Betting on change

"The trick is not to predict an unknowable future, but to try to understand the present, and the probabilities of the various paths that may evolve from it." Bill Miller

Welcome to 418 new subscribers! If you enjoy exploring the business of life and investing, join 3,590 subscribers for free weekly content.

And thank you to Farnam Street for highlighting my interview with Gary Hoover!

Hi everyone,

I just returned from Capital Camp and am still decompressing from an overwhelming amount (for me) of social interaction with strangers. Honestly, I felt like an imposter among so many high-achieving people (exhibit A of the price of surrounding yourself with great people).

I was struck by how many ways of creating wealth were represented at the event. People were building or investing in startups, public equities, real estate, buyouts and roll-ups, quantitative strategies, and crypto. Roughly speaking, one group was betting on change, the other was looking for things that would remain constant.

This reminded me of Bill Miller who started as an “old school” value investor betting on mean reversion in the 1980s. In the 1990s, he pivoted. First, he focused on companies with a higher return on capital. Then he started investing in technology and internet companies, including Amazon, Dell, and AOL.

His fellow value investors shied away from technology due to the sector’s rapid rate of change, among other reasons. Miller took a different view: “Although technology changes reasonably rapidly, it doesn't follow that such change is random or unpredictable.”

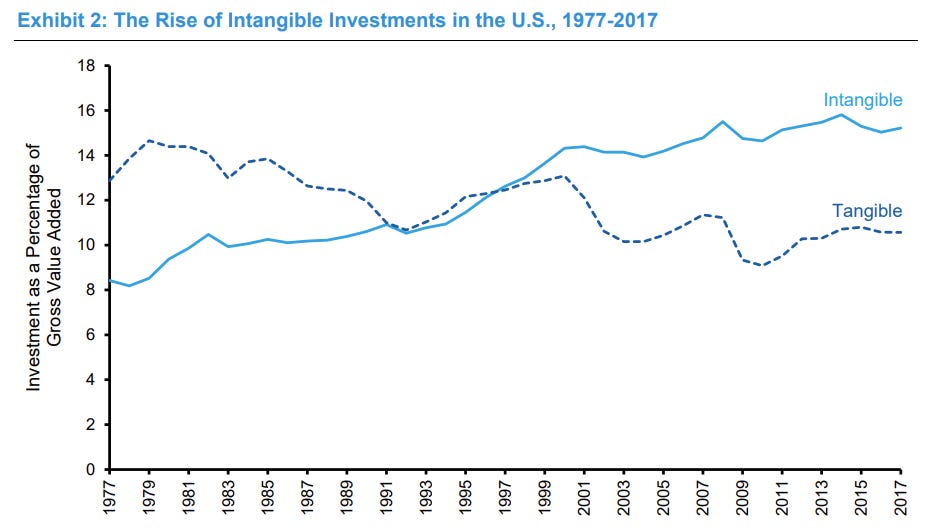

This was right around the time when intangible investment started to overtake tangible investment, as Michael Mauboussin pointed out in his excellent paper.

The collapse of the dotcom bubble seemed to validate the skeptics. But today, we are back in an environment in which betting on change captures the returns, the imagination, and the capital. And as Packy McCormick wrote in Compounding Crazy: “The world will continue to get exponentially crazier.”

Change compounds

Miller mused that the rate of change was accelerating and therefore becoming more important: “There is a universal sense that things happen faster today, that the pace of change is faster, in the economy, in the world, in life in general. This suggests that anticipating change will carry greater rewards and perhaps pay off faster than before, and that reacting to change, even quickly reacting, will not confer any competitive advantages.”

This makes sense if we think about innovation as a compounding force. Isaac Asimov, one of the grandfathers of science fiction, explained in 1988:

“Society is always changing, but the rate of change has been accelerating through history. Change is cumulative. The very changes you make, make it easier to make further changes. It was only with the coming of the Industrial Revolution that the rate of change became fast enough to be visible in a single lifetime. That was when science fiction came into being. People knew they would die before they could see the changes in the next century, so it would be nice to imagine what they would be.

