when it was in a a slump. This turned out to be an advantage: the cost of drilling was low, the competition for deals muted. He could execute his first takeovers of sleepy, undervalued energy companies and gain valuable experience.

“I often did better in a down market. There was less competition, land prices were lower, and drilling was cheaper.”

Oil prices spiked in the 1970’s energy crisis. While this lead to record profits, it also triggered a drilling boom. Many oil companies had lost their production in the Middle East and competition for domestic exploration drove up prices for land, labor, and equipment. Pickens had built a sizeable company and needed to drill to replace his own reserves:

“Reserve replacement is like a treadmill. It just keeps coming around, year after year. The bigger the company gets and the more oil and gas it produces, the more oil and gas it must replace.”

Trying to avoid the fierce competition in the US, he started drilling in the North Sea and the Gulf of Mexico. Still, he was competing with the capital of the major oil companies.

“It wasn’t long before the majors had bid up the price of everything - from acreage to drilling costs - far beyond its economic value.”

In the 1980’s prices started to slide again and a wave of bankruptcies swept through Texas. At first Pickens skillfully pivoted to the public markets. There he could unlock value in undervalued large oil companies. Although he disliked the term, he set out like a Viking raider, finding poorly defended treasure on the shores of Wall Street.

Eventually this opportunity disappeared and as prices for oil and natural gas continued to decline Mesa Petroleum was in trouble. Boone was booted in the restructuring in the 1990’s and had to painfully reinvent himself. In the 2000’s he re-emerged as a successful commodity hedge fund manager and rode the wave back up as oil entered a new bull market.

In commodity industries even the outsider operators find themselves at the mercy of the cycle. And while Boone was quick to criticize Big Oil for wasting capital, even he fell into the trap of drilling aggressively during the boom. His efforts at diversification were unsuccessful and his capital allocation choices remained limited to public and private assets in the energy markets.

How to bootstrap an oil company

Pickens’s father had been a “landman,” finding landowners willing to lease their mineral rights and then striking drilling deals with the oil companies. When the oil industry entered a downturn in the 1940’s, he joined Phillips Petroleum. Pickens himself studied geology and when he graduated in 1951, the industry was still in a depression and there weren’t many jobs. The head of the geology department told him: “Pickens, they’re not even hiring the good boys.”

He joined Phillips as well, working as a geologist and visiting the company’s wells. He quickly figured out that he didn’t fit into the bureaucratic, hierarchical company. After working late one day he was told: “Nobody stays in the building after hours, and you have been staying sometimes until six o’ clock.”

He realized the company had no appetite for risk and no room for initiative. Employees were more interested in climbing the ranks and not being blamed for mistakes than in finding good drilling ideas. Pickens was told to “shut up” if he wanted to keep his job.

One day after Pickens complained to his wife, not for the first time, probably, she said: “If you hate it so much, why don’t you just quit?” Which he did the next day. He started with $2,500 and a pickup truck. He was independent oilman too now, driving up and down the dusty Texas Panhandle, looking to put together creative deals.

Pickens had two children and a third underway. In the beginning he did well-site consulting work so he could support his family. While being independent seemed scary, his sense of purpose was immediate:

“This was what I was born to do. It became clearer once I was actually out there on my own, putting deals together. The most important thing is that it was just plain fun. Feeling the pure joy of work and success – jumping out of bed in the morning charged up to accomplish something in the day ahead – is necessary for an entrepreneur.”

His bootstrapping formula:

Know the opportunity set intimately. Meet all the players.

Find ways to create value and get paid for the deals you put together.

Become a principal: raise capital and get paid for making judgements, for taking risk.

Know the opportunity set intimately and meet all the players. Pickens worked hard to build unique and valuable knowledge about local geology and built relationships with landowners, leaseholders, and active drilling companies. During the day he visited wells and talked to landowners. At night he studied the maps. His job was to find promising sites and connect these opportunities with capital: people willing to invest and drill.

“The key to making deals was for me to develop “drillable” ideas. I would return to the office at night, after the kids had gone to bed, and work on my maps, looking for places where another well might be drilled or a farmout negotiated. Once I had a prospect, I then started looking for an investor to drill the well.”

