Birds of a Feather (Dyal, Owl Rock, and a SPAC?)

Are two fast-growing alternative managers going to combine?

What if I told you we could combine the boom in SPACs with the boom in private equity?

To put it a different way, what if we put these two birds together?

That’s right, I’m talking about the Dyal bird and Owl Rock, Arizona. Well, almost. Last week saw a interesting announcement by a SPAC called Altimar:

“Altimar Acquisition Corporation … has executed a non-binding letter of intent with Owl Rock Capital … and Neuberger Berman … with respect to a potential transaction which … would result in combining certain portions of the asset management businesses of Dyal Capital Partners division of Neuberger and Owl Rock as a publicly listed company”

First, let’s unpack this transaction: Dyal Capital is a part of Neuberger Berman and buys minority stakes in alternative asset managers. It owns stakes in HPS and Owl Rock. HPS sponsored the Altimar SPAC. Altimar is now in conversation to merge with Owl Rock and “certain portions of the asset management business of Dyal.”

It’s not clear to me what this will look like. What are these “certain portions” of Dyal? It seems the founding teams of Owl Rock and Dyal would lead a new standalone alternative asset manager. This would be a pretty unusual combination: a minority manager fund (there are only a handful of these) and a direct lending platform. We’ll have to wait for more detail to see the rationale behind the deal.

What do the firms have in common?

Set up after the financial crisis

Different ways of riding the same wave: private equity

Rapid growth and roughly similar AUM (Dyal has ~$22 billion in committed capital, Owl Rock has $23.7 billion)

Institutional investor base and in a good spot to further growth in those allocations

[For reference, Michael Mauboussin’s excellent paper on evolution and growth of private markets.]

Dyal was set up by Neuberger Berman in 2009. Neuberger itself had been part of Lehman Brothers and was bought out by management in 2008. Dyal launched its fourth fund in 2019 and collected $9 billion.

It’s is one of a handful of firms that buy into alternative asset managers. Others include Blackstone Strategic Capital, Goldman Petershill, Investcorp, and other niche firms. There are also firms that provide liquidity for LP vehicles, such as Whitehorse Liquidity and 17Capital, that will occasionally own GP stakes.

This is not a new concept, CalPERS invested in Carlyle in 2000, Nikko bought 20% of Blackstone in 1988, Affiliated Managers Group is a company built around “equity investments in high-quality boutique investment management firms” (albeit in the hedge fund/mutual fund space). Per Pitchbook, 45% of the “top-end GPs” have sold a stake and the market has also become increasingly competitive.

Why buy GP stakes? Buy into a potentially great business (secular growth in allocation to alternatives, capital-light business that scales well), maybe generate co-investment dealflow, create a hedge to the fee burden in your endowment style portfolio.

At this point you can become a shareholder in the largest private equity platforms, Blackstone, KKR, Carlyle Group. Dyal provides a way to access the growth of the next tier as well as the boutique middle market managers.

Why sell a GP stake? Take money off the table or raise capital for the GP commitments to the next fund (valuable if fund size is growing significantly and/or your old fund takes longer than expected to liquidate).

Initially, Dyal did more hedge fund deals. Consider some initial deals such as Whitebox Advisors, MKP (macro), Blue Harbour (activism; now a family office), and Jana (activism).

Jana liquidated most funds in 2019 and was then sued by Dyal:

The hedge fund firm had $11 billion in assets when Dyal invested in 2015. By the end of 2019, Jana was overseeing less than a quarter of that. Dyal eventually agreed to the liquidation of the funds last year, according to the lawsuit. BBG

Hedge Funds have become a tough business and AUM can walk out the door rather quickly. Perhaps unsurprisingly, Dyal’s focus has shifted to private markets - primarily private equity but also credit and real estate.

They invested in some well-known private equity managers, including, Vista, Silver Lake, HIG, Providence, ICONIQ, HGGC, Clearlake (jointly with GS), and KPS. Also Starwood and Round Hill in real estate. And HPS, Golub, Cerberus’s CBF direct lending platform, TPG Sixth Street, and Atalaya in credit.