It becomes more and more important to adjust what you do today with the fact of change in the future. It's ridiculous to make your plans now on the assumption that things will continue as they are now. You have to assume that if something you're doing is going to reach fruition in ten years, that in those ten years changes may take place and perhaps what you do will have no meaning then.

Science fiction is important because it fights the natural notion that there’s something permanent about things the way they are right now.”

As an aside, I have been thinking about a book project. But the idea of investing years into something that could be “too late” is terrifying. It is a strong incentive to only focus on timeless content.

There is nuance to the speed of change though. In 1983, Asimov was asked to predict the world of 2019. He could see the continued computerization, musing that the "mobile computerized object" will "penetrate the home." However, until recently I would have called his thoughts about space exploration overly optimistic. I would have referenced Peter Thiel’s notion that rapid innovation in the digital realm was masking a lack of progress in the physical realm: “We wanted flying cars, instead we got 140 characters.” But today, the “first space settlement” which Asimov envisioned to be “on the drawing boards” might well be Musk’s plans for a base on Mars.

What if the future doesn’t look like it?

It is difficult to distinguish the future from a passing fad and it gets harder as we age. Douglas Adams wrote:

“I’ve come up with a set of rules that describe our reactions to technologies:

1. Anything that is in the world when you’re born is normal and ordinary and is just a natural part of the way the world works.

2. Anything that’s invented between when you’re fifteen and thirty-five is new and exciting and revolutionary and you can probably get a career in it.

3. Anything invented after you’re thirty-five is against the natural order of things.”

Plus, the nature of innovation changes. Dan McMurtrie said “the nature of progress is ever more trivial nonsense.” As we move up Maslow’s pyramid to tackle ever more marginal problems, he said, signal and noise are getting difficult to tease apart, “because the things that are signal are getting dumber.”

This seems especially challenging inside bubbles when capital is abundant and a wide variety of experiments get funded. What if the future was right in front of you but it looked too silly to warrant much attention?

I remember reading Peter Lynch’s One Up On Wall Street, my introduction to investing. Lynch argued that retail investors could gain an advantage over the pros by paying attention to their environment: What items were selling well at the mall (remember those?), which companies were taking the lead in the industry you worked in, what restaurant was always packed, what clothing brand or toy were selling out, that sort of thing.

That kind of anecdotal insight is only possible if you are interacting with novel ideas. That becomes a challenge when novelty looks like a weird fad and is quickly dismissed. If the future is in fact getting dumber, meme stock traders might have a tiny advantage over professionals after all.

Crypto and NFTs fit squarely into this bucket for me. For years I was curious but confused by the lack of real-world applications (beyond trading and storing wealth). However, the asset class seems to be quite lindy, it refuses to fizzle out and go away. Not only that, crypto also remains a highly infectious meme that keeps attracting more people, more creative power, more capital.

Along came NFTs which I believe could solve a real problem, namely the lack of value accrual to digital artists. But that doesn’t mean that NFTs must look anything like what I would consider art. They are built buy and for new communities. Case in point, in an experiment with this new world, I nearly bought a jpeg of a piece of a smashed toilet last week (but I was too slow and the server struggled with too many prospective buyers):

Take another hot buzzword, the Metaverse. It is easy to assume a shared, immersive digital world will look like a VR version of the real world. Serious and useful, saving you money on office space and travel.

But what if it will be built by and for a younger generation? What if they prefer a crossover between Lego and Hello Kitty?

McMurtrie’s advice is to find people who closer to the trend, as guides if you will: “we call it tasting the Kool-Aid, where when we see something that seems insane to us, we have to go into the lion's den and go talk to the people who are really into that thing and figure out, what is this from their perspective?”

Another friend of mine shared a timeless quote that touches on the same idea:

“When you are younger, you need older mentors. When you are older, you need younger mentors. They teach you to be young again.”

Get used to being wrong

If change is more important than ever but also faster and weirder, we should probably accept that we will be wrong more often.