Get paid for deals. His initial goal was to get “farmouts,” whereby a leaseholder let someone else drill. In one instance he knew a promising area that Philips hadn’t been interested in. He arranged for a local oilman to drill there. When the wells produced gas, Pickens finally got paid.

“In a typical deal, we would get a few thousand dollars when we sold the prospect and would retain a “back-in interest,” a percentage of any profit the well made.”

Not that different from dealmakers hustling to put together deals, and get a cut, in the worlds of venture, real estate, and private equity.

Become a principal. Brokering deals was a tough way to make a living. Once he had a track record of a few successful wells he raised $2,500 from two investors to form Petroleum Exploration Inc., which would become Mesa Petroleum. He then raised capital to drill by borrowing from a local bank and by putting together drilling partnerships, initially with local investors. Later he started travelling across the US and found capital from a couple of investors in New York (one of them had the patent for blister packaging).

While he was finally getting paid for his judgement, the drilling business was capital intensive and risky. He structured the deals to split the risk, retaining a percentage after selling off pieces of the cash flow to investors. Still, the company tiny and a few dry holes nearly ended his career.

“It was up to me to find the investors. Asking people for money is the most essential skill for a young dealmaker. It was as hard as anything had ever done.”

“Looking back, it seems as though I have spent my whole life raising money for a deal.”

Drilling is hard. Have you considered takeovers instead?

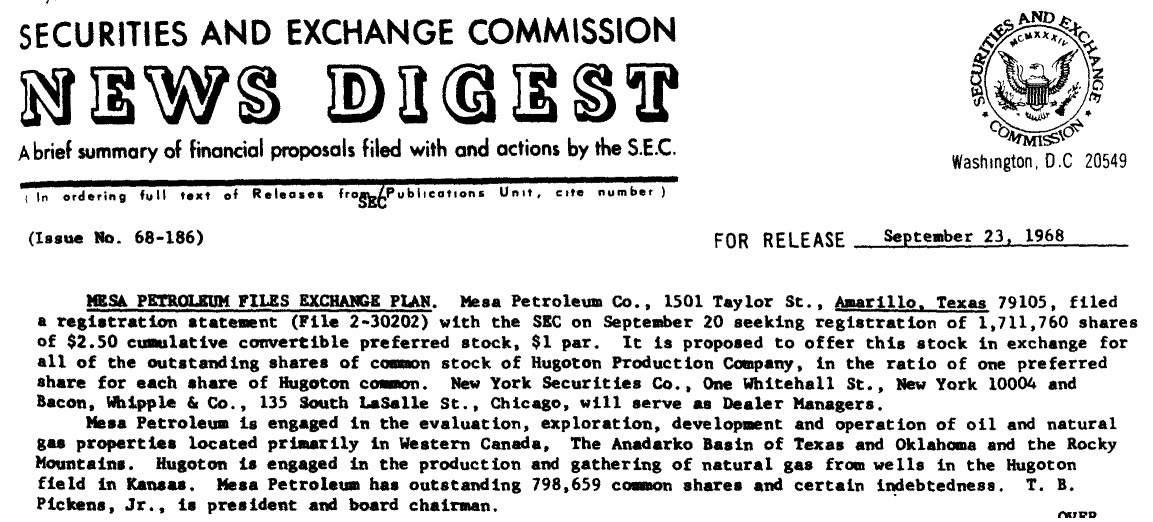

Young Mesa Petroleum went public on the American Stock Exchange generating just $1.5 million in revenue. Pickens wrote in the IPO prospectus: “in addition to internal growth, management is also considering acquisitions in the petroleum industry.”

His first deal was a dud: he acquired a small Utah mining company called Standard Gilsonite for $500,000 of stock. The company’s mining costs however were not competitive with its larger competitor American Gilsonite (I have no idea why he didn’t figure this out before buying the entire company). Despite this setback, Pickens continued to look for deals. “Our growth was steady but slow, and I was impatient.”

While other oilmen were looking for the next gusher, the next big new field, Pickens found the opportunity for step function growth on the stock exchange: Hugoton Production Company. The sleepy company had been spun out in 1948 and owned a large part of the Hugoton gas field in Kansas, one of the largest in the US. The company’s gas reserves were 1.7 trillion cubic feet compared to Mesa’s 62 billion.