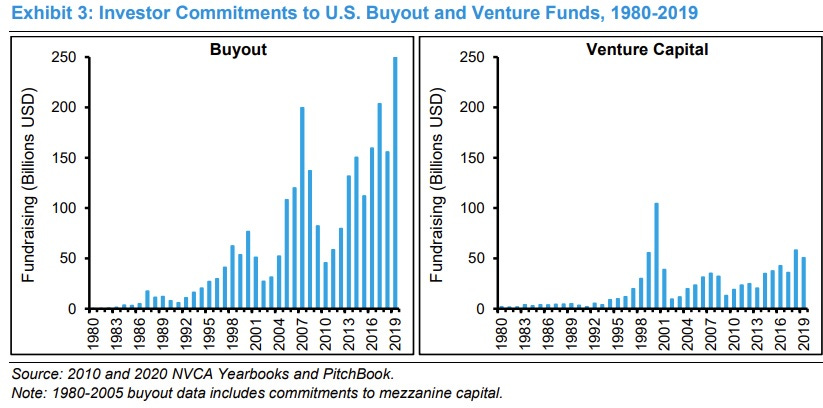

This chart is a bit dated but tells the story for the entire industry:

The story of Owl Rock dates back to GSO, a credit firm formed in 2005 by Bennett Goodman, Albert "Tripp" Smith, and Douglas Ostrover, former leveraged finance bankers at DLJ/Credit Suisse. The business was acquired by Blackstone in 2008.

Doug Ostrover left in 2015 to start Owl Rock. Tripp Smith left in 2018 to form Iron Park and recently teamed up with General Atlantic for a COVID distressed fund. Bennett Goodman retired in 2019. Without the G, S, and O, the unit recently became Blackstone Credit. In 2008, Blackstone had $22.6 billion in credit AUM. Today that number stands at more than $130 billion.

Ostrover set up Owl Rock with two partners, Marc Lipschutz and Craig Packer from KKR and GS. Owl Rock then raised its first private BDC which went public in 2019. In the same year, Dyal invested.

BDCs used to be retail-focused investment vehicles, providing income-oriented investors with access to direct lending. They also offered managers above market fees compared with other long-only institutional credit funds and accounts. This has started to change somewhat as brand name firms have launched large BDCs (think TPG, Goldman, Carlyle) and fees have decreased a bit, especially for new launches looking to attract capital and institutional investors.

Owl Rock was at the forefront of this development, cultivating an institutional investor base by offering incentives to invest in its private BDC (the toolkit includes fee breaks, co-investment sidecars, and fee sharing agreements). Supported by large institutions (33% of its AUM stems from pensions per II) it was able scale much more rapidly than the traditional BDCs which regularly offered stock in small increments in the public markets.

Its first BDC IPO’d with nearly $6 billion in assets. Today that number is more than $10 billion. The firm manages a second (private) BDC with nearly $2 billion in assets as well as other institutional accounts (CalSTRS just committed $1 billion) for a total AUM of $23.7 billion. Compare that to when Dyal invested just one year ago (November 2019): $14.6 billion.

Wrapping up

It’s going to be interesting to get a look under the hood of these businesses. They would offer a way to participate in the growth of the private equity and private credit markets with management teams that are able to rapidly raise new capital and launch more products.

But keep in mind that Blackstone went public in 2007, at the top of the last cycle. And all credit portfolios that mushroomed during expansions should be treated with a bit of caution. Especially since the BDC structure provides a strong incentive to constantly recycle the capital and cover the dividend. Dyal will also be a complex beast, managing four funds that each invest in managers of numerous funds stuffed with illiquid assets.

One other idea that was raised is that the combined entity could pave the way for more GP IPOs, allowing Dyal’s portfolio companies to go public (and returning cash to Dyal’s fund LPs). To answer Bob Ryan’s question: that’s actually something I would be interested in.