If you have time for another great podcast, check out my friend Tom Morgan on Jim O’Shaughnessy’sInfinite Loops. This is how he described great investors:

“If I was to isolate kind of a uniform trait, it's the ability to see the entire landscape as accurately as they possibly can at a single moment in time. To probabilistically work out what all the outcomes are, and then to dynamically adjust those probabilities as new information comes in. That's exactly the trait of Phil Tetlock's superforecasters that destroy expert predictions on everything. Because what they're doing is they're effectively destroying their ego every 15 seconds, because everything's a hypothesis to be tested.”

While ego death sounds a little dramatic, Tom hits the nail on the head. Once we place our bets, we can become awfully resistant to new information that would force us to revise our worldview.

Which is one reason why I enjoy studying macro traders like Paul Tudor Jones or George Soros. They are navigating markets like oceans. Their portfolios could be swallowed by the sea at any moment (before Victor Niederhoffer blew up in 1997, Soros warned him about surfing waves that were too big with the words "That's your big problem. You don't know when to stand away.")

They can’t afford to invest ego in a position because holding on for too long would threaten their survival. They accept being wrong, cut their losses, and move on without a second thought.

“When a trade is wrong, he [Soros] will just cut it, move on, and do something else. I remember one time he had this huge FX position. He made something like $250 million on it in one day. He was quoted in the financial press talking about the position. It sounded like a major strategic view he had. Then the market went the other way, and the position just disappeared. It was gone. He didn’t like the price action, so he got out. He doesn’t let his structural views on how he believes the market will play out get in the way of his trading. That is what strikes me about really good money managers - they don’t get attached to their ideas.” Soros, “World’s greatest loss taker”

Compare that to the fundamental investor whose premise is that the market is wrong, that a particular asset is mispriced. Mauboussin wrote an equity investor’s one job was to take advantage of “gaps between expectations and fundamentals.” Miller wrote:

“Systematic outperformance requires variant perception: one must believe something different from what the market believes, and one must be right. More simply, the market is either wrong about how important something is, or wrong about when that something occurs, or both.”

Believing one can outsmart “Mr. Market” requires confidence and conviction. But confidence can turn easily into arrogance and conviction into stubbornness. It is an inherent tension and difficult to balance.

No straight line

Miller often quoted Wittgenstein:

“When we think about the future of the world, we always have in mind its being where it would be if it continued to move as we see it moving now. We do not realize that it moves not in a straight line ... and that its direction changes constantly.”

Stock prices are a wonderful visualization of this constant change in direction. Consider how right and wrong a fundamental investor in change could look at different points in time.