Pickens believed the company was undermanaged: it was slowly depleting its reserve and he believed it could achieve better pricing for the gas it. The reason: Hugoton was managed by Mike Nicolais, an officer at a New York money manager which was Hugoton’s largest shareholder. Pickens approached Nicolais about a deal but was rebuffed.

“Mesa’s first takeover battle was about to begin. We felt like Orville and Wilbur Wright. Would this thing fly?”

He decided to make a hostile offer: he offered to exchange newly created Mesa preferred stock for Hugoton stock. His preferred offered a $2.50 dividend whereas Hugoton paid a $2.0 dividend. 17% of shareholders tendered and Hugoton stock rose to an all-time high.

Pickens knew that this strategy had a crucial weakness: if Hugoton’s management cut the dividend, Pickens would start bleeding cash. He would pay cash on the preferred stock while owning Hugoton shares that paid nothing. However, he estimated that Hugoton’s management believed the dividend to be sacrosanct.

Instead, Hugoton’s management announced a friendly merger with another oil company, Reserve Oil & Gas. Pickens reached out directly to Hugoton’s directors and started meeting them in New York. He presented his case on how to create more value with the Hugoton assets if they were run by Mesa. One of the directors called up an old friend in Amarillo to get a reference on Boone. This was Pickens’s reputation:

“I don’t know much about Boone, except that he’s the only oilman in town who still works on Saturday.”

Going the extra mile to make sure your deals succeed

“I have found that many CEOs could care less about the mechanics of a deal and depend almost totally on their lawyers and investment bankers. They don’t ask questions because they are afraid of looking stupid. I would rather look uninformed at thirty-six than stupid forever after.”

Pickens hit the road to convince shareholders to block the deal with Reserve Oil. He heard about a 5% shareholder intending to vote against him. Pickens called him up and the man agreed to talk if Pickens met him at 9am the next day at his farm in Virginia. So he headed for the airport and spent the next morning driving through the countryside. He found the man on his farm, herding cows back into the pen. Pickens climbed over the fence and stepped into the mud to help out. Afterwards he made his case. “Boone, I’m not going to intercede on your behalf. But I’m not going to vote against you, either.”

Another meeting with the board was arranged. After darting Pickens with questions, one director stood up and turned to leave. “I’m leaving. I’m not going to waste any more of my time listening to this guy.”

Pickens called him out: “how much stock in Hugoton do you own? What do you own personally?”

The director owned a hundred shares. Pickens played his trump card: “I own seven thousand shares personally, and Mesa owns 17% of Hugoton. It looks like I’ve got a lot more confidence in Hugoton than you do.”

It was a turning point in the deal. The man stormed out but the unified front among the other directors was breaking. Pickens borrowed more capital and acquired additional stock to get a blocking position. It was a gamble as he couldn’t afford to carry the debt for long. He called up management and threatened to open the exchange offer again. Finally they were ready to talk merger terms.

“The Hugoton acquisition is still the most important deal we ever made. In 1969, it was terribly important for us to make that giant step forward. Hugoton’s assets gave us the leverage we needed to expand our business and play in a bigger league. Debt had never frightened me, and now we had both the experience and the balance sheet to expand.”

His first big deal was not only terribly important but also quite difficult: he still lacked a reputation as a dealmaker as well as capital. Mesa was walking a tightrope. His conviction in the underlying value allowed him to raise the stakes until he forced the management team’s hand. Perseverance and courage got the deal across the finish line.

The lessons of a tough industry

“Geologists generally have a tendency to be overly optimistic because of the nature of their business. You can get a string of dry holes that could destroy some guys, but you can’t give up. You have to think that the next one is going to hit a big field for you.”

Pickens had his share of drilling success, such as in Canada where an initial investment of $35,000 led to a $500 million exit. His efforts to diversify however were duds. Such as when he jumped into the cattle feedlot boom. Mesa became the second largest cattle feeder. When locals complained about the smell, he replied: “it may smell like shit to you, but it smells like money to me.”

He had entered another capital intensive business (for which he had raised capital from investors) with a commodity output. After several years of increasing cattle supply, beef prices fell and Pickens cut his losses and exited with an $18 million loss

“We’ll remember this the next time we’re tempted to diversify”

Things weren’t easier in the oil patch. Pickens increasingly found himself on the “reserve replacement treadmill.” To reduce the pressure, he spun out some reserves into the Mesa Royalty Trust, a company that didn’t replace its reserves and distributed the cash it generated.