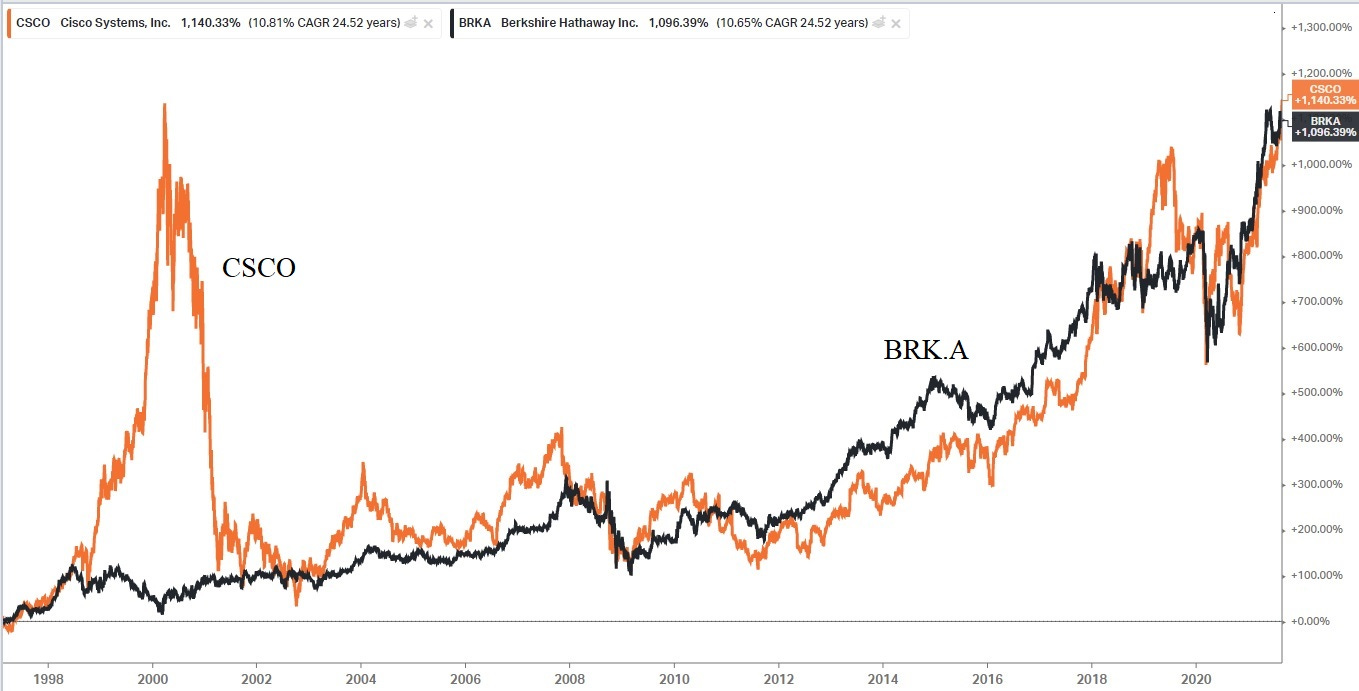

In 1997, an analyst pitched Warren Buffett on investing in Cisco. Two years after the Netscape IPO, the Internet was picking up steam. Cisco as the leading manufacturer of networking equipment was "akin to shovel manufacturers during the Gold Rush of 1849.” The company was “best positioned to benefit from the initial hype over the Internet.” Cisco stock turned into a ten bagger in a few short years – before imploding.

In 1999, Miller wrote about the pitch: “There is no evidence Buffett read the letter, but we read it and didn't buy Cisco. Johnson was right and we were wrong; not because the stock went up a lot, but because it was significantly undervalued and we missed that.”

Amazingly, more than two decades later, Cisco and Berkshire Hathaway ended up in nearly the same place. But along the way, investors could look like geniuses and idiots. Careers were made and destroyed by the future’s constant change in direction.

Conclusion

We don’t have to bet on change. Jeff Bezos once said he tried to bet on "what's not going to change in the next ten years" (consumers wanting convenience, selection, quality, etc.). Morgan Housel put it very well recently: “Predicting what the world will look like in, say, 2050, is just impossible. But predicting that people will still respond to greed, fear, opportunity, exploitation, risk, uncertainty, tribal affiliations and social persuasion in the same way is a bet I’d take.”

During a recent conversation with Bill Brewster, Jim O’Shaughnessy said: “markets change second by second, human nature hasn’t changed millennia by millennia. Arbitraging human nature is the final edge.”

It’s important to invest within a “circle of competence,” an area in which an investor can analyze situations better than others and place bets with an edge. However, the circle should be change or expand as over time as we learn and the world changes.

Steve Jobs compared the human mind to an electrochemical computer which got “stuck in patterns” with age, “just like grooves in a record.”

“Of course, there are some people who are innately curious, forever little kids in their awe of life, but they’re rare.” Steve Jobs

We have to fight getting stuck. We need to be “curious, not judgmental” (maybe by Whitman, definitely by Ted Lasso). Within our circle of competence, we can exploit what we understand already. But to understand change, we must keep exploring. This might require an investment of time in, or an occasional bet on, things that look silly or foolish. It may require finding mentors who “teach us to be young again.” It requires a comfort with being wrong that serves long-term learning and compounding.

“Being wrong is something anyone involved in capital markets has to get used to, though being used to it and being comfortable with it are two different things.” Bill Miller

Enjoyed this piece? Let me know by hitting the ❤ like button.👇

Please consider sharing it with friends who would enjoy it as well. Thank you!

👏 I love the way you write.

In my opinion, even the absence of change is a prediction. We must predict the future - otherwise there would be no way of valuing anything.

Excellent once again :)