Still, he was drilling and hunting for the next big field. In the drilling boom following the energy crisis, prices for land, equipment, and people skyrocketed. Pickens started drilling in more distant and challenging places. In the North Sea he discovered the Beatrice field but was forced to exit when the British government demanded its pound of flesh. He hoped to find the saving gusher in the Gulf of Mexico. Instead, he nearly drowned in shallow water.

Pickens didn’t mince words when it came to the Good Ol’ Boys club of CEOs running the large energy companies:

“They were bureaucrats, caretakers. They had learned to move up through the bureaucracy with a minimum of personal risk. It was a special talent, and not one I wanted.”

“The biggest hurdle in American corporations is the CEO’s ego. Nowadays we talk about ‘downsizing’ companies, but what we really need is a way to downsize the egos.”

“Giving the Good Ol’ Boys excess cash flow is like handing a rabbit a head of lettuce for safekeeping.”

But arguably Pickens couldn’t even trust himself with the “head of lettuce for safekeeping.” He had overextended himself in the Gulf. Declining oil prices were problematic for his leveraged company.

“We had fallen into the trap: Mesa was now totally dependent on continued OPEC price hikes in order to stay active and amortize our debt.”

In 1983 he found himself with his back to the wall. The expenditures for offshore drilling were threatening his company:

“At one time Mesa had more jack-up rigs operating in the Gulf than any other company except Arco. We had spent almost $300 million buying tracts and three times that much exploring for and developing our reserves. We had not found the big one that would cover the dry holes, and I doubted we ever would.”

“Our total Gulf operation was costing over $500,000 a day - a colossal amount of money for a company our size.”

He needed a creative solution to plug the hole and rallied his troops:

“Boys, this is it. We’ve got to figure out a way to make $300 million and we’ve got to make it fast. We’ve lost too much money in the Gulf of Mexico. We can’t drill our way out of this one. A field goal won’t do it – we need a touchdown.”

The raiding game: locking horns with big oil

Boone found the solution in public markets. Oil companies were undervalued and overcapitalized. It was his chance to take on the establishment and either acquire cheap reserves or make make a gain on his investment in a takeover by another company.

“I was intrigued by the relationship of a company’s market price to the underlying value of its assets. Many people, including some managements, like to view the stock market as an irrational mechanism. My analysis was the opposite. Over the long haul, the market reflects management’s ability to make the most out of its assets. So the price of a company’s stock is like a report card. Mesa’s stock has almost always traded near or above the appraised value of the assets. A going concern should sell for at least the value of its assets, and something more if it has good management. If a company has poor management, the price of the stock will suffer, usually selling substantially below the appraised value.”

“Although most CEOs own a few thousand shares of stock, their value as an incentive is insignificant compared to that of the four P’s: pay, perks, power, and prestige.”

“Chief executives, who themselves own few shares of their companies, have no more feeling for the average stockholder than they do for baboons in Africa.”

In 1982, he had tried to acquire Cities Service which traded at a third of its asset value and was six times as large as Mesa. Pickens tried to raise capital and pitched people including Dr. Arnand Hammer of Occidental and Sid Bass. He also approached some of the large oil companies, including Gulf, but they declined to participate in a hostile deal. Meanwhile, Cities responded with a counteroffer to acquire Mesa. Pickens almost lost control of his company. He responded with a bear hug, an offer directly to the company’s board rather than shareholders.

But in the end, Gulf swooped in to buy Cities. In a jab at Pickens, Cities tried to force Mesa to sell its stock back at cost. Pickens pushed back and threatened to blow up the deal until he was able to sell his stock, albeit at only $55 per share, lower than the $63 per share offer by Gulf. Gulf later pulled out of the deal and the stock crashed, hurting the arbitrageurs. The company was then taken over by Occidental.

Pickens’s next big target was Gulf Oil. It was twenty times Mesa’s size, mismanaged, and undervalued. However, it had been undervalued for a long time and due to its massive size it was believed to be safe from raiders. Timing was good: after backing out of the Cities deal, Gulf’s management had lost its credibility on Wall Street. And now Pickens had a reputation and was able to raise both equity and debt through Michael Milken.

Pickens didn’t intend to acquire Gulf. He just wanted to increase the stock price by forcing management to restructure: to buy back stock or create a royalty trust. To him, these actions seemed “self-evident: oil companies were generating substantial cash flows, but the prospects for reinvestment were poor.”

Pickens was accused of trying to liquidate the company and looking for greenmail (selling his stock back to the company at a premium, leaving other shareholders worse off). He argued that the company was already in stealth liquidation, having failed to replace its reserves. And what looked cheap to him was a difficult asset to others as some of Gulf’s divisions were underperforming or even losing money. “Although many analysts said Gulf stock was undervalued based on net worth of assets, others said its price was reasonable based on its earnings.”

On CBS Morning News he was asked “why Gulf” and made a simple and compelling case: mostly domestic reserves, management’s poor performance, and trading at “2.5 times cash flow and a fraction of appraised value.”

Pickens raised capital from other investors and borrowed to take on Gulf. After acquiring 9% and disclosing his stake, Gulf made its first defensive move: to reincorporate from Pennsylvania to Delaware. The rationale: avoid cumulative voting which would have ensured Pickens a board seat.

At the shareholder meeting Gulf’s CEO Jimmy Lee denounced Pickens as a “shark” and declared the royalty trust would “cripple the company.” Pickens was forced to speak from the floor, facing management on the podium, prompting this amazing line: “I appreciate your giving me the chance to speak today from the same level as the Gulf employees and stockholders. Frankly that’s where I feel most comfortable.” It’s all a bit reminiscent of the Gordon Gekko at Teldar Paper scene.

Mesa continued to increase its stake and eventually made a partial tender offer. In response, Gulf entered into a merger with Socal at $80 a share. Pickens had acquired his initial 9% at an average price of $44. In this video (or below) you can see Pickens at the annual meeting around minute 7.40. Following that shot he talked about the outcome:

“A crusader never makes money, I don’t want to be one. There were 400,000 shareholders that came out making $6.5 billion. We happen to be one of the stockholders, the largest, and we made $500 million.

Managements of certain companies are convinced that they’re the owners. That’s not so. The stockholders are the owners. It’s incredible to me to see some directors have zero ownership. Yet they profess to represent the stockholders.”

Pickens became one of the most prominent raiders both out of necessity and because the conditions were right. Mesa needed cash and public oil companies were undervalued, poorly managed, and overcapitalized. Junk bonds and a growing community of arbitrageurs made it easier to execute takeovers and proxy battles. It was an opportunistic move, not the culmination of a career he planned long in advance.

But the biggest lesson to me was that he was not afraid to go for the jugular. After a lifetime of building a company and doing deals he was ready. And when the opportunity presented itself, he went after huge companies, often stretching his team and resources to the limit. He was not afraid to take on the establishment: people who pressured his bankers and partners and who tried to discredit him in the media. It was good that Pickens was more comfortable on his ranch than in a country club anyway.

"If you’re on the right side of the issue, just keep driving until you hear glass breaking. Don’t quit."

“Capitalism without accountability rewards complacency while stifling innovation; it focuses individual initiative on building bureaucracies rather than achieving economic results and replaces leadership with political gamesmanship. We now have a system of ownerless capitalism. The vast majority of our public companies are managed by autocratic executives who have very little ownership in their companies but operate them as if they were their sole proprietorships.”

More Reading:

**Edit: here’s another good profile from 1982, it’s a play by play of the Cities deal.

A word on the two books: Boone was written in the late 1980’s and is an intimate and fun read on his early deals. The First Billion is the Hardest was written in 2009. It includes the 1990’s, when Pickens hit a low point and lost Mesa. It also has a section on his hedge fund days which I’ll cover in another email. But I found it less fun and engaging and it lacked the detail on his early career. This is partially because it also covers his political ideas, namely his energy plan. Keep in mind that both books are personal reflections of an ambitious dealmaker and do reflect his ego. You can also find a summary of his deals in Tobias Carlisle’s Deep Value.

Dallas Morning News “Legacy of Boone Pickens”

NYT Obituary, Fortune obituary

Fortune, 2002: Return of the Raider

How did you like this newsletter?🤔